Introduction

The importance of researching the current trends in how supply and demand of Russia gas in UK interrelate with each other can hardly be underestimated, due to the fact that there are many objective reasons for consumption of natural gas in this country to significantly increase, during the course on next few years, which has clear geopolitical implications for UK, as one of major European powers. Despite the fact that utilization of natural gas has been traditionally discussed within a context of such practice being of purely economic and technological essence, the realities of 21st century’s living imply strong geostrategic overtones, for as long as discussion of issues related to consumption of natural gas is being concerned.

The validity of this thesis has been illustrated in the winter of 2009, when gas-related dispute between Russia and Ukraine had resulted in ensuing “energy panic” among Eastern European nations. In her article “Russia gas dispute puts Europe in the deep freeze”, Isabel Gorst states: “The year 2009 was the first time that deliveries of Russian gas through Ukrainian transit pipelines completely halted, depriving the EU of one fifth of its supplies” (Gorst 2009, p. 4). Given UK’s membership in EU and also the fact that ever since 2005, Great Britain became the net exporter of natural gas due to depletion of natural gas deposits in United Kingdom Continental Shelf (UKCS), it will be logical, on our part, to suggest that during the course of next few decades, our country is going to be increasingly affected by the dynamics on European market of gas. In their turn, these dynamics will be defined by:

- Ability of major suppliers of gas to Europe to stick to their contractual obligations.

- Objective socio-political and technological preconditions that would account for fluctuations within natural gas’ supply/demand ratio in Europe in the future.

The discussion of both factors can hardly avoid mentioning Russia as one of the major gas suppliers to Europe. As of 2008, the percentile ratio of Russian state-owned corporation Gazprom’s supplies of natural gas to countries of EU accounted for 25%. Despite the fact that in the same year, Britain’s consumption of Russian gas amounted to only 2%, there are many good reasons for us to believe then, within a matter of new few years, this percentage will increase dramatically. By the year 2015, Gazprom aims to control at least 20% of UK’s market of gas. And, as we will prove later in this work, such Gazprom’s plans are not being altogether deprived of rationale – it is not only that there are many purely objective factors that should account for annual increases in percentage of Russian gas being circulated within British energy sector, but also subjective ones as well.

Even though that, while being in position of political power, British Laborites had initiated many “socialist” reforms, concerned with the process of government assuming control over certain aspects of nation’s political and economic life, they have simultaneously liberalized the energy sector of British economy even to a greater extent then it was the case under Conservatives. In his article “Britain’s energy future”, Simon Hughes is making a perfectly good point when he states: “Tory and Labour have set up and continued a privatized energy industry where those who consume least pay most” (Hughes 2009). Given the fact that, during the course of Laborites’ reign, the dynamics on UK’s energy market had been increasingly defined by an ongoing process of corporate consolidation, British largest energy providers are now being endowed with a completive advantage over their smaller rivals, due to these providers’ ability to sign direct interruptible contracts with Gazprom and with Norway’s gas-exporting companies.

In its turn, this creates a paradoxical situation – despite the fact that in recent years the political relations between Russia and Britain have been marked by strongly defined animosity, commercial ties between these two countries continue to strengthen, as time goes by. This trend fully corresponds to practical essence of Globalization, as the process of large commercial and financial organizations assuming quasi-independent functionality. Such our thesis will serve as theoretical framework for this study, as a whole.

Aim and Objectives

In this work, we will aim at accomplishing the following set of objectives:

- Analyzing the key issues that affect trends, concerned with supply and demand of Russian gas to UK’s market. While researching the subject matter, we will also strive to provide readers with the insight on how the factors, defining fluctuations within Russian gas supply/demand ratio in UK, came into being in the first place. Moreover, we will also aim at accentuating the objective and subjective subtleties of these factors, in order for us to gain a better understanding as to how Britain’s policy-makers should address the challenges and opportunities, associated with the presence of Russian gas in UK’s energy system.

- Analyzing the present situation with consumption of natural gas in UK by corporate bodies and private citizens. While pursuing with the task, we will focus on exploring what causes British commercial operators and private citizens to consider activities, associated with gas consumption, as an integral component of their operational/existential modes.

- Explaining PESTEL issues that affect both: a) situation with supply and demand of Russian natural gas in UK b) Gazprom’s ability to stick to its contractual obligations, in regards to British consumers of Russian natural gas. While addressing these issues, we will also strive to outline general tendencies, which will affect such issues’ dynamics in the future.

- Providing readers with a forecast onto future developments within UK’s market of natural gas. In order for us to be able to achieve this objective, we will need to take into consideration a variety of different social, economic and political factors, which are the most likely to affect the process of shaping up Globalized geopolitical realities in EU, in general, and in Britain, in particular.

- Recommending British governmental officials as to what would account for the best course of action, on their part, while facing challenges and opportunities, associated Gazprom’s activities on UK market of natural gas. While coming up recommendations, we will make point in stressing out these recommendations’ hypothetical essence, so that this study would not be associated with any legally bounding implications.

Dissertation Structure

The structural values of our study derive out of the subject matter, with which this dissertation is being primarily concerned – namely, the analysis of factors related to supply and demand of Russian gas in UK. While researching this topic, it is the matter of crucial importance to assure that we approach our task in most thoroughful manner. This is why we have made a point in adjusting the structure of this dissertation to correspond to the foremost principles of qualitative research. That is – we will aim at collecting as much relevant data as possible, in regards to discussed issues, before analyzing the practical implications of this data. Also, given the analytical essence of this study, its substantial volume will be solely dedicated to discussion of how an obtained data may provide us with the insight on things to come, within a context of how dynamics on UK’s market of natural gas are being formed. The following is the general outline of this dissertation’s structure:

- In this part of our study, we will embark upon: a) Providing readers with the insight onto conceptual premise of this work, b) Defining study’s primary aims and objectives, c) Outlining dissertation’s structure, d) Validating our choice for this work’s methodological rationale, e) Outlining the principles of methodological approach, which we will utilize while dealing with the subject matter, f) Defining what would account for primary and secondary values of the data that will be obtained during the course of a research.

- This part of our work will be dedicated to: a) Introducing readers to the set of considerations, which define our choice for the literature that is going to be reviewed, b) Reviewing literature concerned with Theme 1 (Current situation with supply and demand on UK market of natural gas), c) Reviewing literature concerned with Theme 2 (Russia as an exporter of natural gas to UK).

- In this part of our dissertation, we will analyze issues that surround Gazprom’s presence on UK market of natural gas, while utilizing PESTLE analytical framework: a) Political factors, b) Economic factors, c) Social factors, d) Technological factors, e) Legal factors, f) Environmental factors.

- In this part of our study, we conduct phone-based interviews with CEOs of imaginary gas-producing companies in Algeria, Russia and Nigeria.

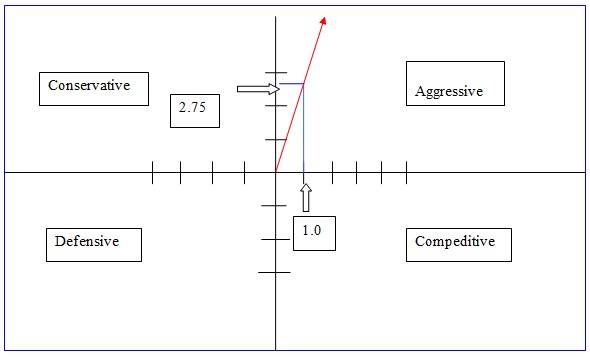

- In the final part of our research project, we will provide readers with our own assessment of implications that derive out of conducted earlier literature review, PESTLE analysis, and three interviews, while being primarily concerned with: a) Summarizing study’s conclusions, b) Defining possible spectrum of practical recommendations for British governmental officials and representatives of this country’s energy sector as to how they can address challenges / opportunities, associated with Gazprom’s operational expansion to Britain. Also, in this part of the study we will construct Strategic Position & Action Evaluation Matrix (SPACE), in regards to the current positioning of Gazprom on UK market of gas.

