Introduction

Microfinance refers to the kind of banking service offered to the people with no jobs, low income earners or to people with little access to the financial services. In other words, Microfinance is a combination of many financial services aimed at people earning low income. As a result of aiming at the low income persons, the products provided by these microfinance institutions have low monetary values. Some of the examples of the products offered by the microfinance institutions include small grants, loans, savings and insurance policies. The amount of these services given depends with the financial needs of the person taking the loan. Due to the fact that microfinance institutions targeted the poor population, they in some instances use traditional methods in their lending process. Microfinance is currently a very popular strategy of poverty reduction in the world. Both rich and poor nations poverty stricken areas and have poor people living there. As indicated by Shah (2008), poverty has always been present in all these nations. The World Bank report compiled in 2005 indicated that 1.4 billion people in the world live in adverse poverty. This is about 25.2% of the entire world’s population (Bauer et al., 2008). The reduction of poverty globally was driven by china (ibid) and it managed to reduce the world’s poverty by 10%. Most of international development debates have been dominated on the concerns about poverty reductions strategies that can be adopted by countries. Nations have tried both micro and macro level programs to eradicate the problem of poverty. These programs have been undertaken globally and at regional level by relevant bodies like the United Nations, World Bank, IMF and Asian Development bank among others. The governments and nongovernmental organizations have been on the vanguard to try to alleviate poverty among the people. Alleviation of poverty in the world is a continuous process because sometimes poverty is seasonal based on the prevailing conditions in an economy. For instance, in most of the countries that are dependent on agriculture, poverty level tends to reduce during the harvest seasons. When there is draught the rate increases. Microfinance has been cited by most organizations as the most viable method of poverty reduction. Microfinance has been growing at a very high rate in the world in the recent past. According to Cheng (2003), data obtained from Microfinance Information Exchange (MIX) showed that the sector expanded at historic rates, with average annual asset growth of 39 percent, accumulating total assets of over US$60 billion by December 2008. The microfinance institutions that are serving people around the world have increased to about 2500 worldwide. According to Sengupta & Aubuchon (2008), the number of people globally who are using microfinance services have also increased to over 67.6 million clients. There is evidence, therefore, that microfinance has greatly contributed to poverty reduction. They improve the socio-economic conditions of the poor in many countries. For instance, the microfinance institutions have programs for providing credit facilities to their clients. The programs can be proven to be very successful because of the repayment rate of loans has been successful. They level of awareness of the target groups about the microfinance facilities also indicates that there is great improvement. The receivers of the credit have also developed and their livelihood improved. There are some critics who do not agree with this conclusion. They believe that you cannot eliminate poverty through the small amount of credit that people get from the microfinance. They argue that the poor are just implicated into the long debt cycle. However, this criticism is diluted by Ahmed (2004) who says that when one gets a little, it is easier to acquire some more. He argues that the most difficult thing is to get that little. Those living in adverse poverty do not have even that little amount. When they have access to it, they are able to stat an income generating activity; however little it will bring in. the biggest issue has been how the destitute will get the little amount they so desperately need. The Microfinance institutions are available to give the poor that little amount. That is why the MFIs are very relevant to the poor because they enable them to make more through the little they get from them.

The study has tried to address the impacts of the microfinance on the lives of the poor people who lives in China and more specifically to the people who lives in the rural areas. This paper tries to look at the microfinance institutions in China and more specifically on the poor people living in the rural areas. The study is more specifically aimed at answering the question what is the impact or effects of microfinance institutions on the lives of the poor rural households’ individuals in China?

Statement of the problem

Empirical analysis has been done on the impact of microfinance on the standard of living. Analysis started in the year 1990. However, the studies are few and more research has to be done. Some of the studies have questioned the importance of microfinance in alleviating of poverty. Adams & Von Pische (1992) argued that the use of debt is not a good tool that can be used to help the poor in improving economic conditions. Adams and Von Pische (1992) points out price fluctuations, risks associated with technology and market conditions as some other issues that need immediate attention among the poor population. Other researcher has also doubted impacts of such program. Gulli (1998) says credit is not the key challenge facing growth of micro enterprises. Mayoux (2002) there are some economic empowerment strategies that are non-existent but are almost always talked about. Studies have shown that micro entrepreneurs need to be empowered at all levels so that they may generate an income through projects established through microcredits. Those living under poverty lines, if not well trained on entrepreneurial skills, will consume their microcredits and engage in none of income generating activities. Therefore income of the poor is expected to decrease while those for the rich are expected to increase (Gulli 1998).

Other research which has been done indicates that poor households have a higher chance to use loans from the institutions for consumption purposes. Conversely there are some researches which have shown that there is a positive correlation between microfinance and poverty reduction. In fact other have microfinance is much important not only to the beneficiaries but also to the rest of the community (Khondkar, 1999). In carrying out the research, Khondkar, (1999) used a number of households to carry out the research and came up with conclusion that access to microfinance loans helps in the poverty reduction. This is notable especially so to women at the village level. Contrary to this Murdoch has contradicted argument by Pitt and Khandker’s and he says his research concentrated on program selection rather than the impact of borrowing.

Studies done have found out that microfinance plays a big role in most countries in mitigating poverty levels. Murdoch (2002) says that microfinance have a positive relationship with poverty eradication. He goes on to say that credit extended to the rural people helps to fund self-employment opportunities which help to increase their income. According to Peace & David (1994), microfinance helps to generate more jobs to people living in poor areas as well as those living in low populated regions Other studies which have been done also indicates that micro finance are an important aspect in poverty eradication but rarely is accessible to the poor group as it has always be claimed (Hulme and Mosley, 1996). Rahman (2001) carried out a study on the impacts of microfinance programs. The impact of the two was found to be significant but mostly to the rich population.

The study further identified that richer households are in a position to obtain more amount of loans since they have a lot of influence through high ranks they have in big microfinance institutions. Rahman (2001) says that the impact of the loans on households depend on size of the loans they acquire. He says there has been an increase in the number of drop out from microfinance program due to the complaint that the size of the loans are very small to impact on investments they make and their lives. In another study done by Mosley (1996), he reports that more than 25 % indicated an improvement in their lives while 60-65% did not change in term of their live. He also noted that 10% to 15% were bankrupt even after obtaining credits from the institutions. This means that their lives retrogressed instead of progressing after participating in microfinance programs.

Loans extended to women make them more indebted putting them in a vulnerable and desperate position. In addition, he concluded that poor households deplete most of their assets in the process of making loan repayments as the income they obtain from investment opportunities are not enough. Microfinance institutions make a difference in the lives of the poor who take part in their programs. It is expected the impacts cannot be direct to every person and to everyone who engages in such programs. It is important to note that although there has been no research which has shown any strong impacts of microfinance credit, a lot of studies suggest the possibility of an existence of the same. There is, therefore, need for more research in this field.

More research should be done towards to identify the context in which better impacts will be obtained (Nanda, 1999). There is a general agreement that the impact that credits from microfinance institution have in one region might be different for another region (Montgomery et al, 1996). This is due to the changing socio cultural and economic environment. Future research focused on these changing contexts will help to increase pools of knowledge in this field.

