Problem Statement

Introduction

Ernst & Young conducted research considering the estimation of the Islamic financial institutions and explored that the rising demand of Sukuk has already reached US$ 300 billion and would jump up to US$ 900 billion by 2017; moreover, although the product is conflicting with Sharia law, due to Islamic getup and backing of Islamic banking system, Sukuk gained tremendous success.1 Afshar pointed out that 85% of Sukuk in the GCC region do not comply with the basic principles of Islamic Law (termed as Sharia) and are associated with incredible legal risks that conflict with the fundamental provisions of Sharia and conventional regulations of the operating countries.2 The financial system has always engaged to discover rational solutions to the ongoing dilemmas while the conventional bonds and Sukuk both involved to mobilising fund for surplus, spending even if conventional bond stands as a debt instrument, and Sukuk stands for religious ethical financing based on equity.3 Although the religious bannered financial institutions feel very proud to differentiate the Sukuk from conventional bonds from the religious context, and engage to exploit the cheapest sentiments of the Muslim communities, virtually there is no financial and operational differences between the two.4

The theoretical debate of Sukuk and conventional bonds has long been flourished, but following the global financial crisis, the practical implication under the concurrent recessionary economy has presented tremendous growth crossing the border barrier of Islamic countries with assets management value of $1 trillion. The Dawn Media reports that Sukuk is rising with 15 to 20% growth rate per year and exploring in a large number of non-Muslim nations; while the UK intends to make London as a global hub for Sukuk, Hong Kong engaged itself to be the gateway of Sukuk in China, and EU countries are working to welcome this financial instrument.5

Hussain mentions that the constitutional and judicial development of Kuwait has been going through a long-term political crisis following its independence, and the contemporary legislative framework has originated from the ancient tribal codes, influenced by the British colonial rule; after independence, it has pressured for democracy and human rights, and so, different UN conventions with the constitution upholds Islamic law.6 As a constitutional monarchy, there is no separation of power and the judiciary and executives are strongly influenced with monarchic tools to strengthen the existing ruling system; moreover, the business and commercial matters are showing growing conflict with the Islamic law of Sharia due to absence of necessary legislative framework. Under the changing dynamics of global debt financing and capital market growth, it is essential to have a comprehensive study on the comparison between Sukuk and conventional bonds from the legal aspect of Sharia law and the conventional regulations of the financial market.

This dissertation has aimed to scrutinise the development of Sukuk in Kuwait by comparing it with conventional bonds; however, this paper will also deliver five major chapters, such as Introduction, that presents the problem statement, literature review, that handles the scholarly works in this topic area, methodology, findings and discussion, along with the conclusion and recommendation for Sukuk in Kuwait.

Background of the Problem

Salah notes that scandal of Dubai World crisis in 2009 has seriously shocked the global capital markets while Dubai World faced acutely pressure to restructuring of US$ 26 billion due to the setback in the settlement of the US$ 4 billion Sukuk that was due by the Nakheel the developer Dubai World. The Nakheel Sukuk was structured in the class of Manfaa-Ijarah where holders of Sukuk were empowered for ‘look back option’ twelve months later than redemption date and could apply subscription rights; although the Dubai World is the 100% owner of Nakheel and Dubai World is 100% owned by the government, but the Nakheel Sukuk was not guaranteed by the government.7 The failure to repayment by Nakheel Sukuk and appropriate response to the restructuring request raised an interrogative sign with the legal framework of Sukuk and its compliance with the Islamic law called Sharia.