Data and Methods

Given the fact that the export of Russian gas to UK can be best discussed in terms of being a comparatively recent economic and political phenomenon, it would be wrong, on our part, to rely on utilization of solely quantitative methodology, while proceeding with a research. In our case, referrals to statistical data, regarding the history of Gazprom’s expansion onto UK gas market, can only have a supplemental value, because they could not possibly provide us with understanding of the full scope of intrinsic motivations, behind such an expansion. If we had only relied on the analysis of the rates, by which Russian gas has been finding its way into UK in recent years, then Gazprom’s plans to acquire at least 20% of Britain’s gas market by the year of 2015 would not make much sense in our eyes. Yet, there is nothing truly improbable about these plans.

As it appears from the editorial “Gazprom plans to have 10% of U.K. gas market by 2011”, which is available on the web site of Russia’s official news agency RIA Novosti, Gazprom’s top officials are being already in the process of calculating the amount of income Gazprom will be able to generate in Britain by the year 2011, when according to their beliefs, 10% of natural gas consumed in UK will account for Gazprom’s supply: “Gazprom plans to occupy 10% of the British energy market by 2011, Gazprom CEO Alexei Miller said on Friday at the Russian energy giant’s annual shareholders’ meeting” (RIA Novosti 2009). Thus, without denying the fact that, while pursuing with the research, it is utterly important to observe statistical trends, as to the annual amount of exports of Russian gas into UK, it would be wrong to assume that relying on statistical data alone, as solemn theoretical premise of this study, would endow the conclusions of this dissertation with full conceptual validity.

In its turn, this brings us to discussion of application of what kind of research methodology for this study would the most appropriate. As we have suggested earlier – the analysis of quantitative data alone, in regards to the subject matter, can hardly serve as metaphysical basis for this work’s conclusions to be based upon. Thus, we are being left with only one possible methodological option – to tackle the subject of this research project by mainly the means of qualitative analysis, while resorting to the analysis of statistical data as only the secondary methodological instrument. As Herbert and Riene Rubin had put it in their book “Qualitative interviewing: The Art of Hearing Data”: “Qualitative research methods emphasize the depth of understanding associated with idiographic concerns. They are intended to generate theoretically richer observations that are not easily reduced to numbers” (Rubin & Rubin 1995, p. 25). In other words, it is namely by exploring the conceptual significance of this study’s findings that will be able to reveal the full scope of their practical implications.

Methodology

The considerations of methodological appropriateness, outlined earlier, provide us with the insight on application of what kind of methodological approach we should resort to, while conducting this research. The essential elements of this approach can be defined as follows:

Review of relevant literature

The literature review has been traditionally considered as one of the most effective qualitative research-methods, because while being exposed to different authors’ opinions, as to the subject of a particular research, we do not only obtain relevant information, but also get to assess the implications of a researched matter from variety of different perspectives. The rise of Internet, as informational medium, had significantly increased researches’ chances of discovering the true meaning of a studied social, political or economic phenomenon. In their book “The Real Life Guide to Accounting Research: A Behind-the-scenes View of Using Qualitative Research Methods”, Christopher Humphrey and Bill Lee state: “For qualitative researchers, the web offers an apparently impersonal collection of artefacts, concerning business and interpersonal processes and interactions. Further, the widespread availability and amount of data on the web has led to researchers asking new questions, developing new research ideas and theories, to reach a different and potentially richer understanding of phenomena than was possible in any given time frame even as recently as 10 years ago” (Humphrey & Lee 2004, p. 310). Given the fact that Britain began importing natural gas only five years ago, there had not been many studies conducted on how the shortage of this natural resource will affect this country’s economic and political standing in the future. Moreover, because the amount of Russian natural gas that is being currently supplied to UK can be best referred to as rather insignificant, only very few British politicians had seriously considered the possibility for the UK to become energetically dependent on Russia in the near future. Nevertheless, the information, in regards to how Gazprom might pursue with expansion onto UK market of gas, which is available on the web, leaves no doubt as to the fact that Britain’s energetic dependency on Russia had long ago ceased to represent a purely hypothetical possibility. Therefore, while conducting this research, we will take an advantage of the fact that we have a direct access to online informational resources. Nowadays, the academic dubiousness of many of such resources is being counter-measured by the fact that, so far, these sources remain well beyond the reach of hawks of political correctness.

PESTLE Analysis

The value of any academic research directly corresponds to universality of such research’s conclusions. Therefore, it is the matter of crucial importance for researches to be able to properly identify the objective subtleties of a particular issue that it being analyzed. This is exactly why PESTLE analysis became an indispensible tool in the field of contemporary marketing. In his book “Key Marketing Skills: Strategies, Tools, and Techniques for Marketing Success”, Peter Cheverton refers to PESTLE analysis as probably the only fully reliable tool of economic forecasting: “For much of the time, these factors (political, economic, social, technological, legal, environmental) are simply things that we read about in the newspapers, but from time to time they have a dramatic impact on the working dynamics of our own marketplace. The marketer’s task is to make sure that this ‘time to time’ impact doesn’t come as a surprise, and, even further, to seek to gain advantage by recognizing and understanding the relevance of these changes, ahead of the competition” (Cheverton 2004, p. 72). Thus, it was not by an accident that we decided to tackle the issue of supply and demand of Russian gas on UK market within the framework of PESTLE analysis – by subjecting the subject matter to such an analysis, we will be able to not only properly identify objective preconditions that prompt Gazprom to pursue with the strategy of expansion onto British gas market, but to also predict what would be the practical effects of this expansion. Moreover, after having analyzed the issue through PESTLE’s theoretical framework, we should be able to come up with prediction as to whether Britain’s energetic dependence on Russia can be discussed as an objectively predetermined economic phenomenon or not.

Data

Given the particularities of methodological approach we intend to make use of, while conducting this research, the data that will be obtained throughout study’s entirety can be generally divided on “temporal” and “spatial”. Temporal data will mainly account for statistical information, in regards to the current dynamics on UK market of natural gas, because of such data being closely associated with linear flow of time. In their book “Exploratory Analysis of Spatial and Temporal Data: A Systematic Approach”, Natalia and Gennady Andrienko state: “Temporal specificity” appears only in queries with constraints that specify times (i.e. time moments or intervals) or some temporal relations” (Andrienko & Andrienko 2006, p. 346). Spatial data, on the other hand, will correspond to the results of PESTLE analysis, and can be discussed in terms of a long-term trend, which has three-dimensional characteristics. The same book, from which we have already quoted, authors provide us with the insight on conceptual essence of such a data: “Spatial data are data in which at least one of the components, either a referrer or an attribute, has a spatial nature. The presence of a spatial referrer means that the values of some attributes are associated with spatial locations, spatial segments, or objects situated in space” (Andrienko & Andrienko 2006, p. 341). As we have suggested earlier, the analysis of current statistical data, related to supply and demand of Russian gas in UK, would only endow us with a better understanding of such supply and demand’s current specifics. However, given this work’s strategic nature, we will regard temporal data as one among many indications as to the time-spatial nature of this study’s subject matter.

Literature Review

Just as any method of empirical research, literature review is being conducted to reach a number of clearly defined objectives:

- Collection of relevant data. By analyzing relevant online and printed materials that contain information, directly relating to the subject of this study, we will be able to establish a factual groundwork, upon which this dissertation’s conclusions will be based.

- Outlining data’s conceptual pattern. While collecting relevant data, we will also aim at exploring whether such data’s temporal values correspond to a particular “spatial” trend. By doing it, we will be able to gain a better understanding of a researched subject matter, even before we embark on conducting PESTLE analysis.

- Evaluating authors’ own perspectives, in regards to information, contained in their articles and books. By applying an analytical approach towards assessing authors’ opinions, we will be able to define whether a certain commonality can be found in how they discuss the implications of the data, which was obtained during the course of their own research.