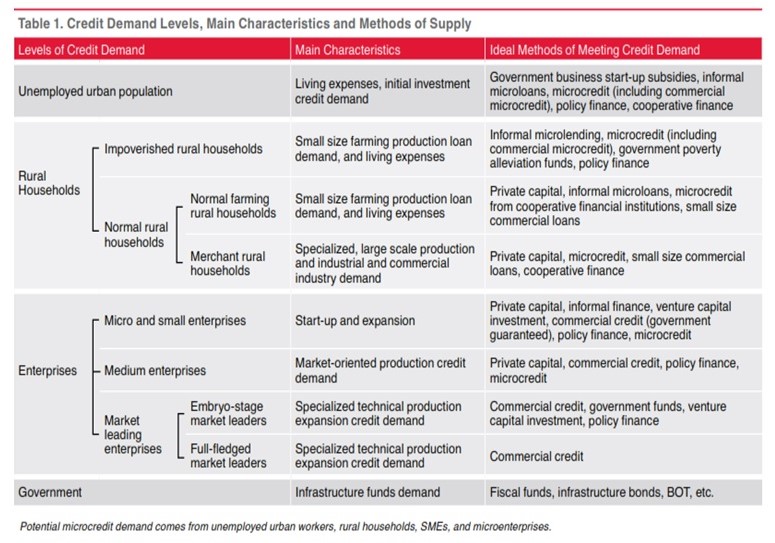

It is from this foundation that this analysis is based on. The study focuses the Impact of Microfinance on Rural Poor Households’ Income and Vulnerability to Poverty: A case study of China poor population. The study targets more on the poor people. The study done by Tambiah (2010) on the status of microfinance in china revealed the need to conduct an analysis to investigate the effects that microfinance would have on the livelihood of poor population. He came up with the following summary:

The summary above shows that the improverishes rural population are in high demand of microficance loans to start small size farming and meeting living expenses. Other studies ahowed that they need funds to start small businesses to help them earn a living. They need to have a valid reason for borrowing loans from microfinances. If they borrow purely to meet living exenses, they will not manage to service the loan. Most of those who obtain the loans indicate starting up a business as the reason foor borrowing. Does microfinance really improve the livelihood of there people? Does it affect their income? Does it reduce their vulnerability to poverty? The are the main questions that necessitated this study. This study will focus mainly on answering these questions.

Research objectives

In the contemporary microfinance industry are established to give microcredits to the population that cannot get such assistance from other big financial institutions. In short this thesis has four main. They all have some degree of interrelation so that they can bring some level of understanding of the impacts of microfinance towards the rural poor households in poverty eradication. The attributes of the households are also studied. This has also helped to determine whether the poor people are the ones who obtain loans or not. The study also wanted to understand the reasons for obtaining such loans. The objectives are summarized below:

The basic aim of the study is to investigate whether microfinance is of any significant influence on the poor population in China or whether it plays a role in making them less prone to poverty. This general objective is broken down into a number of specific objectives that are listed below.

- To explore the socioeconomic factors that surround households that take part in microcredits programs among the rural population in China.

- To find out the factors affecting loan acquisition among the poor population in the rural China.

- To investigate whether loans obtained from microfinance institutions significantly reduce poverty.

- To find out the impact of microfinance on household income

Research Questions

The above objectives will be analyzed by answering the following questions.

- What are the social economic factors and background of households participating in microfinance credit programs?

- Which are the factors that determine the amount of loan acquired by the poor households in china?

- Does microfinance significantly reduce poverty?

- What is the impact of microfinance on poor households’ income in China?

The other relevant question in this study concerns the impact of microfinance on household incomes and vulnerability to poverty. The main issue here is the role of disjoint liability groups in ensuring that households afford to repay their loan to the microfinance institutions.

Limitations of the Research

The major limitation that was faced in this study is time. The behavior of poor population in china in an environment with high accessibility would require enough time. It needs to be studies over a long period of time. There are other factors that could have been very useful in the study but they needed a lot of time to observe. For instance, the factors that affect the success of microfinance among the poor population in china could have been of great use in the study but need to be observed over time.

The other challenge was availability of data. There is little data that is published about the variables used in the study. For instance, there is not up to date data about the level of lending of microfinance in China. The amount of loans given to the poor in china by microfinance institutions on annual basis is very scanty. However, the research overcame these limitations by reviewing a lot of literature to gather the necessary information. The objectives of the study were met because reliable data was obtained. Most of the data related to the topic of study is not consolidated and it was gathered from different sources.

Significance of the study

The study will be very helpful to a number of parties.

The government of China and other Countries

The government of china should benefits from the research because it will be easier to assess the success of microfinance in alleviating poverty in china. Other counties will also understand the role of microfinance in improving the livelihood of the poor in the country. The countries that are using microfinance in alleviating poverty will be able to see the areas that they need to improve.

The Microfinance Institutions

The recommendations of this research will be very helpful to the microfinance institutions. They will see the areas they need to improve I order to make their objectives fully achievable.

The poor population in China and other region

The poor populations are also he targeted beneficiaries of this research. They will find solution for their situation from microfinance. The poor populations are also he targeted beneficiaries of this research. They will find solution for their situation from microfinance. Thy will find out that microcredits can help improve their livelihood.

Literature Review

Most governments and donors concentrate on addressing liquidity issues that they believe are the main challenges that the poor households face (Jegede et al, 2011). There is, therefore, a high chance of reducing the level of poverty if this problem is addressed. According to many economists, poverty cycles require intervention from different sides for it to be eliminated. This force will help increase the demand of goods and services. This can only be done by bringing some liquidity which will in turn improve productivity of labor. This can be done by microfinance institutions. These institutions help to inject liquidity by ensuring economic empowerments which consequently improves household standards of living. On extension of credit from micro finance institution, there will be good market for products in which they will make investment in.

Microfinance operation is based on foregoing assumptions. They believe that the impact of poverty reduction and economic empowerment among the poor population are what these poor people have been lacking for many generations. The success of credits from microfinance depends with how successfully microfinance programs help to address the problem facing the rural population. One of the key factors that enhance better impacts by microfinance is better understanding of strengths and limitations of micro credit (Gulli, 1998).

Rahman (2001) notes that growth in microfinance in China has been caused by market forces. Many donors and nongovernmental organizations see microfinance institutions as a way of improving living standards of the poor. However, there are some doubts that have arisen on how microfinance has impacted greatly on the lives of the poor yet many financial institutions are failing.

It is known that the poverty and desperation experienced by poor households have resulted to such areas becoming good markets of microfinance services lenders. This is caused by the need for liquidity and consumption as well as need for micro smoothing or for micro entrepreneurship. In order to reach the poor population in China, microfinance institutions have come up with innovative strategies to help them.

One of the ways used so that it can be successful is asking the poor households to form themselves into groups before they obtain loans. This has ensured joint liability for such loans. Another tactic they use is to ensure they give repeat loans to those whose loans perform well.

The ability of the poor household in China to borrow and save is not very obvious but at the same time their need to obtain such credit is more than for people whose living standard is high. Therefore, it is important for micro finance institutions to help such poor people manage such credits. This is done by such institutions through ensuring they have received remittances and makes savings after selling their produce. Credits obtained from microfinance bodies have enabled the poor Chinese people to save and hence cope with volatility of their incomes. This in turn results to stable consumption habits (Shah, 2009).