The National reports that a foreign firm Hogan Lovells claimed against a Kuwaiti developer company named ‘Abyaar Real Estate Development’ for non-payment on fees of Sukuk claiming US$ 155,711 under the legal contract through banking channel; moreover, Hope notes that it was offering the valued US$ 225,000 for the claimant.8 The officials of the National Bank of Dubai were implicated the above-mentioned transaction and noticed Mr. Rahail Ali, the associate of Hogan Lovells, that the Islamic bond Sukuk was not monotonous, but resolve expenses bring upon to date is a better accounting process that it put into practice and to make Sukuk holder agreed to reduce fees as original contract. Meanwhile claimant concentrated on the formulate a complete renovation of the structure of transaction from Sukuk to private placement as an individual investor, Abyaar disclosed its financial statement for the first quarter of that year that demonstrated that the company was unable to pay both the Sukuk Murabaha and Istisna’, which is Kuwaiti Dinar 792.4million approximately. Abyaar availed the chance to make it for 10 instalments paying by 10 months; in addition, it had hired an effectual financial adviser who would manage and negotiate with the lenders with the aim to bring them in a contract to the point for rescheduling debts in the capital market.

The Reuters reported that the Kuwaiti company Investment Dar in 2009 failed to pay about US$ 100 million to Sukuk, and was bound to adjust the investor’s claims by converting them into the equity to overcome the dispute and arbitration in this regard and the process of restructuring take two years up to 2011.9 In 2012, Dana Gas of Sharjah has failed to redeem five-year Sukuk of US$ 920 million on maturity due to the delay to receive revenue payments from Egyptian and Iraqi market; as a result, the regional debt market hardly blinked and the Sukuk and shares of Dana plunged due to the fears of non-payment among the Sukuk holders. The overseas investment firms decided to take action against Dana Gas in order to liquidate its assets backed the Sukuk, but the company negotiated with the creditors by offering partial pay back and the rest by issuing issue two new Sukuk; it was really the biggest failure to following the Dubai World crisis in 2009. Meanwhile in 2009, Saad Group of Saudi Arabia defaulted US$ 650 million of Sukuk and gone to arbitration, Malaysia’s strong Sukuk of Sukuk Bhd, Nam Fatt Co and Tracoma Holdings have the evidence of failure to pay back for their Sukuk at maturity that would ultimately raise question to the compliance of Sukuk with the conventional law including Sharia. If Dana and its creditors become unsuccessful to attain an ultimate agreement on the restructuring of Sukuk, it would go for dispute resolution through arbitration; in such case, court may verdicts for liquidation of the Sukuk assets of Dana that would be capable to redeem only 47% of its deterred creditors; so, it would be wise to agree for restructuring.

With such background problems and market disputes of the Sukuk in the presiding years had raised question regarding the regulatory, legal framework of Sukuk, lack of its transparency, lack of benchmarking, limited secondary market, and lack of standardisation, and this dissertation has aimed to scrutinise comparison between Sukuk and conventional bonds in context of Kuwait.

Rationale for the Research

Radzi & Muhamed states that although the literature of Islamic finance proclaimed that Sukuk is complying with Sharia law, but so far, most of the Sukuk disputes have been trialled and arbitrated in the British courts under the British legislative framework and there were no disapproval raised by the Sukuk issuers.10 It illustrates that either there is no provision under Sharia law to resolute non-payment of debts, or Sharia law is not enough to protecting the investors by safeguarding their investment. The legal issues for default payments of Sukuk under the legal framework of Sharia illustrate emergence for more clarity because non-payment generates uncertainty in the capital market, and the investors feel very risky to invest in Sukuk due to absence of legal protections and increasing risk. Sukuk has tried to overcome the Sharia prohibition to give and take interest by presenting land and other assets, and the investors are paid for their assets, but the reality is that most of the Gulf nations have already amended land law imposing restriction on foreign ownership of property in Kuwait, which is a conflicting paradigm of theory and practice. Thus, it has been illustrated that there are huge gaps regarding in the conceptual framework of Sukuk and its compliance with the Sharia law, as the Muslims believe that Islam is the complete code of life, but it failed to resolve the Sukuk disputes for which arbitration goes to the court of non-Muslim nation.