Current situation with supply and demand on UK market of natural gas

Hodgson, P. (2004) Gas supplies to the UK – a review of the future. [Internet]. IOP Institute of Physics. Web.

- In his briefing paper, Peter Hodgson outlines objective preconditions for Britain’s energy system to begin experiencing the shortage of natural by year 2010. These preconditions can be defined as follows:

- Ever-increased demands for natural gas within EU, due to political, industrial and environmentalist reasons.

- Continuous political instability in such gas-producing nations in Eastern hemisphere as Russia, Algeria and Nigeria.

- The fact that gas-transporting system (pipelines), utilized by Russia to export natural gas to EU, cannot be maintained fully functional at all times and also cannot be easily diversified.

Apart from describing geopolitical challenges, associated with keeping Britain’s needs in natural gas satisfied, in his study Hodgson also highlights purely technical ones, such as counter-productive nature of a relationship between the sheer length of gas pipelines and the commercial feasibility of natural gas, which is being streamed through these pipelines: “Transporting the gas requires compressor stations roughly every 100 kilometers along the pipeline… It has been estimated that up to 25% of the natural gas may be lost to the consumer in transporting the gas over thousands of kilometers” (Hodgson 2004, p. 6).

Despite the fact that in his study, Hodgson had rightly predicted the depletion of natural gas in United Kingdom Continental Shelf by the year 2006, he also makes it clear that by the year 2020, two thirds of energy consumed in UK on annual basis will account for natural gas: “It is expected that gas will become an even more dominant source of energy providing two-thirds of the UK’s total energy requirement by 2020” (Hodgson 2004, p. 4). Author bases such his prediction on the following set of considerations:

- Environmental friendliness of gas-fired power generating plants.

- High commercial feasibility of gas-fired power generating plants.

- The continuing process of liberalization on EU. market of natural gas.

Hodgson supports his conclusions with statistical data, which indicates that, ever since early nineties, the rates of gas consumption in UK began to increase in exponential progression to the flow of time – that is; whereas, in 1997 gas-generated power in UK was fulfilling only 12% of this country’s overall power demand, by the year 2004 the ratio of gas consumption in UK had risen to 40%. Author concludes his study by suggesting that, in order for Britain to be able to successfully deal with gas-related challenges in the future, it must seek to diversify its gas-energy sector: “The trend towards natural gas as the major primary fuel, coupled with declining UK fossil fuel resources and a reduction in electricity generating capacity from other domestic sources, brings to the fore the need for diversity and a balanced mix in order to provide security of supply” (Hodgson 2004, p. 7). The implications of Hodgson’s briefing paper directly relate to the subject of our study – in next few years to come, the situation with Russian gas in UK is going to be characterized by an increased demand for this gas, on one hand, and by under-supply of this gas, on the other, due to political and technological reasons.

Wright, P. (2006) Gas Prices in the UK: Markets and Insecurity of Supply. Oxford. Oxford Institute for Energy Studies.

The reading of Philip Wright’s book comes in particularly handy for anyone who strives to attain a comprehensive insight on what will account for the situation with supply and demand of Russian gas in UK, because in this book, author explains structural properties of Britain’s gas-powered energy system. According to Wright, as of 2004, 45% of all natural gas that has been streamed to Britain, served power-generating purposes, even though that in 1995, the amount of such gas accounted for only 15%: “The largest component for the demand of gas (in UK) is demand from households, with demand for power generation a close second. The remaining, approximately one-third of demand is fragmented, with energy industry own use almost on pair with “other final users”, who include commerce and public administration” (Wright 2006, p. 4). As of today, there are five power-generating companies in Britain that operate more then one plant: EdF Energy, E.ON, International Power, RWE Innogy Plc and Scottish Power. All of the power-plants that are being operated by these companies have dual capacity – that is, they can run on gas and also on coal. In other words – if for whatever the reason the supply of gas to these plants gets to be interrupted, they will continue to remain fully operational.

The fact that earlier mentioned companies can well afford having the flow of gas to their power plants being broken up for unspecified period of time, automatically causes them to seek signing “interruptible” contracts with suppliers of natural gas, because of cost-efficiency, associated with such contracts: “Some gas consumers pay less for their gas in return for accepting a possibility that, within certain agreed rules, their supplies may be interrupted… 45 days (per year) is the standard level of allowable interruption in interruptible contracts. However, this is the maximum cumulative interruption over the course of a year: there is no expectation that a single interruption lasting 45 days would actually occur” (Wright 2006, p. 6). In its turn, this provides us with a better understanding as to why the percentage of Russian gas within Britain’s energy system continues to grow – signing direct “interruptible” contracts with Gazprom is the most logical choice for British large power-generating companies which continuously strive to increase their commercial competitiveness, especially given the realities of today’s world-wide economic recession. And, the reason why these British companies are able to sign direct contracts with Gazprom, is because the functioning of Britain’s gas-energy sector continues to remain utterly deregulated, as compared to what it is the case in other countries of EU.

In his book, Wright also explains why currently existing situation within British gas-energy sector poses a considerable danger to Britain’s well-being as energetically secure country: “Even at its theoretical maximum only a relatively small proportion of gas demand could be displaced by the most dynamic and price responsive UK consumers of gas, and in practice the actual proportion displaced has been less then 1 percent” (Wright 2006, p. 7). Therefore, it appears that the reason why Britain has not yet experienced the acute shortage of energy in winter months, when the rates of gas consumption double, has to do with a blind luck more then with anything else. It is needless to say, of course, that such situation can hardly be referred to as tolerable.

Blauvelt, E. (2007) Natural gas – Britain nearing end of self sufficiency. Web.

Euan Blauvelt article’s main points confirm the validity Wright’s argumentation, which we have outlined earlier. These points can be summarized as follows:

- It is the matter of very short time, before Britain will be affected by an energy crisis, due to government’s failure to diversify country’s energy sector: “With Britain reliant on diminishing natural gas supplies and renewable energy sources only expected to shoulder a small percentage of the energy demand, an energy crisis is imminent” (Blauvelt 2007).

- Government’s original intention to utilize “renewable sources of energy”, by the time when conventional sources of such energy in country’s possession become depleted, appears to have been based on wishful thinking. This is exactly the reason why the only remaining option for UK to deal with a situation, is building more nuclear power plants: “The government has now changed its tune and opted for nuclear power” (Blauvelt 2007). However, building such plants is being associated with so many environmental and political challenges that it is very unlikely that this process would ever begin. Apparently, Britain’s major energy-generating companies are being well aware of this fact, which is why they seek for alternative options to assure the interrupted flow of natural gas to UK: “The gas industry is investing heavily in new pipelines to import gas from Norway and the Netherlands in addition to Russian piped gas” (Blauvelt 2007).

- The prices for “final consumers” of natural gas in Britain continue to rise, despite the fact that major suppliers of gas to UK, such as Norway and Russia, are simply in no position of asking more for the gas that is being streamed to UK, since prices for crude oil (the natural resource that cannot be replaced with coal, unlike what it is the case with gas) continue to remain at all time low. Author does not provide us with the answer as to why this is happening, even though that the answer to this question appears to be quite obvious – apparently, gas-powered energy companies in UK enjoy little too much freedom of corporate action.

The only weak part in Blauvelt’s argumentation is that he draws parallels between Russia, as the biggest exporter of natural gas in the world and OPEC, as an organization that represents world’s major oil exporters: “Russia is flexing its muscles ominously and is talking of a gas version of OPEC” (Blauvelt 2007) – if anything, Russia is the least interested in joining “gas version of OPEC”, because then, it would have to begin playing by third party’s rules, while supplying gas to EU. In its turn, it would unable Russia to offer “energy partnership” (low-priced gas) to countries-importers of natural gas, in exchange for political favors, as it does now. Nevertheless, the overall validity of concerns, raised by Blauvelt in his article, cannot be doubted.