Despite the better impacts that loans extended to the poor rural Chinese have, there are still some challenges that microfinance institutions have faced. The genius microfinance institutions have been in a position to come up ways of dealing with such problems. Some of the problems they face include ensuring high volumes of loans, retaining customers and ensuring reduced fraud in dealing with poor borrowers.

The role of microfinance in improving the lives of the poor has even been acknowledged by Nobel peace prize committee (Rogaly, 1996). Globally, there has been a projection in poverty eradication which has left an impression that there is need for magic to ensure improved impacts from micro finance (Hudon, 2006). A good example in this is use of suitable stories on the effects of microfinance on specific households. Policy makers and donors have come to know that one of the ways of eradicating poverty in rural areas of China is through the use of microfinance services like credits and loans (Glazer, 2010).

Although much research has not been done to show the relationship between the two, there is some believe on a lot of correlation (Roper, 2002). Some research has also come up an assertion that microfinance causes a lot of negative impacts on the lives of women (Mayoux, 2002). This is the case in some countries while in others, for example in Bangladesh, there is a positive impact (Khondkar, 1999). In other countries like Thailand, it has some mixed results. In other countries in Africa like Kenya, it has an insignificant impact (Kiiru, 2007). The above trends have elicited a lot of debates on the role of microfinance towards poverty eradication. In addition, it has made the process of formulating policies on micro finance more complicated to the policy makers (Mosley, 2001). One of the most important assumptions in all microfinance programs is that it will result to more access to economic resources which will consequently result to the achievement of increased consumption of household goods and services hence economic well being (Hossain, 2008). There has been a lot of evidence to support that households experience improved access to goods and services after the intervention of micro finance institutions. The richer population is able to obtain loans with ease compared to the poor households. The rich may therefore continue getting richer and the poor poorer. It is observed that richer households are in a position to access more loans bringing the question of whether such loans made them richer (Noreen, 2010).

There are many arguments which tend explain that microfinance helps to reduce poverty. They say that micro credit improves entrepreneurship, especially to the poor households hence resulting to an increased level of income. Other proponents say that income from micro enterprises is good but they face some challenges like access to finance. It therefore means that in a household, credit advance can result to a lot of income. Despite all this, many people have questioned if the assumptions underlying the expected impacts on the lives of poor households are a result of participation in micro finance institutions (Khandker, 1999). Some even say that such assumptions may not hold hence it is a fallacy to say that microfinance can be said to contribute to the reduction of poverty. All the counter arguments have created a polarized debate concerning microfinance hence putting doubts on whether or not microfinance can be used to alleviate poverty not only in China but also in other countries.

The intended impacts of microfinance institutions may not be realized where policies are non-existent. There is a need to come up with policies that will govern microcredits so that they may achieve the targeted objectives. Microfinance institution should also look at other possible ways of reducing poverty other than giving microcredits. It has been realized that the outcomes of microfinance institutions are shaped by pre existing social economic infrastructure (Ghalib, 2007). It is not correct to base your results on few studies which dispute the fact that microfinance credit cannot be used to eradicate poverty.

Microfinance is believed to play a key role in mitigating the impacts of poverty. The microcredits they provide to the poor households enable them to make use of their entrepreneurial skills to generate income. The returns the get from investing microcredits acts as their constant means of earning a living. The challenge has been accessibility to such microcredits from microfinance enterprises. This means that if the finances are made available to poor households then there is a chance of empowering such households economically. Parties who oppose the fact that microfinance have helped reduce poverty in rural areas have said that there is danger which will be caused by policymakers and donors since they will withdraw or reduce resources from other policies so that they can put them in micro finance lending institutions (Ghalib et al, 2011). There is need for better research on the role of micro finance in rural development and poverty alleviation.

Is economic empowerment brought by micro finance institutions? One important question that needs to be addressed is whether an increase in micro entrepreneurship in rural areas both in China and other countries has been caused by economic empowerment from micro finance institutions.

When an entrepreneur establishes new businesses that create jobs, the level of economic wellbeing of the households is also improved. The truth concerning unrelenting increased of informal sole proprietorship business witnessed in rural is an indication of economic well-being.

There were some notable characteristic of rural areas in China. There is some limited productivity from inputs but not labor. The incidence of absolute poverty, where the households are unable to afford basic needs, is usually high among the rural populations. Three major stages of impacts can be deduced from rural areas as a result of micro finance institutions. These three stages are obtained through use of micro entrepreneurships. Many of the households at first engage in subsistence farming. This is to mean that a lot of their expenditure is on food. As a result of lack of roads and electricity in the rural areas, households consume a lot of their products. There is also the presence of disease, hunger and poverty.

There are some factors which households consider before choosing a micro finance institution. Firstly, Households choose the micro finance in which they will obtain credits from depending on utility preferences. They accept where that option gives them optimal satisfaction. Two reasons why households are key attractive areas for microfinance to extend credits to are the possibility of exploiting a good business, which is opportunity driven while on the part of households is survival. This is known as survival- driven- financing. Microfinance institutions are driven by supply. They are thus likely to thrive well in conditions where households are in much poverty. Households, for lack of options, have been faithful to uphold the prevailing conditions. They are also desperate to improve their living conditions through consumption and new entrepreneurships.

Some conditions have to be met before real improvement in income is experienced by the household. Some of these include the capability of entrepreneurship by the members of the household. Good movement should also be available to ensure goods and a service obtained from households obtains good market. The deal only benefits the households if the rate of return from microcredits exceeds the amount they pay for the loans obtained. The supply of essential needs to the Chinese people can be increased through being market oriented in the approach used to meet with these needs. In the modern days, a lot of microfinance institutions focus on the process of providing the poor population with micro credits so that they ensure such group of people experience labor productivity hence more incomes (Chowdhury et al, 2004). The model that is targeted to the poor society is known as the Joint liability lending (JLL). This is the group of the people who cannot borrow individually but have to borrow as a group together with other borrowers. The major participants in this system have to form groups which act as security of other groups loans. In such arrangements the groups are the one who are responsible with the repayment of the loan (Copestake et al, 2001). The loan extended is monitored by the lending institution. This study have tried to understand the means through which people in the rural areas of China have formed themselves into groups which they have used to access the loans from micro credit (Chowdhury & Bhuiya, 2002). It has also tried to understand how these groups have operated so that they can be in a position to access the loans. Finally, it has studied how the households have utilized the credit and the impacts towards them.

Perception of microfinance

Globally, it is believed that microfinance have been successful in reducing the rate of poverty (Dash, 2002). In the policy making process therefore more concentration has been on making loans affordable and available to many poor households in the rural China. In order to make some profit form their programs, microfinance institutions particularly the donors have certain fixed charges on the microloans they give (Deolalikar, 2002). The basic assumption in the study of microfinance is that microfinance is beneficial to the clients and so the most important thing is the process of making financial service accessible to many people. Murdoch (2002) identifies that for the microfinance institutions to be successful they have to be based on a win-win strategy where both parties have to gain. For the poor household to benefit, microfinance institutions must embrace the principles of good banking (Develtere & Huybrechts, 2002). This will help alleviate poverty. Murdoch (2002) says that it is possible for such institutions to operate by covering costs and at the same time help alleviate poverty.