The Financial Times reported that the wave of rising Sukuk is increasingly drawing attention of the global investors due to the Euro-zone debt crisis and liquidity in the GCC Sukuk, which is highly driven by oil prices, issuing both in local and foreign currency specially in US dollar and aim to manage debt financing from local and foreign investors. At the same time, the Malaysia Sukuk is much stronger than GCC due to sharp boost in supply side with sufficient regulatory control and primary attention to the local investors in local currency. As a debt instrument, both the Sukuks have aligned to provide the regular yield, which is very similar to the conventional interest; however, investors could understand that the word ‘interest’ has been technically avoided, but it is ironically offering the similar interest in different name.11 So-called Islamic scholars, profit hunter Muslim business communities and the collaborators of debt financing would like to identify Sukuk as a bond that complied with Sharia law, but in practice, it is a clever approach to hide interest payments from the Muslim communities in order to bring the blind supporters in the mainstream financial market.

The US and the European capital is looking for a new home of investment that emanate from the GCC, but positively it would not mean that the new investors of Sukuk are attracted from the religious scruples of Islamic ideology; its just business and the profit making is the only ideology. To the western investors, Islamic financial system is an area of business where Sukuk is a debt instrument for profit making game and the performance, compliance is the method of play, and there is nothing spiritual or immaterial. Due to Euro zone debt crisis, the investors turned their face towards Sukuk and huge money has been pulled back from Europe to the Middle East where the banks or semi-government agencies issue Sukuk; although there are also credit risk, investors feels it safe for the support of oil-rich states.12

There is enough research to compare the Sukuk with conventional bond; most of them are focused on either the theoretical perspectives or practical growth rate and even with the market demand and supply. A major part of the research in this area are biased by different Islamic financial institutions who would like to promote Sukuk as a tool of debt financing under Islamic garment with no basic difference with the conventional bonds, but behavioural emotional blackmailing with the mainstream Islamic thought is arguing it as a Sharia complied instrument. Another class of research in this area has engaged from the academic needs and tried to establish the supremacy of Sukuk over the conventional bonds, which ultimately supported the prior class. There is no research agenda yet comparing the Sukuk and conventional bonds from their legal perspectives as a whole; thus, it is rational to scrutinize legal foundation of the Sukuk and its compliance with the Sharia law and then compare and contrast the conventional research and this research arena from overall perspective.

Research Questions and Objectives

There are huge studies that have already been conducted on the comparison of Sukuk and conventional bond in context of GCC and Malaysia, different features and market trend, their magnitude and contribution in the capital market of issuing country including their secondary market, but no research agenda yet has risen to compare the two debt instruments from their legal perspectives. The rapid growth of the booming multi-billion dollar Sukuk market has drawn the attention of global investors to this sovereign and corporate Islamic bond, although they were primarily introduced to mobilise capital from the investors who hate interest due to religious faith in the host Muslim countries, but gradually expanded to the non-Muslim markets. As the Sharia law has prohibited interest payments, the strict followers and radical Muslims are not willing to invest their capital in exchange for the interest; therefore, Sukuk has designed without interest rate swaps, credit derivatives, and other detachable options, but kept better opportunities for fixed return on maturity.

As a result, necessities of risk management and competitiveness would pressure the Sukuk for further development that will make the bond as a perfect alternative to the conventional bonds complying with Sharia law as without modification the financial markets of the Islamic countries could not develop in right direction, which is deeply concerned with the legal framework for market regulation. Thus, to compare the Sukuk with conventional bonds, it is essential to compare legal framework of both bonds. The objective of this dissertation is to scrutinize the legal structures of the Sukuk and examine the different risks associated with Sharia law that would be theoretically complied by sovereign and corporate Sukuk operation and then compared with the conventional bonds in Kuwait. This paper also scrutinizes the associated risks of the conventional bonds that may facilitate Sukuk to acquire a market segment and offer recommendation for further restructuring to cope in the competition with conventional bonds for better, superior, and successful sustainable market position in Kuwait. With this objective, this dissertation has aimed to rejoinder the following research questions:

- To what extent the theoretical framework of Sukuk complied with the legal structure of Kuwait.