Durrant, B. (2005). UK energy: why is Britain so low on gas? Fleet Street Invest. Web.

While researching this work’s subject matter, we could not have possibly skipped mentioning Durrant’s article, even though it was being written four years ago, because in it, author outlines the history of how current situation with supply and demand of gas in UK came into being. As it appears from the article – the solemn reason for the fact that today’s Britain faces absolutely realistic prospect of energy crisis, is because during the course of late eighties, the government had adopted an utterly irresponsible stance towards the process of UK energy sector being privatized. “From the interwar period until about 20 years ago, gas was used to provide only domestic heating. But following the privatisation of the electricity industry in the late 1980s, it became a low-cost alternative to coal for power stations” (Durrant 2005). After having acquired 80% of ownership rights over UK energy infrastructure, British largest power retailers had switched to natural gas, as power-generating medium. However, they had failed to conduct comprehensive feasibility studies on the long-term appropriateness of such their decision, as the result of them being solely concerned with generating as much commercial profit as possible, within a matter of comparatively short period of time. Thus, just as the article analyzed earlier, “UK energy: why is Britain so low on gas?” implies that it is namely a corporate greed, on the part of Britain’s largest power-generating companies, and British politicians’ corruptibility, which should be primarily blamed for the current situation within UK energy sector.

The ultimate conclusion of Durrant’s article is being expressed in the following sentence: “Britain is beginning to look more like a European country – lacking its own domestic gas supplies – but without the storage capacity… If we were to have a one-in-10 cold winter, industrial gas demand would have to be cut by 30% for up to 40 days in order to keep the system in balance and prevent power cuts to domestic users – the ‘sacred cow’ of Britain’s woefully inadequate energy politics” (Durrant 2005). Nowadays, Laborites in high offices are trying to convince public that there were many purely objective reasons for Britain to begin experiencing a shortage of natural gas, such as depletion of gas deposits in UKCS. In the similar way, Hitler used to blame Russian cold winter for German army’s inability to sack Moscow in 1941; however, winter had nothing to do with it – it was due to German army being utterly unprepared for fighting in winter, which caused it to sustain a defeat in 1941. The depletion of gas in UKCS has nothing to do with Britain currently standing on the brink of energy crisis, but the fact that, during the course of last decade, Britain’s most prominent politicians had been solely preoccupied with turning this country into “Northern Pakistan”, instead of addressing issues that really do matter, such as ensuring Britain’s energetic security.

Conclusions

The major conclusions that derive out of earlier conducted literature review can be summarized as follows:

- As of today, UK is the least energetically secure country, as compared to other members of EU.

- The percentage of Russian gas within UK gas-energy sector will continue to increase, (due to Britain’s major power-generating companies’ ability to sign a direct “interruptible” contract with Gazprom), for as long as supply of natural gas in Russia lasts.

- British government’s current attempts to diversify country’s energy sector are very unlikely to produce positive results, due to these attempts’ utterly formalistic essence and due to high rates of deregulation within energy sector of UK economy.

In the next part of this study, we will strive to provide readers with the insight onto economic, political and geostrategic implications of Russia being determined to become one among major suppliers of natural gas to UK, by analyzing relevant information in regards to the subject matter, contained in online and printed sources.

Russia as an exporter of natural gas to E.U. / UK

Noel, P. (2008) Beyond dependence: How to deal with Russian gas. [Internet]. European Council on Foreign Relations

Pierre Noel’s report can be considered as the most comprehensive study of how supply of Russian gas to Europe affects dynamics on EU energy market, up to date. The foremost thesis of this report can be summarized as follows:

- Unlike world’s market of oil, Europe’s market of natural gas is being overly politicized, due to Russia’s intention to utilize its status of a major gas-supplying country as the tool of pursuing its geopolitical agenda: “Europe wants to depoliticize the EU-Russia gas relationship in order to integrate Russian gas imports into a competitive pan-European gas market and to maximize the volumes it can import from Russia. But Russia – or its current leadership, at least – wants precisely the opposite: to keep the politics in the gas relationship” (Noel 2008, p. 2).

- The importance of assuring the uninterrupted supply of Russian gas is being often exaggerated. Unlike what it is being commonly believed, the volume of Russian gas supplied to EU continue to decrease, as time goes by: “Since 1990, 80% of the growth in European gas imports has originated from countries other than Russia, especially Norway, Algeria, Nigeria and middle eastern countries. Accordingly, Russia’s share of EU gas imports has declined sharply, from 75% in 1990 to just over 40% today” (Noel 2008, p. 5).

- There are many indications as to the fact that, during the course of next few years, Gazprom will have an increasingly difficult time, while sticking up to its contractual commitments, for as long as the export of Russian gas into the countries of EU is being concerned: “Despite controlling the world’s largest gas reserves, Gazprom will find it difficult to maintain its current supply levels. Production from the three “super-giant” west-Siberian gas fields, which account for the bulk of Gazprom’s output, is now in steep decline” (Noel 2008, p. 5).

- It is in Russia’s best interests to keep EU market of gas segmented, which is why Gazprom tries its best to prevent EU members from working out a common energy strategy. The way Gazprom approaches this task is very simple – it offers individual EU’s members to supply them with low-priced gas, in exchange for a variety of political favors, on these countries’ part. Also, it seeks to attain a share in European gas-transporting system, which has direct implications to the situation on UK gas market, since Gazprom had already bought out Pennine Natural Gas in 2007 and continues to bombard British largest gas retailer Centrica with takeover offers. This is exactly the reason why; whereas, the overall volume of Russian gas streamed to E.U. continues to decline, the volume of gas that is being redirected to Britain continues to increase.

Gorst, I. (2009) Dreams of Gazprom. Petroleum Economist, 76 (5), p. 18-20

In her article, Isabel Gorst discusses the operational weaknesses of Gazprom, as world’s biggest gas company, while bringing readers’ attention to the fact that Gazprom can no longer be discussed in terms of being a purely commercial institution, after having been turned into the tool of Russia’s geopolitical expansion by Vladimir Putin. According to Gorst, there are no objective reasons for Gazprom to apply pressure upon East European consumers on natural gas, as it was the case during the winter of 2009, when Russia had simply stopped streaming natural gas to Europe through Ukrainian-owned pipelines. The fact that Gazprom continues to act as if it was nothing short of a monopolist on EU gas market, can only have one possible explanation – the prospect of generating commercial profit by supplying gas to nations of EU does not represent this company’s top priority. Therefore, it is conceptually inappropriate to compare Gazprom to Algerian or Norwegian suppliers of natural gas. Unlike what it is the case with its rivals on European market of gas, Gazprom is being primarily interested in acquiring more and more ownership rights over Europe’s gas-transporting system. The sheer aggressiveness with which Gazprom pursues such its agenda can be explained by:

- The particularities of current world-wide economic crisis.

- The fact that Russia’s reserves of natural gas are far from being limitless, as Gazprom’s officials would like us to believe.

In order to substantiate the validity of her article’s main thesis, Gorst points out at the following list of problems that are being presently faced by Gazprom:

- Decreased demand for Russian gas in European countries with diversified energy sectors, such as Germany and France, which explains Gazprom’s recent failure to reach its market capitalization objectives: “As recently as last summer, Gazprom boasted it would, by 2015, be the world’s biggest company in terms of market capitalization with a value of $1 trillion. Since then, its market capitalization has fallen from a peak of near $300bn to around $90bn” (Gorst 2009, p. 19).

- Gazprom is having an increasingly difficult time, while trying to offer its partners competitive prices for gas, due to world-wide sharp decline in prices for crude oil: “Export earnings are set to fall this year, as European gas prices, pegged to world oil prices with a time lag of six to nine months, decline in the second quarter — the price of oil has fallen by 64% in the last nine months” (Gorst 2009, p. 19).