Through the win-win strategy both the institution and the households have to gain. The microfinance institution have to follow good banking principles with the aim of obtaining some profit while the poor households benefits through accessing credit which helps them improve their living standards (Choudhury, 2001). One of the indicators which have been used to determine whether the loan extended to the poor is beneficial is the ability to repay. If they are repaying well, then it means the investments which they are undertaking are beneficial. This preposition further assumes that the amount of reduction in poverty is proportional to the total number of households accessed by the loans from microfinance institutions (Feng, 1997). The best practices of banking have been embrace by the major donors in this field who includes Consultative Group to Assist the Poorest (CGAP) which is a consortium of NGOs funded by the World Bank to help eradicate poverty (Mina & Alam, 1995). United States Agency for International Development (USAID) is one of the donor organizations that offer microcredit services to the poor. The other one is the United Nations Development programme (UNDP) (Goetz & Rina, 1996).

Despite all this the win- win strategy has been questioned by socially oriented service providers (Okpara, 2010). They have questioned the basic assumptions underlying this proposition. In fact they have question the validity of the assumptions.

in the year 1997, a meeting was held to deliberate on issues that need to addressed in the area of microfinance. A consensus that $billion should be mobilized within a time frame of 10 years was reached. This was meant to help microfinance organizations continue with their programs without any major challenge. Again the United Nations recognized the work done by microfinance institutions in 2005. The same year was termed as the Year of Micro-credit. The following year, Prof. Muhamad Yunus was given a Nobel Peace Prize because o his contribution towards microfinance programs. As a result of the publicity which has been given to the micro finance institutions, it has resulted to the creation of success in this sector (Gurung et al, 1997). In China much publicity has also been given resulting to improvement in the impacts of the loans extended to the poor Chinese. This is being done by the government and other donor institutions. Microfinance is not just assumed to improve the lives of the poor but it is well improved.

In the past it has been assumed that microfinance have a positive impact on the lives of the poor (Rahman, 2001). A lot of excitement about the success of success of microfinance which were known was based on few programs at the global level. There have been stories given of women experiencing poverty but their lives changes drastically whenever they are in a position to access credit from microfinance institutions (Panjaitan-Drioadisuryo, 1999). After obtaining the loan from such institutions, they have been in a position to start new business hence they are in a position to alleviate from poverty and afford better nutrition, education and health services (Hickson, 1997). According to many policymakers and donors, the rural poor household in China is in a position to borrow and repay meaning that the investments they are undertaking are good enough and benefiting them.

Research

The study was based on the villages in the rural areas of China. In choosing the village to be studied, it was based on whether it is valid or will be representative. Some of the criteria which were used were the ability of the villages to represent social, economic and cultural aspects of life in rural areas. Some of the programs selected included Funding Poor Cooperative (FPC) microfinance program which is run by Rural Development Institute of the Chinese Academy of Social Sciences. This is one of the microfinance programs which were used to make the study. Henan province is one of the selected areas of study. This province makes a big portion of the entire population of this country. It is also designated in one of the poverty.

In doing this, research was done on the people living in the north, central and southern China where microcredit facilities have been in operations. To come up with the effects comparison was done on the neighboring areas where microfinance programs have not penetrated. The research question focuses more upon explaining impact or effects of microfinance institutions on the lives of the poor rural households’ individuals in China. Quantitative analysis has been used to measure impacts but this has been complemented by qualitative techniques that attempt to explain the processes through which impacts actually occur. The research was draws upon the knowledge from a variety of sources, in particular from those living in poor rural households’ in the north, central and southern China. The theoretical approach was used in this academic analysis, which was being carried out in relation to this subject. This research aims at unveiling how microfinance has impacted on the lives of poor people living in China as well as vulnerability to poverty. The specific focus is given on the development of the best practice models for microfinance in china.

Impacts in poverty reduction

Globally, there is an impression microfinance is successful in the reduction of poverty that (Reddy, 2000). Policy makers are keen to come up with policies that will enable microfinance programs be more effective than they are currently. The donors and major stakeholders of this program have argued that can be of more benefits if it reaches large group of people.

For any of the microfinance to be determined whether it is successful or not, three different characteristics like sustainability outreach and impact (Holcombe & Xu, 1997).

The first micro finance program to be put in place in China was done in the early 1980s although the progress has been slow. This has been caused by low interest rates making the financial institutions not being in position to recover costs incurred in giving out the loans. This has caused the program not to be sustainable.

The impacts of microfinance

Information about the impacts of micro finance is not usually available. Some have doubted whether microfinance institutions can be used to fight poverty but others have also agreed to the fact that services offered by such institutions can help to reduce poverty (Sengupta & Aubuchon, 2008). There are different areas in which microfinance institutions can help in the reduction of poverty especially to the poor.

One of these areas is the physical assets. The reduction of poverty is done in a circle involving more income, more credits extensions and extra investments. Good lending programs improve the lives of the poor people as it helps to increase their income below the poverty lines (Setboonsarng & Parpiev, 2008). The level of borrowing is related to the level of income hence making the poor to benefit more. The income gained helps the people to diversify their sources of income while others are more likely to specialize in their engagement in productive activities (Shamsuddoha, 2008). The program will help the poor to accumulate assets resulting to increased income.

Studies which were done in China indicate that microcredit programs aimed at women have helped to improve human capita. This study was done on six microcredit programs. The programs have caused increased expenditure on consumptions and education as well as the health sector. These programs are also known to increase the rate of enrollment to school (Swope, 2005). With respect issues related to education, there is presence of a good relationship of women involvement in microfinance programs and enrollment rates to schools. This is due to the fact there is some inclusion of education programs in the microfinance programs. The programs offer training opportunities to women so that they can be in a position to acquire skills. This is evidenced by the fact that more than 70% of the participants in this microfinance activities have been in a position to acquire new skills (Yan, 1997). Another research found out that participation in microfinance activities have motivated farmers to learn new skills of farming hence improved agricultural productivity (Yan & Wang, 1997).

In addition, studies done in China have also shown that microfinance program have resulted to women demanding their own healthcare program as well as child nutritional programs.

Micro finance programs have a lot of impacts on social capital (Shah, 2009). This is the interaction part of the people and also includes norms and values. A study which was done in China found come up with tangible evidence that micro finance helps in increase of risk management by enhancing of social capital (Mosley, 2002). Most of the cases which were studied indicated that those who participated have been in position to share market information, changes in price and technology as well as being in a position to pool resources and sharing of such resources (Mosley, 2002). The programs have made the members to form groups which help each other in making contributions towards each other at times of needs.

It is known that by targeting of women through microfinance programs, it can help in improving their economic status in the household contexts as well as the community at large (Subrahmanyam, 2000). The programs are known to increase the mobility of women and have also given them freedom from family issues and violence. Moreover, they have given them security in terms economic issues and enabled them to be in a position to their own purchases (Schuler & Hashemi, 1994). The two authors also found out that micro finance programs helps to reduce isolation of women hence helping them progress their economic or social status. There are different models which can be very successful and others are not effective. Hulme (2000) proposed the development of microfinance systems which are favorable to the prevailing local conditions.