- How the Sukuk and conventional bonds emerged and developed in the financial market of Kuwait?

- What are the major regulatory loopholes of Sukuk in Kuwait?

Literature Review

Theoretical Framework of Sukuk

The purpose of this chapter is to provide theoretical framework related with the definition of Sukuk and conventional bonds, the history of Sukuk, structures of the Sukuk, benefits of Sukuk, major challenges of Sukuk market, background of the legal system in Kuwait, development of commercial law from 1960s to 1990s, the provisions of new law, and so on.

Defining Sukuk and Conventional Bond

Afshar notes that both the financial vehicles Sukuk and conventional bond have aimed to generate fund flow from surplus capital entities to the shortage spending entities through a logical process that attracts the fund owners.13 Both the financial instruments are not visibly identical, but practically there are no basic financial dissimilarities among them, while the Sukuk financing stands on equity method and aligned with real asset, the conventional bonds stands on debt instrument where the fundamental asset is money. Most impartial scholars have duly criticised the concurrent expansion of Sukuk and blamed that none of the Sukuks in the market had complied with the Sharia law and there is no radical difference with the conventional bonds and where the only difference is their literature of definition and the major characteristics and risk-exposures are mostly similar.14

History of Sukuk

The idea of Islamic capital market or Sukuk market was unknown to the individuals 12 years ago though Sukuk was familiar word to the buyers of the GCC countries; however, Malaysia introduced and developed sovereign Sukuk in 2002.15 On the other hand, literature of previous studies stated that history of Sukuk could be traced back from the first Century while Ottoman Empire started Esham in 1775 to save the nation from the trouble connected with financial crisis. However, the policy makers of Malaysia declared that MNMC issued a sovereign Sukuk in 1995, which was popular to the GCC members; at the same time, McNamara and others note that Bahrain entered this market in 2001.16

Furthermore, it became popular to the buyers within very short time because of many dominant aspects, for instance, the definition of this word is financial certificates while Islam not supported interest-bearing bonds; therefore, it was one of the best solution to the buyers since it fulfilled the provisions of the Shariah law as well as other legal provisions. In addition, Zawya reports that market demand for Sukuk increased to the corporate and public bodies because it provided several advantages to the clients; however, the next diagram demonstrates the history of Sukuk:

Oxford Business Group reports that Kuwaiti corporation “Commercial Real Estate Company” took place the first Sharia based fixed-income offering Ijarah in 2005;18 according to the report of Markaz Research, total amount of Islamic Sukuk was more than US$ 229bn at the end of 2012 among them about US$ 99bn issued within 2009 (40% of total GCC bond market). However, the central bank of Kuwait provides data and the following table gives more information about the issuance of Sukuk in the capital market of Kuwait:

Table 1: Issuance of Sukuk. Source: Self generated

Structures of the Sukuk

It is wrong to think that Sukuk always follow a particular structure since different Sukuks have different features and facilities, for instance, product plans, pay off to the financiers, and rating tactic. In addition, Chik argues that the names or categories of Sukuk is determined by the Sharia agreement into which both the issuers and financiers entered into at the first stage to create legal obligation among them; however, the following figure gives more details about the process or activities of Sukuks:

Zerban and Others argue that the Islamic scholars have identified the most common categorization taking into account Sharia law provisions though each agreement would have created dissimilar obligations; nevertheless, the next diagram shows four main categories of Sukuk in the Islamic financial market:20

Generally, there are mainly four categories of Sukuk in the global financial market and it has already mentioned that every category has different features in terms of chronological developments of the Sukuk, maturity level with year of issuance, hierarchy of sophistication and so on. However, the subsequent table describes the four main types of Sukuk structure more elaborately:

Table 2: Four main types of Sukuk structure. Source: Self generated

Farah reports that the International Islamic Financial Market presented the information connected with different model of Sukuk in the global market from the early stage of development to describe the trend of the investors and other parties in the Islamic Capital market; however, the next diagram demonstrates that Sukuk Al-Ijarah is the supreme point considering both the issuance and attractiveness:

In addition, IIFM reports that the Islamic scholars have provided 14 types of Sukuk under four major categories for which this dissertation focuses on these structures of Sukuk in following points:

Sukuk Ijarah

Many renowned authors like Saleem argues that Ijarah is one of the new products of the Islamic financial market; however, the key features of this kind of bonds include it is related to lease properties and assets, which make sure equal values; at the same time, it needs to address that it has gained acceptance to the Sharia scholars.25 Ali notes that the demand for this type of Sukuk is too high and it attracts investors rapidly since investors are treated as the partners in the ownership of the property and they get yearly or monthly profits from the leasehold assets; however, the governments and companies of different countries would like to generate funds for the long-term projects.26 In accordance with the evaluation of Global Research, it is one of the most significant Sukuk in the Kuwaiti and international Islamic capital market because it has already captured more than 43% of the total share of international Sukuk market as an asset based contracts; however, it has included many risk factors, which the issuers need to address. At the same time, there are many reasons to attract the investors, for instance, complicated legal framework to ensure Sharia compliance, internal disagreement for complying the basic rulings of Islamic finance, and many other factors; however, the following chart gives more details about Sukuk Ijarah or leasing arrangements:

Table 3: Sharia rulings and requirements. Source: self generated

Most significantly, this type of Sukuk is popular in Kuwait for different reasons, for instance, five among fifteen corporate Sukuk issuance were structured under the pure Ijara model; therefore, Saleh states that the government has already introduced new legal framework to provide transparent and developed capital market.28

Certificates of ownership of Usufructs of the future assets

It will be futuristic for a particular time-frame for a specific asset, which will not be ready when Sukuk certificates will issue in the Islamic capital market; however, the certificates are documents of equal value introduced with intent to sake of leasing assets; here, the next table describes Sharia rulings and requirements in more detail:

Table 4: Sharia rulings and requirements. Source: self generated

Certificates of ownership of Usufructs of existing assets

The key characteristics of such bond demonstrates that it holds equal values while the proprietor of the existing assets issue Sukuk; nevertheless, Sukuk holders get the chance to lease the assets by taking consent of the owners of such assets; furthermore, the certificates provide the rights on the service or Usufruct of an asset both direct and indirect way. The main purpose of leasing or sub-leasing such property is to obtain rental from the profits of subscription; here, the certificate holders will be the owners of the Usufruct of an asset to get benefits during the lease period; however, the following table shows Sharia rulings and requirements in more detail:

Table 5: Sharia rulings and requirements. Source: Self generated

Contractor’s or Supplier’s Sukuk

Contractors or suppliers of goods or services can issue this type of Sukuk certificates, which can be for existing commodities; moreover, the certificates carry equal values according to the explanation in the security. In addition, certificate holders will be the owner of the services and will obtain the proceeds from selling the same in the markets; however, the following table shows Sharia rulings and requirements in more detail:

Table 6: Sharia rulings and requirements. Source: self generated

Hybrid Sukuk

Ali states that the investors first issued this kind of Sukuk in the financial market of the United Arab Emirates; however, the advantage and disadvantages, and the characteristics of this bond have created by combining of Istisna and Ijara Sukuks; however, the next diagram illustrates the structure of this bond more elaborately:

The key issuers of hybrid Sukuks are the Solidarity Trust Services Limited and Islamic Development Bank (acted as guarantor); on the other hand, this company mainly combined three Sukuks where presence of Ijarah was more than 51% and rest two Sukuks were Murabaha and Istisna.