- The fact that gas-deposits in three major Siberian gas-fields, currently exploited by Gazprom, are estimated to only last for another 5-10 years. In its turn, this explains Russia’s recent military activities in Arctic Ocean: “Russian Security Council released a strategy document in March calling for an increased military presence in the Arctic to ensure the transformation of the region into Russia’s “main strategic resource base” (Gorst 2009, p. 19).

Thus, the main conclusion of Gorst’s article can be formulated as follows: even the short-term benefits (low-priced gas), associated with European gas-importers signing “energy partnership” with Gazprom, cannot be thought of as an objective category, due to Gazprom’s utter operational unreliance, with “energy partnership” long-term benefits being simply non-existent.

European economy causing uncertainty for Gazprom. (2009). Pipeline & Gas Journal, 236 (5), p. 57

Despite “European economy causing uncertainty for Gazprom” editorial’s small size, it provides us with a comprehensive clue as to what will account for Gazprom’s operational strategy in near future, which directly relates to the ultimate theme of our research project.

According to this editorial, Gazprom continues to enjoy a competitive advantage over its rivals on European market of gas, due to sheer flexibility of its contractual obligations: “Gazprom has a key role to play in helping Europe manage any emerging gas bubble. Gazprom’s supplies have contract flexibility of up to 30% on the annual contracted quantity, depending on the market, before the minimum take or pay kicks in” (Pipeline & Gas Journal 2009, p. 57). Given the fact that the amount of Gazprom’s annual sales to Europe in 2008 accounted for only 20% of its total sales in the same year, world’s largest exporter of natural gas can well afford sustaining loses, associated with the demand for gas in Europe being significantly curtailed, without even trying to increase the attractiveness of its “energy partnership” offers: “Gazprom is scaling back its European gas export forecast by 30 Bcm to 140 Bcm in 2009 (18% reduction), the second downward revision this year. Gazprom’s export volumes would be at or below the minimum take-or-pay commitments from its gas buyers” (Pipeline & Gas Journal 2009, p. 57). While curtailing its gas exports to Continental Europe, Gazprom increases the amount of gas that is being streamed to Ukraine and UK, with this company’s ownership share in both countries’ gas-transporting systems continuing to swell.

As it appears from editorial’s context, Gazprom’s approach to dealing with current trends on EU gas market points out to the fact that Russia strives to prevent the process of this market’s diversification from getting underway. Moreover, it also appears that Norway is beginning to follow Russia’s footsteps, in this respect – something that EU’s political and economic annalists never thought would happen. In the spring of 2009, Norway has declared that it does not intend to reduce the amount of its gas that is being streamed “down the South” – instead, it is going to re-direct an “unwanted” gas to gas-starved UK; thus aiming to kill two rabbits with one shot: to further ensure the competitive edge of its national gas-industry and to create preconditions for the prices on natural gas in Europe proper to begin rising again: “Norway has indicated a desire to maintain export volumes by reducing supplies to Continental Europe to minimum bill (the amount a customer is obliged to pay irrespective of whether they need the gas) and increasing exports to the United Kingdom” (Pipeline & Gas Journal 2009, p. 57). The reading of “European economy causing uncertainty for Gazprom” editorial has brought us to the following set of conclusions:

- A variety of political and economic tensions continue to define the relationship between EU members, which does not allow us to suggest that European counties are being equally committed to diversifying EU gas market. Russia and Norway are going to exploit such situation to their advantage.

- The talks of “gas-energy diversification” within EU are being primarily concerned with the process of natural gas being stockpiled in underground gas-storage facilities. However, just as France and Germany (countries with substantial stocks on natural gas), Britain (country with ridiculously insufficient stocks of natural gas) is not being truly interested in diversifying its energy sector. And, the reason for this is simple – whereas; France and Germany consider themselves being energetically secure nations, Britain is being energetically insecure to such an extent that it simply cannot afford embarking on qualitative diversification of its energy-sector, especially during the time of world-wide economic recession. In its turn, this leaves Britain with only one possible option as to how address the situation – hoping that Russia will continue supplying gas to UK on ever-increased scale. This is the reason why recent months saw a considerable decline in the amount of anti-Russian rhetoric, carried out by British mainstream Medias.

Parthasarathy, S. (2008) Russia-Ukraine gas dispute: yet another prod for Europe. Pipeline & Gas Journal, 235 (7), pp. 46-48

In his article, Sundhar Parthasarathy analyses the effectiveness of Gazprom’s current operational strategy, while providing readers with the insight on how Russia’s largest commercial organization is going to deal with challenges it is currently facing. According to Parthasarathy, there are no good reasons for European consumers of Russian gas to believe that Gazprom would ever reconsider its objectives, for as long as the process of diversification of EU gas-energy sector is being concerned. And, as the proof to such his suggestion, Parthasarathy points out at “gas war” between Russia and Ukraine, which according to the author, has been lasting ever since Ukraine had become an independent country. Given the fact that 80% of Russian gas is being supplied to Europe via Ukrainian gas-transportation system, Gazprom had continuously attempted to acquire a share in this system’s ownership but to no avail. This is the reason why political tensions between two countries continue to remain at all times high.

Parthasarathy’s article accentuates such state of affairs between Russia and Ukraine as an indication of Gazprom’s operational inflexibility – this company will never consider indulging in negotiations with its partners, as the pathway towards achieving a mutual understanding, for as long as such “understanding” can be achieved by the mean of bullying. As it appears from Parthasarathy’s article, the ways in which Russia tries to bring its European gas-partners into submission, can be summarized as follows:

- Applying a direct political pressure upon Central Asian countries-exporters of natural gas, such as Turkmenistan and Kazakhstan, so that these countries would sell gas to Gazprom at ridiculously low prices: “The strategy includes consolidating supply of gas by signing long-term contracts with Central Asian republics and securing equity stakes in key infrastructure in Central and Eastern Europe. The deals with Central Asian countries are mainly to offset the dwindling gas reserves in Russia. Turkmenistan has pledged its entire gas production to Russia at $100 per 1,000 cubic meters…” (Parthasarathy 2008, p. 47). It is well worth mentioning that Turkmen gas is being currently sold by Gazprom to EU at the price of $385 -$400 per 1,000 cubic meters.

- Trying to intensify inner disputes among EU members, by offering its “preferred customers”, such as France, Germany and Italy to sign bilateral “energy partnership” contracts, in exchange for not supporting other EU members’ propositions as to diversification of Europe’s gas-energy system: “The EU, in an attempt to consciously avoid Russia and Gazprom, has made several overtures to Turkmenistan and Azerbaijan to secure its gas directly through Turkey. Meanwhile in 2007, EU members Bulgaria, France, Hungary, and Italy struck private partnerships with Gazprom” (Parthasarathy 2008, p. 48). Author concludes his article by suggesting that importers of natural in Europe should seek for the alternatives ways of ensuring their energetic security: “The solution for Europe lies in diversifying its suppliers and looking at the Middle East and North Africa as options” (Parthasarathy 2008, p. 48). However, as we have pointed out earlier – this is something that is being easier said then done.

Conclusions

The analysis of Theme 2-related articles had brought us to the brought us to the following set of conclusions:

- It is in Russia’s best interests to keep EU energy sector segmented, which partially explains Gazprom’s recent expansion of its operational activities to UK.

- Gazprom faces the prospect of having its currently operational gas-fields being depleted within matter of next few years.

- Gazprom seeks to acquire ownership rights over its partners’ gas-transporting systems in exchange for continuing to supply them with low-priced gas.

- As recent history shows, Gazprom is capable of shutting down the flow of Russian natural gas through the pipelines to those countries that dare to defy Russia politically or economically.

The conclusions, to which we came while analyzing literature related to Theme 1 and Theme 2, provide us with better understanding of a variety of political, economic, technological and legal factors that that affect the situation with supply / demand of Russian gas on UK market. In the next part of this study, we will explore these factors even to a greater length, while utilizing PESTLE methodological framework.