In China it has also been seen that self- help group started by microfinance programs have enabled women to participate in the political processes. They have enabled the people to air their needs to the government as well as holding power at different local levels.

Economic impacts

One of the notable changes is the ability to overcome conservative economic constraints which were traditionally embraced (Sebstad & Gregory, 1996). The provision of microfinance services to the local rural households have resulted to low demand for labor together with products and services. The programs are also known to stabilize the income of the residents of such areas hence reducing the poverty levels (Bai, 2001).

A lot of research done on the effects of microfinance in rural China has concentrated on sustainability obtained from microfinance programs and how the government policy has impacted on such programs. A lot of studies have shown that microfinance programs have resulted to increased incomes (Bai & Youli, 1997). A research done by the United Nations International Fund for Agricultural Development indicated that the borrowers experienced reduced poverty levels as a result of participation in microfinance programs. This was noted to decrease by between 8% and 20% in a period of four years. On the other hand, returns obtained from investment funded through micro finance programs increased with a range of 4% and 13%. Another study done indicated that engagement in microcredit program has made women to become entrepreneurs hence being in a position to start small enterprises like farms and other business. This has in turn resulted to the creation of employment to the rural people resulting to elevated standards of living (Holcombe & Xu, 1997). A good example is in Hebei province where the number of people who left the village to go and look for work reduced. This is attributed to the employment which has been created by micro finance program. In addition, they have resulted to increasing number of labor migration from three ten to fifty in a span of two years. Another research which was done in the mountainous west part of China developed good conclusions about the impact of microfinance on the lives of the poor. This is one of the areas where a large percentage of the poor population lives. It was noted that they have created a large productive investment chances to the people of these areas. However some challenges have been faced in offering of microfinance programs. The poor ones are considered to have high risks associated with low returns.

Women the rural areas of China are more disadvantaged than any other group in this country. They are regarded as those of low status, have minimal education opportunities and less economic welfare. On participating on such microfinance programs, it has been shown they have been in a position to increase their social status as well as ensuring a sense of personal responsibility. It has also created capacity to women.

Another major crisis in the rural areas is health crises causing a lot of debts to the people of these areas. Despite this, there is a great relationship between health and economic security. With the introduction of microfinance programs there is an improvement in health care and nutrition issues. In another province known as Qinghai it is evident that microfinance has resulted to welfare benefits mostly in cases of emergency. Loans obtained from micro finance programs have been used to improve welfare needs for the poor Chinese through provision of emergency funds. The program participation has also improved the standards of living (Cheng, 1997).

More studies have been done on the effects of micro finance in south-west China. One key observation was that in some areas there is a lot of social discord especially to some communities (Cheng, 1997). This social discord has brought a lot of negative issues in terms of social dynamic (Tsien, 2002). But with the introduction of microfinance loans, such discords have declined due to the fact that they create income equalities. Other studies have indicated that there has been social solidarity resulting from the use of the program. Moreover, it has shown an improvement in social position (McLean, 2003).

Assessment on the housing conditions has been done on the current housing conditions in the rural areas of southwest China. There has been a notable difference in the current conditions as compared to the previous conditions when there was no microfinance programs (Zheng, 2001). Due to the good housing which has been witnessed as a result of the people engagement in the microfinance programs, the housing improvement has contributed on the emotional well to the Chinese living in the poor rural areas (Cheng & Nguyen, 2000). According to other researches which has been done have shown that the income of the Chinese living in the rural areas has been increasing as a result of extension of microfinance loans. The microfinance has also resulted in low interest lending even by other institution (Sun, 2002). Where there has been combination of microfinance loans and issues of environment, it is notable that it has resulted to better and positive environment conservation (Markus, 2002).

The introduction of microfinance programs in the rural China has helped to reduce income and food vulnerabilities through the provision of production expansion in such areas (Wu, 2001). They have also resulted to enhancement of income and the reduction of income gaps.

A lot of research that has been done on the impact of microfinance in China concentrates on how institutions can sustain themselves through the help of microfinance institutions (Tsien, 2002). Research has also been done to show how the lives of people living in rural and urban areas have been changed through participation in microfinance programs. Government policies that govern the operations of microfinance have also been widely discussed by many scholars (Wu, 2002). Most of these reports are written by third parties and very few have been written by those mandated with implementing microfinance programs or those who fund these institutions. Consequently, most of these reports are biased and do not capture everything there is to know about the positive impact of these microfinance institutions in the lives of poor people. The reports also fail to highlight most of the negative effects of these institutions because the Chinese culture forbids people from admitting that they have failed in achieving a set target. Therefore, most of the reports that highlight the successes of these microfinance institutions are no truthful because they tend to exaggerate the success rate of the institutions. Very few cases of actual assessment on the success rate of these microfinance institutions in china have been done. Mot of the literature available has been compiled from mere observation. China is one of the countries that are experiencing speedy growth in their economy. However, the studies conducted on this area are not convincing enough in attributing this growth to the presence of various microfinance institutions in the country. Therefore, most of these reports do not fully reflect the actual situation on the ground.

Income and unemployment

Most of the research that has been done on this area concludes that the incomes of the participants who solicit the services of microfinance increase significantly compared to those people who do not. A study done by United Nations International Fund for Agricultural Development (IFAD) shows that the poverty level of those who had borrowed money from microfinance reduced significantly by close to 20 percent. This happened over a period of four years (IFAD, 2002). Additionally, there was an increase in the returns of investments whose owners had borrowed money from microfinance. Moreover, microfinance institutions offer women funding which enables them to become small entrepreneurs. This helps them to put up small enterprises for instance rearing of chicken, which may offer others employment (Kabeer, 2002).

Although there is a significant increase in the level of income for people who participate in these programs, it has not been possible to measure the actual change in income for the beneficiaries (Liu & Zhang, 1997). The beneficiaries of these programs are not usually truthful in reporting their income as most of them tend to give a lower figure than the actual amount. The real impact of microfinance on poor farmers is not able to be measured accurately because of factors such as the constant change of climate leading to differences in crop harvest. Therefore, there is need for the study of income change to be done over a period of several years.

Microfinance has helped to fund the setting up of small enterprises in rural areas in China. This has led to the reduction of the number of people migrating to urban areas in search of employment. People prefer to stay in the village and work there instead of going to look for jobs in urban areas (Zhang,1997).

Microfinance programs have profound impacts on the poorest among the Chinese population

A large number of people living in the mountainous west of china are the poor. This is also the region where most microfinance institutions have their operations. Nevertheless, there have been arguments which have been raised citing that microfinance institutions serve the interest of the rich and not the poor (Zhao, 1997). This happens because microfinance institutions feel that there is a higher risk involved in giving poor farmers loans compared to giving the rich. Therefore, they feel that it is safer for them to give the rich instead of the poor. The study by IFAD also indicates that microfinance institutions in China have not been effective in reaching out for the poor. Most borrowers of loans from these institutions are, therefore, the people who are well-off. People who are very poor do not have access to such loans because they may not be able to pay back.