Salam Sukuk

According to the view of Islamic scholars, the key purpose of this Sukuk is to mobilizing Salam capital by providing equal value; however, the next figure and table illustrate the structure of this bond with Sharia requirements more details:

Table 7: Sharia rulings and requirements. Source: self generated

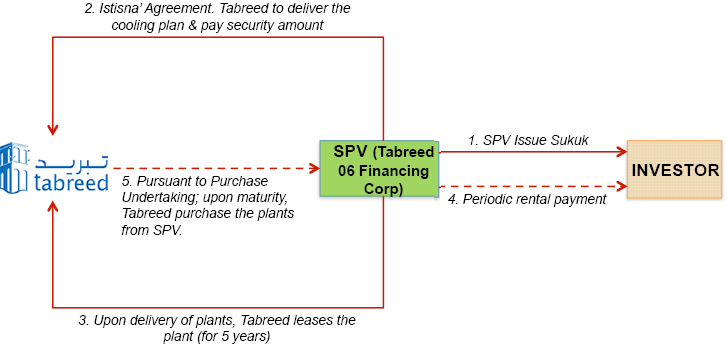

Istisna’a Sukuk

Such items can be sold with partial advance payments consistent with Istisnaa contracts to be delivered at a particular time in the future; however, it is applicable on building along with developing transport infrastructures, such as, vessels, air-crafts, bridges, roads, power generation and water supply stations and so on. Here, it is important to mention that this is the most popular structure to the global investors in this century; however, the next diagram and table provide more details about the structure and Sharia rulings of Istisna’a Sukuks:

Table 8: Sharia rulings and requirements. Source: Self generated

Sukuk al Murabaha Structure

According to the report of Global Research, this type of Sukuk is not playing very important role in the national and international Islamic capital market since it has only captured 5% of the total share of Sukuk market as an asset based contracts; moreover, it has many credit risk considerations linked with mode of finance. At the same time, this organization further addressed that the merchant or his agent can issue this bond to purchase commodity; however, it is a transaction where the seller clearly declare cost plus profit margin; however, the subsequent diagram and table give more details about the structure and Sharia rulings of Murabaha Sukuks:

Table 9: Sharia rulings and requirements. Source: Self generated

Sukuk al Musharaka

In accordance with the estimation of Global Research, this type of certificate played a significant role in the national and international Islamic capital market since it has already captured 27.5% of the total share of Sukuk market as equity based contracts; in addition, it carries equal values and losses; it has many credit risk considerations linked with mode of finance. Simultaneously, this report also pointed out that numerous business entities or the agents could issue this bond to finance projects; however, the subsequent diagram provides more details about the structure and Sharia rulings of Murabaha Sukuks:

The demand for this certificate has increased exponentially since the Sukuk holders can contribute the capital amount to the issuer to enter new market considering different form of strategies; however, the subsequent diagram and table provide more details:

Table 10: Sharia rulings and requirements. Source: Self generated

Mudarabah Sukuk

In accordance with the assessment of Global Research, this type of Sukuk is playing significant function in the Kuwaiti and international Islamic capital market because it has already occupied more than 18.4% of the total share of international Sukuk market as an asset based contracts; however, it is equity based Islamic financial products. At the same time, it carries equal value like other types of Sukuks; however, the characteristics of this type of Sukuk are different from the Musharaka certificates, for instance, it involves a partnership in entrepreneurship and capital; in contrast, both Sukuks are non-debt creating modes of finance while the principal amount of finance is not guaranteed.

Muzaraa Sukuk

The main purpose of issuance of this certificate is to collect funds to meet the agricultural costs where the certificate holders will become the partners of the produced crops according to the provisions of the contract; however, it is not popular in Kuwaiti financial market because agricultural sector is not developed due to lack of water and arable land.42

Musaqat Sukuk

The key objective of issuance of this certificate is to collect funds to irrigating trees that produce fruits where the certificate holders will be entitled to the share of the produced trees according to the provisions of the contract; however, it has no significance in Kuwaiti financial market since agricultural sector has little contribution in the national economy.