PESTLE Analysis

Political Factors

The political factors that define currently existing state of affairs, in regards supply and demand of Russian gas in UK, appear to be closely related to:

- Continuing tensions between Russia and UK, which came about as the result of FSB’s (Russian secret service) recent activities in Britain. In his article “Londongrad – a problem of Britain’s making”, John Kampfner says: “Gordon Brown appear to have accepted that a signal must be sent that Britain will not tolerate the FSB (the successor to the KGB) assassinating its enemies on UK soil” (Kampfner 2007, p. 23).

- Deregulation of Britain’s gas-energy sector, which allows British large power-generating companies to act as semi-independent political bodies. In their article “The UK Market for Natural Gas, Oil and Electricity: Are the Prices Decoupled?”, Frank Asche, Petter Osmundsen and Maria Sandsmark confirm the validity of earlier suggestion by stating that: “After deregulation of the UK gas market (1995) and the opening up of the Interconnector (1998) – the UK gas market had neither government price regulation nor a physical Continental gas linkage” (Asche, Osmundsen & Sandsmark 2006, p. 27). And, as a direct consequence of it – the share of Gazprom on UK energy market will continue to grow exponentially to the flow of time.

- EU’s apparent inability to diversify its gas market, from which Britain could have benefited, and also Britain’s continuing reluctance to strongly identify itself with this organization. In his book “The Grand Chessboard: American Primacy and Its Geostrategic Imperatives”, Zbigniew Brzezinski refers to UK as country that exerts very little influence on designing European political and economic policies, as compared to what it used to be the case in the past: “Britain’s ambivalence regarding European unification and its attachment to a waning special relationship with America have made Great Britain increasingly irrelevant insofar as the major choices confronting Europe’s future are concerned” (Brzezinski 1997, p. 43).

Despite the fact that British government treats Russia with caution, UK power-generating companies actively oppose such government’s stance, by signing direct “interruptible” contracts with Gazprom. Given the fact that the process of Globalization continues to gain a momentum, even despite recent world-wide economic recession, it will be only logical on our part to assume that, as time goes by, there would be less and less governmental rules and regulations imposed upon operational functioning of UK gas-energy sector. As one of the most famous proponents of Globalization Kenichi Ohmae had stated in his book “The Next Global Stage”: “The global economy ignores barriers, but if they are not removed, they cause distortion. The traditional centralized nation-state is another cause of friction. It is ill equipped to play a meaningful role on the global stage” (Ohmae 2005, p. 15). As we have mentioned earlier, during the course of recent year, the intensity of anti-Russian sentiment, present in British mainstream Medias, has been considerably reduced, which has only one possible explanation – it is namely the considerations of economic expediency, which now serve as metaphysical foundation, upon which the government of John Brown bases its political decision-making.

Thus, it appears that, at present time, there are no strong political obstacles on the way of Gazprom expanding the range of its operations in UK. Apparently, both: British and Russian governments are equally interested in having Gazprom being allowed to supply natural gas to Britain. However; whereas, Russian government’s stance on the subject matter is being motivated by its intention to regain Russia its former geopolitical power, British Laborite government’s stance on the matter can be explained by its executive powerlessness. While understanding perfectly well that Britain’s growing reliance on Russian gas reflects the process of this country becoming less energetically independent, the government of John Brown simply lacks the means to address the situation in any effective manner.

Economic Factors

The economic factors that will shape the dynamics within the ratio of supply / demand of Russian on UK gas market in immediate future directly correspond to the current state of British economy, which is best described as being stagnant, mainly due to a global economic recession of 2009. These factors can be identified as follows:

- The weakened profitability of the corporate sector of British economy. In their article “Prospects for the UK Economy”, Simon Kirby, Ray Barrell, Tatiana Fic and Ali Orazgani, provide us with the insight onto the sheer magnitude of a financial crisis, which has been affecting the proper functioning of UK economy over the course of 2009: “Concern about the state of the UK economy has increased dramatically. The global financial crisis has been acutely felt in the UK. UK financial sector has lurched from the failure of Bradford and Bingley, a mortgage bank, to the near collapse of the UK banking system” (Kirby, Barrell, Fic and Orazgani 2009, p. 101). In its turn, this will serve as an additional incentive for British power-generating companies to seek signing bilateral contracts with Gazprom, as the most logical way of increasing their commercial efficiency. Moreover, the increased inflation rates within British financial system will also enhance the attractiveness of Gazprom’s takeover offers to such British energy retailers as Centrica.

- The increased importance of LNG (Liquid Natural Gas) exports to UK. As of today, the share of annually consumed LNG within UK energy sector accounts for only 5%; however, this percentage is likely to increase considerably within a matter of next few years, due to the limited capacity of British conventional gas-transporting system (gas-pipelines). In their article “Perspectives of the European Natural Gas Markets Until 2025”, Franziska Holz, Christian von Hirschhausen and Claudia Kemfert predict a significant increase in the rates of LNG exports to UK: “The UK started to develop LNG regasification projects in the early 2000s and has three operating terminals in 2008 (Milford Haven, Isle of Grain, and an Excelerate vessel in Teesside). There are expansion plans for these terminals and construction plans for three or so more regasification ports in the next decade. In total, the UK will have more than 40 bcm per year of LNG import capacity by 2015” (Holz, von Hirschhausen & Kemfert 2005, p. 145). If LNG regasification plans’ objectives will be attained by 2015, it will slow down the pace of Gazprom’s operational expansion into UK gas market. However, given the realities of current economic crisis, the prospects for Britain to begin increasingly rely on exports of LNG in foreseeable future appear quite dim, due to high costs, associated with maintaining LNG transport / storage infrastructure fully functional.

- The inadequacy of UK’s current taxation policies. One of the major reasons why the volume of natural gas deliveries from UKCS has been on a sharp decline ever since 2006 is because in this year Laborite government had imposed additional taxes onto British gas industry. In his article “UK: tax regime “not fit for purpose”, Tim Morison says: “The latest tax rises have damaged the UK’s competitiveness and will shorten the productive life of the UK continental shelf…This move (increased taxation) raised the marginal tax rate on fields developed after 1993 to 50%, while fields developed earlier are also subject to PRT and pay tax at a marginal rate of 75%” (Morison 2007, p. 28). Therefore, the depletion of gas deposits in UKCS cannot be referred to as the solemn reason as to why the extent of Britain’s energetic dependency on other countries had increased dramatically through years 2006-2009. In its turn, just as the factors mentioned earlier, this creates an objective precondition for the demand on Russian gas in UK to increase.

Thus, even though that there appears to be many possibilities for Britain’s energy sector to ensure its uninterrupted functionality, without becoming dependent on supply of Russian gas (such as developing national LNG transport/storage infrastructure and investing into national gas-exploration projects), because of the fact that Laborites have been in charge of running this country ever since 1997, and also because of the realities of today’s global economic recession, we cannot seriously consider these possibilities.

Social Factors

Given the clearly defined political implications that derive of out Russian gas’ presence on UK energy market, the prospects for Gazprom’s continuous expansion into Britain should theoretically be challenged by citizens’ negative attitude towards such an expansion – after all, the presence of strong patriotic sentiment among Britons has traditionally been one of this country’s trademarks. However, as the result of Laborite government’s commitment towards promoting the concept of “multiculturalism”, during the course of last decade, British society has grown increasingly depoliticized, simply because people who “celebrate diversity” on British soil at the expense of British taxpayer money, are simply incapable of thinking outside of mental framework of their tribal solidarity. What it means is that slowly but surely Britain is being deprived of its national identity.