Savings groups in China, which enable people to access microloans, usually comprise of people who have some degree of education, training and experience (Zuo, 2000). Those who lack these and other assets are usually locked out from accessing these loans. These people who are locked out are mostly the ones in dire need of the loans because they are the poorest.

However, there are reviews that indicate that some microfinance institutions try to include even these people who are locked out because of their poverty. The results show that even these people can take part in these programs successfully if given a chance. Therefore, microfinance institutions should not entirely lock out the poorest but should look for a way of reaching out to those who are poor but reliable in order to empower them economically. This will help the poor improve their living standard through engaging in income generation projects.

It is important for the Chinese people to diversify their sources of income. This will help in increasing their sources of income hence improving their living standards. Microfinance programs in China have played a major role in helping the people diversify their sources of income. This has been possible through the setting up of new income generating activities. The money borrowed by people living in Yunnan and Sichuan is mostly used to set up new income generating activities as well as boosting the existing activities. Using the money borrowed in diverse income generating activities helps to reduce the risk of losing all the money if it is invested in a single project.

Women participate largely in microfinance programs either as individuals or in groups. Women living in poor areas of China face various challenges. One of these challenges is lack of economic empowerment. They have little or no access to resources that can help them improve their economic status. However, participation in microfinance programs has been one of the avenues that these women have used to be economically empowered. One advantage that women have over men when it comes to dealing with microfinance programs is that women are deemed more honest than men. When the mother is the custodian of family money, it is more likely that everyone will enjoy the benefit than if the father is the custodian. Therefore, these institutions prefer to give loans to women than to men. Although this has been the trend in China, questions have been raised about the effectiveness of giving loans to women by microfinance institutions. This happens especially during repayment of these loans whereby some women are not able to repay the loans.

Microcredit has a profound impact on the human capital – education, health & well-being of the people living in the poor areas of China. People living in these areas of China face various heath challenges. This is one of the reasons why these people continue to live in debt. Through participation in microfinance programs, people living in these poor areas have been able to increase the money they spend on nutrition and healthcare resulting to improved health (Shaohua and Ravallion, 2010).

In addition, participation in these programs has led to high rates of enrolment in institutions of learning. This has been the case especially because one of the components of these programs is women education programs. Women who take part in microfinance programs are usually taken through various trainings which help them to acquire new skills. Moreover, they are motivated to learn other skills which may help them improve the way they live as well as their income generating projects.

In some provinces such as Qinghai, welfare benefits for the residents have been linked to microfinance. This is especially during periods of emergency. Of all the loans given out, 17% were directed towards needs relating to welfare. Participation in various programs has also resulted to the improvement of living standards among the people.

Social capital

Social capital is commonly found among communities that have strong kinship ties or a common history. However, there are certain areas in China which despite having a shared history, social discord is very rampant. Introducing microfinance programs in such areas would lead to exacerbating of this situation because it may lead to inequality in the levels of income and wealth among these communities. Therefore, it is important for microfinance institutions to consider the social cohesion systems of the people before embarking on any programs. In areas where there is no social cohesion, programs started by microfinance institutions may not be successful.

Efforts by microfinance institutions to give loans to groups in China have been hindered by some members of these groups failing to repay the loans. In most cases, members of these groups are not willing to help the defaulters to pay these loans. This makes it hard for these institutions to continue lending money to groups to boost their businesses or to start income generating activities. However, in instances where members of a group support one another, enhanced social capital is the end result.

Microcredit also impacts on the structures of housing found among the poor people in China. For many people living in the poor areas of China, a house is not only a place of residence for the family members but also a place where income generating projects such as rearing of chicken are situated. The kind of a house one lives in also shows their social status to an extent that it plays a role in determining the marriage opportunities of a person. When people from these poor areas receive loans from microfinance programs, one of the things they do is to upgrade their houses.

Other impacts

The interest rates on loans given by microfinance institutions are usually lower than other loans. This means that more poor people can have access to these loans than to loans offered by banks. In some programs, microfinance institutions combine their activities with activities related to environmental conservation. This leads to a clean environment free from pollution.

Although microfinance institutions have tried in their implementation of projects that help to alleviate poverty among the poorest and the vulnerable in China, there are several methodological issues that have been encountered. Microfinance institutions in China use the model followed by Grameen Bank. This is not very effective the Chinese context. This is because the approach and structure of administration of the Grameen Bank are not compatible with the ones found in China, especially in the countryside where most microfinance institutions are based. The government of China recognizes the village as the lowest organizational level. However, for the Grameen model, a group of 30 people is required for the microfinance to give out loans. Where people organize themselves into groups of 30 people to get loans, efforts to hold weekly meetings are hindered by the attendance of the whole village. This makes it hard to deliberate on any issues concerning microfinance programs. Therefore, many people opt out of these groups because they realize that it may not be possible to make any progress in these groups. In addition, many people living in these poor areas of China are not willing to be part of any group because they fear that some may fail to pay back the loans. For those willing to be part of these groups, through screening is done before one is allowed to take any loan. This ensures that only reliable people are given loans. Those in these groups are at an advantage because groups enable the sharing of technical skills as well as useful information regarding employment and marketing of their products. This is very useful, particularly to the members of these groups since most of them are the poor and need this information to boost their businesses.

Another disadvantage of this model is that initially, it was meant for the people of Bangladesh who lived in lowlands and had steady sources of income although very little. Applying this model to the poor people in China may not be very practical since the land there is mountainous unlike in Bangladesh. This means that attending regular weekly meetings for the poor Chinese may not be easy due to the regions where they live. Moreover, the poor Chinese populations living in these mountainous regions are farmers whose income is not regular. This is because they depend on how the seasons will turn out to be. Additionally, they are faced with the challenge of getting ready markets for their farm produce. However, people who have joined these groups in China struggle and manage to get weekly incomes which they use in the repayment of these loans. Instead of holding weekly meetings as required by the Grameen model, the Chinese groups meet less often. Most microfinance programs therefore, alter the Grameen’s model in order to suit the people’s needs depending on their conditions. Despite these efforts by microfinance institutions to try and alter this model to fit the Chinese context, there is need for the introduction of other models because China is very large and diverse.

Another alteration that has been made on the Grameen’s model is making it possible for members of the same family to join the same group. In addition, men and women are allowed to join the same group.

The use of village agents in the running of microfinance programs was found to be more effective than using agents at the town level. One of the reasons why this was found to be effective was because it is hard for the people working as agents in villages to be moved from one region to the other. However, with the town agents, there is a likelihood of being moved to other positions in the government. Moreover, agents from the town may not articulate the needs of the rural people as effectively as the village agents would.

To complement the work done by microfinance institutions in helping the poor, it is important for these people to be given training in agricultural activities. This will help the people develop new ideas for their income generating projects. They will also be able to increase the output of the already existing projects though the use of improved farming methods and better quality seeds. Banks such as Agriculture Bank of China have been on the front line in making loans easily available to poor Chinese farmers. Their loans have low interest rates and flexible time for paying back the loans. In a bid to ensure that poor farmers have access to these loans, the bank has lowered its transactions costs. By the end of 2008, over 5 million farmers had been given loans by this bank (Chen et al, 2010).