In his article “When South is North”, Peter Jenkins is making perfectly good point when he states: “Over the past half century, Britain has become a racially and religiously complex society in which official policy demands full recognition and respect for each diverse voice. However, in recent years, the policy of multiculturalism in Britain had attained truly pathological subtleties – nowadays, any expression of pride in Englishness is treated as a manifestation of racism” (Jenkins 2009, p. 45). Today Britain’s form of governing is best described as neo-Liberal dictatorship, for which citizens’ willingness to profess this country’s traditional values represent a clear danger, because it makes it harder for the government to proceed with the policy of turning Britain into a “global village”.

The briefing paper “The causes of the decline in electoral activity in Britain”, which is available on the web site of PowerInquiry.Org, substantiates the validity of our suggestion as to the fact that British society is becoming increasingly depoliticized: “In recent years, the way civic duty is understood by British citizens has undergone radical change and that this change has promoted withdrawal from electoral activity…In 2000, only 44% (respondents) agreed with the statement “every citizen should be involved in politics if democracy is to work properly” (PowerInquiry.Org 2004, p. 7). Thus, it appears that in today’s Britain there are no socially defined preconditions for the process of this country growing energetically dependant on Russian gas to be met with much of public criticism.

Moreover, given the fact that in recent decades the demographic fabric of British society has been undergoing a dramatic transformation, as the result of concept of “multiculturalism” having achieved a status of official policy in this country, we can now identify many additional social factors that will make it easier for the Gazprom to achieve its plans of taking over 20% of UK gas-market by the year 2015. One of these major factors is the fact that, as of 2008, 5% of UK populace accounted for representatives of racial minorities (Indian/Pakistani). In Britain’s large cities this percentage often accounts for as much 30%-40%. Given the fact that these people are accustomed to hot climate, their contribution to the fact that, during the course of winter months the domestic consumption of natural gas in UK doubles, appear as being rather substantial. Apparently, British citizens of Pakistani/Indian descend do not profess the values of British “warmth preservation” culture – that is, it never occurs to them that their gas bills can be substantially reduced by application of indirect warmth-preservation methods, such as installing double-glass windows in their houses for the duration of winter.

In its turn, this partially explains why the price for domestically consumed gas in UK continues to rise, even though that price for the gas that is being used for power-generating purposes in this country continues to remain linked to the price of crude oil. However, it would be wrong to suggest that the dynamics on domestic gas market in Britain are being totally unrelated to the dynamics on this country’s industrial / power-generating gas market – the high demand for “domestic” gas in UK subtly implies the high demand for “power-generating” gas in Britain as well. Thus, there are no objective reasons for Gazprom’s top officials to consider that the pace their company’s aggressive expansion onto UK gas market may be slowed due to unfavorable social factors.

Technological Factors

There can be no doubt as to the fact that the current situation with supply/demand of Russian gas in UK is being affected by a variety of technological factors. The most important of these factors can be outlined as follows:

- The underdevelopment of gas-storage infrastructure in UK. In his online article “More UK gas storage needed to ensure integrity of supply”, Mike Major states: “Currently Britain has just 15 days of gas storage against 99 days in France and 122 days in Germany, leaving it far more exposed to disruptions. Being the largest gas producer in the world, Russia holds a mighty power over Europe” (Major 2009). Given the fact that the talks of gas-supply diversification, in which governmental officials have been indulging for the duration of last few years, were only concerned with these officials’ strive to improve their public image and nothing else,. Britain continues to remain the most energetically insecure country in EU. Therefore, UK energy sector simply cannot afford having the supplies of Russian gas being reduced in volume, and to say the least – cut off altogether.

- The plans for Nord Stream pipeline to become fully operational by 2011. In his article “Moscow Playing Hardball On Nord Stream Plans”, Gordon Feller provides us with the insight onto the fact that, if plans with building this pipeline ( which would directly connect Gazprom to EU gas-transporting system) come to realization within a specified timeframe, the talks about “diversification” and “renewals”, on the part of EU bureaucrats, will effectively stop: “The Nord Stream consortium includes Gazprom with 51% of the shares, Germany’s E.ON Ruhrgas and BASF/Wintershall with 20% each, and Nederlandse Gasunie with 9%. The Nord Stream board had announced as recently as mid-October that the first stage of the pipeline would go into operation in 2011 (deferred from 2010), with the second stage expected by 2012, for a combined annual capacity of 55 Bcm of gas” (Feller 2008, p. 70). This will have a direct effect on situation with supply / demand of Russian gas on UK gas market – in other words, the demand for this gas in Britain will increase dramatically due to: 1) Enormous reserves of gas in Yuzhno-Russkoye field (1000 bcm), from where natural gas is planned to be supplied to Europe through Nord Stream pipeline, 2) The projected low cost of such gas for EU consumers. In fact, the substantial increases in export of Russian gas to UK, which now take place on annual basis, reflect British largest power-generating companies’ anticipation of Nord Stream project’s completion.

- The virtual absence of “renewables”, which could have fully replaced natural gas in UK energy sector. As we have stressed out earlier in this study – British largest power-generating plants have dual capacity, which means that they can run on gas and coal. However; these plants cannot fully switch to operating on coal, due to environmental dangers, associated with utilization of coal as power-generating medium, and also due to depletion of coal deposits in Britain.

The editorial “UK: Use coal and save the planet”, which can be found in Petroleum Economist from April 2008, states: “The UK mothballed much of its coal-mining industry in the 1980s when the country engaged on a dash for gas. Its own coal reserves – all anthracite – are small, at 220m tonnes, according to BP’s Statistical Review of World Energy” (Petroleum Economist 2008, p. 30). Given the existence of negative public sentiment against building more nuclear power plants in Britain proper, it leaves UK energy sector with only one possible choice as to how ensure its operational sustainability (apart from increasing amounts of gas imported from Norway and Russia) – utilization of renewable sources of energy. However, there are no such sources in existence, apart from wind and solar light.

The analytical report “Five Myths about Nord Stream Project”, which is available on the web site of Russian Business News, accentuate the sheer naivety of suggestions that exploitation of renewable sources of energy might be the answer to how ensure Europe’s energetic security: “The renewable energy sources are objectively incapable of becoming a real alternative to fossil fuels in the foreseeable future… While the renewable sources cannot provide for the existing needs, the construction of the Nord Stream pipeline becomes the key to strengthening of Europe’s energy and environment security” (Russian Business News 2009). Thus, currently existing technological realities on UK energy market leave no doubt as to the fact that the demand for Russian gas on this market will increase rapidly in very near future.

Legal Factors

One of the legal factors, which continue to affect situation with supply/ demand of Russian gas in UK, has been mentioned earlier in this study – namely, the legislative deregulation of energy sector of Britain’s economy. As of today, there are no effective legal mechanisms, which could have been resorted to by the government, in order to begin exercising control over how British energy retailers form their pricing policies and also over how these retailers negotiate deals with countries-exporters of natural gaz. The most recent government’s attempt to apply a legal pressure upon Britain’s largest power-generating companies, such as Centrica, had sustained an utter fiasco.

In her article “Retailers stand firm despite government pressure”, Katherine Tucker provides us with the insight on this story’s details: “UK energy retailers remained unfazed last week by threats from Prime Minister Gordon Brown to step in if they failed to pass on the recent fall in wholesale prices to end-users. ERA (Energy Retail Association) conceded that fuel prices had come down over the past few weeks, but said as gas – one of the main power-generating fuels in the UK – is bought through long and short-term contracts on the wholesale market, there is always a time lag between a drop in fuel prices and a drop in household bills” (Tucker 2008, p. 49). As we have suggested earlier, British large energy retailers are now in position of acting as semi-independent political bodies, while aiming to defy governmental legislations, concerned with their operational activities. This is exactly the reason why these companies enjoy the liberty of signing long-term “interruptible” contracts with such organizations as Gazprom, while using it as the excuse for their unwillingness to reduce gas-prices for individual and medium-sized corporate consumers of such gas in UK. Thus, the fact that Tony Blair had allowed the privatization of such strategically important subdivision of Britain’s economy as its energy sector, created legally favorable preconditions for the share of Gazprom’s gas in UK energetic infrastructure to continue increasing.

Moreover, such situation also accounts for the fact that it namely Russian Gazprom, with which British power-generating companies now prefer signing contracts, as opposed to Norwegian exporters of such gas, for example. And the reason for this is simple – even though Russia did sign “The Energy Charter Treaty and the Energy Charter Protocol on Energy Efficiency and Related Environmental Aspects”, commonly known as “Energy Chapter of 1994”, it never ratified it, because of Protocol’s clearly defined anti-monopolist objectives: “The fundamental aim of the Energy Charter Treaty is to strengthen the rule of law on energy issues, by creating a level playing field of rules to be observed by all participating governments, thereby mitigating risks associated with energy-related investment and trade” (Energy Chapter. Org 2009). As we have stated earlier, Gazprom strives for nothing less then attaining gas-exporting monopoly in Europe. And, the way it goes about reaching this objective has been outlined earlier – Gazprom proceeds with taking over its smaller rivals, while never ceasing to offer competitive prices for Russian gas to its European net customers. In his article “Europe should tackle Gazprom monopoly”, Boyden Gray says: “One of the problems is that Gazprom is a rather ugly monopoly, and “hell hath no fury like a monopoly challenged.” People will kill to keep their monopolies. This is a core issue in the European-Russian problem. A key reason why Russian gas is being flared is because Russian operators cannot get their gas into Gazprom’s pipeline networks” (Gray 2009). Thus, even if assessed through purely legal framework, it appears that the operational goals of Gazprom and of British large power retailers coincide with utter exactness, which along with mentioned earlier political, economic, social and technological factors, contribute to the process of Gazprom continuously increasing the volume of its gas exports to UK.

Environmental Factors

The major environmental factors that greatly affect current dynamics with supply and demand of Russian gas in UK can be outlined as follows:

Public’s concern as to environmental hazards, associated with the possibility for governmental officials to decide in favor of building more nuclear power-generating plants in Britain, as the way of mitigating energy shortage. As of today, there are eight fully operational nuclear plants in Britain that generate one fifth of annually consumed electrical power, even though as recent as two years ago, their number accounted for ten. However, even the plants that continue to generate electrify, as we speak, cannot be referred to as being fully operational. In their online article “Power cuts feared in UK nuclear plants crisis”, Geoffrey Lean and Jonathan Owen point out at the objective nature of a challenges that UK nuclear industry is currently experiencing: “Two of the 10 (nuclear plants) have been idle for almost a year, with both reactors out of action due to corrosion. Another two have had one of their reactors closed down for months. And yet another two are having to run both their reactors at less than three-quarters of their normal power for safety reasons” (Lean & Owen 2008). Because of growing shortage of power in this country, Britain’s nuclear sector has been pushing its operational limits too far, which significantly undermined nuclear plants’ functional reliability and prompted more and more citizens to express their concerns about the possibility of nuclear meltdown occurring at one of these plants. And, as objective realities indicate, such their concerns are not being altogether deprived of rationale. For example, a substantial radioactive leak had occurred at Thorp nuclear plant in 2005, which caused local authorities to consider evacuating local residents out of the area.

Therefore, it is highly unlikely that Laborite government will give go ahead to the program of building new-generation nuclear plants, despite the fact that even today it continues to consider such a possibility, because it is being overly concerned with maintaining its cheep popularity among the citizens as its foremost priority. As the result, Gazprom will begin enjoying even a stronger competitive advantage on UK market of gas.

Kyoto Protocol having come into effect in 2005. As a country which had ratified Kyoto Protocol, Britain is being obligated to reduce its emissions of CO2 by 5% through the years 2008-2012. What it means is that switching to coal, in case UK energy sector experiences the shortage of natural gas, can no longer be thought of as an option, simply because coal-powered plants are believed to be the main contributors to environmental pollution. What adds to the problem is the fact that much advertised possibility for UK power plants to begin operating on so-called “clean coal” can be referred to as anything but realistic, due to:

- Technological complexity of the process of converting regular coal into the “clean coal”;

- The fact that it will take at least 20 years for this technology to become fully perfected, so that its utilization might represent a practical possibility;

- Depletion of coal deposits in UK.

In his article “Time to bury the ‘clean coal’ myth”, Fred Pearce states: “The British government is deep into clean-coal cuckoo land… John Hutton, until recently business secretary, claimed that a third of British electricity could be generated using CCS (clean coal) by 2030 – clearly pie in the sky. He should fire the adviser who wrote that for him. The mirage of clean coal is designed to coax the world into maintaining its addiction to the most dangerous (and profuse) fossil fuel of all” (Pearce 2008). Given the fact that burning gas to generate electricity remains one of the most environmentally friendly conventional ways to address the issue of global warming, without undermining the overall efficiency of British economy, there can be very little doubt that, despite its current “clean coal” rhetoric, the government will do its utmost to ensure that the exports of natural gas to UK through the pipelines never drop in volume. This means that Gazprom will continue to expand the range of its activities in UK, while experiencing only a formal opposition, on the part of the government, at worst.

Thus, it appears that there are no valid reasons for us to think that the process of Russian gas being streamed to Britain might be challenged by environmental considerations of any sort.

Interviews

Interview Questionnaire

The following questionnaire has been used to conduct a phone-based interview with CEOs of imaginary gas-producing companies in Algeria, Russia and Nigeria:

- Do you think there would ever be increase in demand for natural gas in Britain?

- Do you think Russia, Algeria and Nigeria would ever develop a stable political system that would allow them to effectively manage their gas?

- What are the issues in regards to the maintenance of pipelines and transportation of gas

- Do you think an estimated amount of 25% would be lost to consumer in the transportation of gas over a thousand kilometers?

- By the year 2020, do you think gas would be more dominant in Britain?

- Do you think that in order for Britain to be able to successfully deal with its gas-related challenges it must diversify its gas- energy sector?

- What do you think is the reason behind the growth of Russian gas in Britain today?

- How does the deregulated British gas-energy sector affect those large companies and Britain as an energetically secure nation?

- Do you think it’s a matter of short time before Britain will be affected by an energy crisis?

- Why the prices for final consumers of natural gas in Britain continue to rise?

Interview 1. Ahmed Halid CEO of Algaz.Inc. (Algeria)

- Of course, there will be an increase in consumption of natural gas in Britain – one does not have to be overly smart to realize it. The reason for this is simple – from 1990 to 2001, the consumption of natural gas in UK had increased by 11%, which means that this consumption has been steadily increasing at the rate of approximately 1% per year – that is exponential growth. What it means is that in 70 years from now, Britain will be consuming twice of the amount of gas it does today. What causes the consumption of gas in UK to increase in exponential progression? It is a simple fact that Britain’s population grows in virtually the same progression. Just read an article “Population Growth at 47-year High”, available on the web site of BBC, and you will realize a simple fact that, if current rate of population growth in Britain persists, in 70 years from now, the number of British citizens will amount to 120 million: “The population is now growing by 0.7% a year, more than double the rate in the 1990s and three times the level of the 1980s” (BBC 2009). The more there are people out there, the more their industries require energy to sustain its existence – it is just common sense logic.

- Where there is a gas – there is huge money. And, where there is huge money, there is a much of political instability. It appears that, under Putin’s leadership, Russian government was able to restore law and order in the country, which is exactly why Gazprom has become a monopolist on Russia’s market of gas. Unfortunately, political instability continues to undermine economy’s proper functioning in Algeria and Nigeria, ever since these countries had attained independence. There is steady rise of Islamic fundamentalism in Algeria today – I bet you have heard about European tourists being periodically killed and taken hostages in our country. So far, Algerian government has managed to keep a situation with Islamic radicals under control, but I cannot guarantee that this is going to be the case in the future. We all remember what happened in Iran in 1980, when this country has been turned from West’s ally in the Middle East to its bitter enemy, within a matter of a single night.