Various types of microfinance institutions exist in China. They include public interest and mutual microfinance. These institutions are very important in the lives of the Chinese people, particularly the poor. This is why the Chinese government has continued to improve their policies in order to ensure that there is a favorable environment for microfinance institutions to thrive. In China, microfinance services do not extend to services such as savings or transfer of payments. Most microfinance institutions operating in rural China target the poor people, particularly the farmers. In urban areas, they target the people who do not have any form of employment as well as those who own small and medium scale enterprises. This is aimed at economically empowering the vulnerable and those who are poor. The institutions also help in empowering college graduates who are unemployed as well as the disabled and people who have been laid off from their places of work. These are the people who make up a great percentage of the unemployed and vulnerable population in urban centers. The major challenge for these people is lack of stable sources of income which can enable them to access loans from banks. Consequently, it is hard for these people to set up a business which can give them income to sustain themselves. Loans given by microfinance institutions help in empowering these people through establishment of income generating activities. Micro guarantee loans by some commercial banks also help in making credit financial services available to the people. Therefore, unemployed people are able to start a business that can help to boost them economically.

Methodology

The empirical objectives of the study will be addressed by collecting secondary data regarding The Impact of Microfinance on Rural Poor Households’ Income and Vulnerability to Poverty, A Case Study of China Poor Population. The time series data is used to assess the impact of microfinance on variables related to household income and vulnerability to poverty. The main challenge has been gathering the data that is needed to complete this analysis. The main assumption that has been made in this study is that the poor population in china obtains credit facilities from microfinance institutions in order to start small businesses in rural and urban centers in the country. The analysis, therefore, is relating the data for loans available to poor households to the number of small enterprises they start up. This will be regressed against other variables like poverty level, households’ income, population living in rural areas and any other relevant variable. The rate of movement to urban centers is manly to startup businesses and an indication of improvement in livelihood. The first relationship to be investigated is that of microfinance and poverty rate. In this case, the number of businesses that are established in china by the poor population will represent the presence of microfinance and its effects on the poor population vulnerability to poverty. If the poor population would establish income generating businesses, then their vulnerability to poverty will be reduced.

The second relationship to be investigated is that of poverty rate and level of lending by microfinance. Poverty level will be the dependent variable while lending level will be the independent variable. This will investigate if amounts of loans given to poor population by microfinance institutions have a significant effect on the poverty level in China.

To investigate the impact of microfinance on the households’ income of the poor population in China, the relationship between small businesses started in china and growth of rural household income. The relationship between the amounts of loans out to poor Chinese population and growth of household income will also be investigated.

The relationship between growth of household income and poverty rate will also be used to assess whether microfinance has significant impact on poverty alleviation. The setting up of projects with the help of loans from microfinance helps in increasing the income.

Data analysis will be done using regression analysis. The simple regression analysis will be used because of the nature of the data that was collected. The estimation of regression line will be done using Eviews statistical software. The significance of the independent variables to the dependent variables will be tested using student t distribution test.

Data Analysis and Results

As mentioned above, data will be analyzed using simple regression analysis because the data that was obtained does not allow multiple regression analysis. The Eviews statistical software will be used to estimate the regression lines. All variables will be tested using t-test and 95% level of confidence. The level of significance α = 0.05. The relationships that will be analyzed are represented by the following regression lines:

Microfinance (Number of small businesses) (X) and poverty rate (Y)

The dependent variable this case is the level of poverty among the people. On the other hand, the number of businesses represents the independent variable. Thus, Y = β0 + β1X, is the model to be estimated, where β0 and β1 are regression coefficients.

The Eviews output for this data is as follows:

The regression line estimated will be Y = 59.21830 – 0.001959 X.

This can be represented using real variables as follows:

- Poverty Rate = 59.21830 – 0.001959 (Number of small businesses)

The test details are as follows:

- Y = 59.21830 – 0.001959 X

- S.E = 4.463026 – 0.000207

- T-statistic = 13.26864 9.453177

- The critical value of t at α = 0.05 and 9-1= 8 degrees of freedom is 2.306.

The hypothesis being tested are stated as follows:

- H0: β = 0 meaning that X is not a significant determinant of Y

- H1: β ± 0 meaning that X is a significant determinant of Y

The decision rule using t-test is that the null hypothesis is rejected when t-statistic is greater t-critical. In this case, the value of t-statistic (9.453177) > t – critical (2.306), meaning that the null hypothesis H0 is rejected. The conclusion is that X is a significant determinant of Y.

The coefficient of determination (Adjusted R2) is 91.6980%. This means that the independent variable X explains 91.6980% of variation in Y. The remaining part 8.302% is explained by other variables that are not included in the model.

Microfinance (Lending level) and Poverty rate

The other aspect of microfinance that will be tested is the lending level. The impact of lending level on poverty reduction is investigated in this case. The poverty rate is taken to be the dependent variable (Y) and lending level is taken to be the independent variable (X). The regression line that is estimated is Y = β0 + β1X, where β0 and β1 are regression coefficients.

The Eviews output for the above data is as follows:

The regression Line is estimated as follows: Y = 20.71895 – 0.004766 X. This can also be represented as follows: Poverty Rate = 20.71895 – 0.004766 (Lending Level)

The test details are as follows:

- Y = 20.71895 – 0.004766 X

- SE = 4.608682 0.002674

- T-statistic = 4.495635 1.782783

The hypotheses to be tested are as follows:

- H0: β = 0 meaning that X is not a significant determinant of Y

- H1: β ± 0 meaning that X is a significant determinant of Y

The critical value of t at α = 0.05 and n-1 (8-1) = 7 degrees of freedom is 2.365. The t-statistic is smaller than t-critical. This means that the null hypothesis will not be rejected. This indicates that X is not a significant determinant of Y. The alternative hypothesis is rejected in this case.

The coefficient of determination (R Squared = 0.237333) reveals that the 23.7333% of variation in Y is explained by X. the other variation is explained by other variables that are not part of this model. The variable X explains a very small portion of variation in Y. it is not a significant determinant of Y.

Microfinance (Number of small businesses started) and household income

This investigates whether microfinance has a significant impact on the household income. Household income is taken to be the dependent variable (Y) and number of small businesses represents the independent variable (X). The regression line to be estimated is Y = β0 + β1X, where β0 and β1 are regression coefficients. The sample used in this analysis is rather too small because the data is not available for other years.

The Eviews output is as follows:

The regression line is estimated as follows: Y = -57.93483 + 0.003413 X.

Household income = – 57.93483 + 0.003413 (Number of Small Businesses).

The rest details are represented as follows:

- Y = -57.93483 + 0.003413 X

- S.E = 6.094541 0.000270

- T-statistic = 6.094541 12.65308

The hypotheses to be tested are stated as follows:

- H0: β = 0 meaning that X is not a significant determinant of Y

- H1: β ± 0 meaning that X is a significant determinant of Y

From the T- distribution table, the critical value of t at α = 0.05 and n-1 (3-1) = 2 degrees of freedom is 4.303. T-statistic is greater than t-critical. This means that the null hypothesis H0 is rejected and alternative hypothesis H1 taken into consideration. This shows that X is an important determinant of Y.

The coefficient of determination R Squared (0.987585) shows that the variable X in the above model explains 98.7585 of the variation in Y. this shows that X is a strong determinant of Y in this regression. Only a small portion of the variation in Y is explained by other variables not included in this model. The t-test confirmed this fact because it found X to be a significant determinant of Y.

Household income and poverty level

The relationship between household income and poverty level is also investigated. The household income is believed to come from businesses that are started from microfinance loans. The literature review showed that poor population in china look for loans from microfinance to start small businesses. The relationship to level of poverty also determines the role that microfinance has on poverty alleviation. Poverty level is taken to be the dependent variable (Y) and household income represents the independent variable (X). The regression line to be investigated is Y = β0 + β1X, where β0 and β1 are regression coefficients.

The Eviews output is as follows:

The regression line is estimated as follows: Y = 25.83007 – 0.521638 X.

Poverty Level = 25.83007 – 0.521638 (Household Income).

The test details are listed below:

- Y = 25.83007 – 0.521638 X

- SE = 1.496375 – 0.058085

- T-statistic= 17.26176 8.980559

The t-distribution statistic at α = 0.05 and 7 degrees of freedom (n-1 = 8-1=7) shows a critical value t = 2.365. This indicates that the null hypothesis will be rejected. The conclusion is that X is an important determinant of Y. The alternative hypothesis is, therefore, accepted.

The variable X was found to be a significant determinant of Y. The coefficient of determination (R Squared = 0.919216) also reveals that X in the above model is a strong determinant of Y. R2 = 91.9216% means that 91.9216% of the variation in Y is explained by X. Other variables that may have been omitted from the model explain only a small portion of variation in Y.

Microfinance (Number of small businesses) and population of rural poor people in china

The last relationship to be investigated is that of microfinance and population of poor people in rural China. The regression analysis is done for the number of small businesses started from microfinance loans against the population of poor people in china. The population of poor people in China is the dependent variable (Y) and the number of small businesses is the independent variable (X). The regression line to be estimated is Y = β0 + β1X, where β0 and β1 are regression coefficients.

The data was distributed as follows:

The Eviews output is as follows:

The regression line is estimated as follows: Y = 194.2205 – 0.007708 X.

Population of poor people = 194.2205 – 0.007708 (Number of Small Businesses).

The test details are as stated below:

- Y = 194.2205 – 0.007708 X

- SE = 37.91854 0.001806

- T-statistic = 5.122045 4.267783

The hypotheses that are tested are stated below:

- H0: β = 0 meaning that X is not a significant determinant of Y

- H1: β ± 0 meaning that X is a significant determinant of Y

From the t-distribution table, the critical value of t at α = 0.05 and n-1 degrees of freedom is 2.571. Where n = 6 and, therefore, df = 5. The t-statistic is greater than t-critical. The null hypothesis is, therefore, rejected. The alternative hypothesis is accepted and conclusion made that X is a significant determinant of Y.

The value of the coefficient of determination R Squared is 77.4916%. This means that the variable X explains 77.4916% of the variation in Y. The other variation (100% – 77.4916 = 22.5084) that is unexplained by the model can only be attributed to other variables that are not part of this model.

Discussion of the Results

The study sought to investigate the Impact of Microfinance on Rural Poor Households’ Income and Vulnerability to Poverty. The investigation uses a Case Study of China Poor Population. The term microfinance was identified as the provision of financial services to the poor. Financial services from conventional banks are not readily available to the poor people due to the many requirements that they are not able to meet. The most common form of microfinance is microcredit. This is the provision of small loans to the poor population of a particular economy. It is the key component of microfinance programs. The poor population in China is in high demand of microcredits in order to start small businesses and meet life expenses. The main question in the study is to investigate whether microfinance significantly impact on the rural households’ income and their vulnerability to poverty. The concept of microfinance entered the model through the small businesses that are started by the borrowers of microcredit and the level of lending. These two aspects of microfinance are regressed against variables such as growth of rural households’ income, the percentage of people living under $1 per day, and the population of poor people living in rural china. Each of the two aspects is regressed against these other variables from their relationship to be investigated.

The relationship between the number of small businesses and the number of people living under $1 per day is used to assess the extent to which microfinance has impacted poverty level among the poor people in China. The number of people living under $1 per day are said to be living under poverty line. The relationship between lending level and poverty rate is another also played a big role in achieving the research objectives. The lending level represented the role the microfinance play in supporting the poor communities start up small businesses to help them earn a living. This is done through the provision of microcredit. This helps in reducing poverty rate and also makes the population less vulnerable to poverty because they are able to establish income generating projects. The relationship between the number of businesses established and income level was also investigated. The assumption that was made here is that the microcredit that is given to these poor people in the community is used to start up small businesses. The study investigated whether starting these small businesses will significantly impact households’ income. Household income and poverty level were also investigated and their relationship established. Household income is one of the ways that were used to determine the impact of microfinance on poor people’s lives. The last relationship that was investigated was Microfinance (Number of small businesses) and population of rural poor people in china. The study investigated whether the number of businesses started using microcredits would significantly reduce the number of people living in poverty in China. The results for all these objectives are discussed below.

Microfinance (number of small businesses) and poverty rate

The regression analysis was done between the two variables, number of small businesses and poverty rate. The poverty rate was taken as the independent variable and number of small businesses taken as the independent variable. The analysis revealed that the number of small businesses is a significant determinant of poverty level. The coefficient of the regression line (Y = 59.21830 – 0.001959 X) indicated that the two variables have an inverse relationship. The level of poverty decreases as the number of small businesses increases. The coefficient indicates that when the number of small businesses increases by one unit, the level of poverty decreases by 0.001959 units. The poor people in china are able to start small businesses from the micro credits that they obtain from microfinance. These businesses give them a reliable source of income and they are able live above the poverty line. Their vulnerability to poverty is reduced when availability of microcredits is ensured. The model used to investigate this relationship revealed that 91.6980% of the reduction in poverty is as a result of small businesses that the beneficiaries of microcredit start up. The results showed that 91.6980% of the variation in poverty level is explained or is attributable to the number of small businesses established through microfinance.

Microfinance (Lending level) and Poverty rate

The second relationship that was investigated is between lending level and poverty rate. The results showed that the lending rate is not a significant determinant of poverty rate. It explained only explained 23.33% of the variation in poverty rate. The t-test conducted did not reject the null hypothesis. The alternative hypothesis was taken which stated that lending rate is not a significant determinant of poverty. The regression line estimated (Y = 20.71895 – 0.004766 X), however, indicated that there is an inverse relationship between lending level and poverty rate. According to the coefficient of regression, when the lending level of microfinance increases by one unit, the rate of poverty decreases by 0.004766 units. However, this impact is not significant because the test revealed that lending level is not an important determinant of poverty rate it is, however, known from theory that when lending rate of microfinance increases, many people will be able to start income generating activities which will reduce their vulnerability to poverty. Poverty rate is expected to reduce with increase in lending level and this is the case with the research results. A big variation in poverty rate according to this model is explained by other factors that are not included in the model.

Microfinance (Number of small businesses started) and household income