Musharakah Sukuk in Investment Agency

The aim of the issuance of this type of certificate is to gather finances to implement different projects where the certificate holders will gain percentage out of the profits according to the provisions of the contract; however, it is not playing vital role in Kuwaiti financial market, as this structure has not followed by the investors.

Mugharasah Sukuk (Planting)

The landowners are issuing this certificate with intent to raise funds to meet the costs of plantation where the certificate holders will jointly share the ownership of the trees according to the provisions of the agreement; however, it has no significance in Kuwaiti financial market since agricultural sector has little contribution in the national economy.

Benefits of Sukuks

- Sukuk is a financial instrument of Islamic Finance Institutions, which assists to manage liquidity in some extent as the investors invest in this sector considering the return on investments;

- Furthermore, it needs to raise funds to meet specific objectives or implement different plans since it contributes to greater stability of the financial systems of the nation;

- Release funds from assets by using the concept of securitization;

- However, the investors can take the opportunity to invest in this sector considering Sharia compliance assets;

- At the same time, it is easy to trade Sukuk in the market, when the investors need cash;

- In addition, investors of some countries like Malaysia get incentive or exemption from the government for which they can save cost related with Stamp duties; as a result, it will decrease the load of the financiers;

- Diversifying the product range considering four main categories of Sukuk is one of the most influential factors;

- Transparency stand for an essential principle underlying all Islamic financial transactions while the profit-sharing characteristic of the transactions imposes an extreme level of disclosure requirement in the financial agreement; however, the accountability of the respective parties assist to increase demand of this type of Sukuk;

Major Challenges of Sukuk Market

This structure was the first marketed at a global level, but it has criticized for several reasons, such as, the issue of guarantee, the Sale and Lease-Back Structure, pricing of Sukuk and so on; in addition, Muslim economists and Sharia scholars had not obtained any alternative option to replace the term interest rate to give profits to the investors. However, the main challenges of the Sukuk market are:

- Financial challenges: According to the report of IMF, the distinctive “buy-and-hold” investment policies along with limited diversity of Sukuk financiers create illiquid secondary markets and slow down efficient price discovery; on the other hand, Islamic financial institutions recommended using LIBOR as a benchmark in order to determine returns from Sukuk Al-Ijarah;

- Furthermore, according to the Islamic Scholars the Sukuk holders are willing to receive returns as a rent of assets (expect to have different rental income from different assets), but sometime they use same interest rate for different assets, which definitely unacceptable from Sharia perspective;

- Doctrine of binding precedent: AL-Maghlouth states that Islamic jurisprudence is neither exact nor bound by precedent; in addition, it also not bound to follow the judgment of the courts of other nations for which it is difficult to develop standard legal framework with Sharia compliance to provide interest to the investors.43

- Sukuk structure: According to the view of the scholars, various Islamic organizations particularly IIFM, IFSB, and AAOIFI have worked for the regulatory consolidation and harmonization; therefore, these institutions have identified mainly 14 Sukuk structures and provided suggestions for more standardized Sukuk structures in 2008 and introduced new rules on the sale;

- Legal challenges: Sukuk needs to satisfy both commercial and Sharia law, which creates inconsistencies regarding asset control along with bankruptcy resolution for the financiers in non-Islamic nations, for example, insolvency measures dependent on Sharia law and it can displace financier protection;

Background of the Legal System in Kuwait

Reunite reports that the legal framework of Kuwait mainly based on Sharia law as Article two of the Constitution 1962 clearly mentioned that Islam is the State religion for which Sharia law would be one of the most significant sources of legislation; however, it considered several provisions of English common law, French and Egyptian law, custom and Islamic jurisprudence.44 On the other hand, Sharia is not the exclusive source for which the government has the opportunity to enact laws bypassing the principles of the Sharia; such as, law of commerce allows interest in the transaction; in addition, it Kuwait has already integrated many international conventions and standards into legal framework of this country. Moreover, the domestic court is not bound to follow the order of the foreign courts if the orders contradict with domestic law; however, Kuwait has a three-tiered judicial system and the next table gives more details about court structure of this country:

Table 11: Court structure of Kuwait. Source: Self generated from;45

Geo-political Background of Kuwait

Sundaram mentions that Kuwait is an oil-rich Arab nation stands on north-west of Persian Gulf surrounded by Iraq and Saudi Arabia with a crude-oil reserve of 102 billion barrels while constitutional monarchy positioned its Emir as the supreme authority of the state and has been striving with a wealthy and open economy to sustain with a political stability.46 Michael notes that due to its geopolitical significance and rich oil resources, the US leaders have deeply concerned to establish influence in this region following the Second World War, during the Iraqi aggression to Kuwait in nineties the US military force engaged to fight against Iraq to make Kuwait free.47 As an integral part of Arabian Peninsula and inherited from Ottoman Empire, Kuwait is in high geopolitical risk although the recent political unrest of Arab-Spring in Middle East has not influenced Kuwait with enough political turmoil rather the country has demonstrated significant economic growth.

Present Status of Sharia Law in Kuwait

The New York Times reported that the Emir of Kuwait SK. Shaba imposed his veto power to prevent a parliamentary proposal to amend the constitution to approving Sharia law as the only source of the countries legislation, which was passed in the parliament in 31: 19 votes out of 50 parliamentarians.48 At the same time, Gabe argues that a constitutional monarchy of the Middle East State of Kuwait has prevented the country from Islamic radicalism by his highness the emir rejected the proposal for constitutional change although the Islamist lawmakers are continuously trying to convincing to turn a most progressive Muslim society towards Islamic extremism.49 While the political environment deeply concerned with democracy, human rights, and women’s empowerment; however, in the name of stable political system, the Islamist lawmakers are trying to take the society to an ancient society of thousands year back.

The Islamist lawmakers argued that the people of the country are very religious and very fond of Sharia law, but those have failed to address how far people demand for democracy and human rights. To establish Sharia law as the key source of legislation the Islamist MPs also interested to amending the Article 79, which ultimately reduce the power of the Emir; consequently, the ruling class of Kuwait would not be interested to go to the way that may abolish the monarchism. The Islamic radicals have already taken absolute control over the fourth parliamentary session and trying to move the state in the way of Afghanistan and Pakistan where the Sharia law is threatening to destroy the human civilization and conduct dangerous ruling to convict other religious followers and minorities. Kuwait is the best regional ally of the US, 85% of the people are local Muslim, and the rests of them are foreigners, Hindus, and Christians where the Muslim monarchies are afraid with the increasing wave of democracy, and human rights that the Arab-Spring spread out rather than Islamist radicals. The Kuwaiti monarchies introduced the ongoing liberalisation process due to the prescription of their western allies, but the increasing spirit of Arab-Spring, the rising threat of Islamic radicalism and regional tensions and rivalries, Iran’s effort to establish its domination over the Persian Gulf may drive them towards a strong diplomatic and military alliance with the US and NATO.

Misconception of Sharia Law Regarding Riba

Abdullah notes that concurrent wave of Islamic Banking and financial institutes propagate that they are conducting banking business complying with Sharia law, but in practice, it is a very obsessive term that delivers fraudulent approach to the Muslim communities in the name of religion. The Submission.org mentions that the Arabic literature has clearly differentiated the terms, Riba, Usury, and Faedah;50 so, Burhan argues that there is no chance of misconception, the holy Quran has prohibited Riba or Usury, which indicates excessive interest or complex interest, but not forbidden Faedah that indicates simple interest.51 It is not clear which Sharia Law the Islamic banking and financial institutions are following, do they comply with Shia, Sunni, or Wahabi Sharia Law, there is no superior touchstone in Islam without Holy Quran, and it has not forbidden simple interest.52 The holy Quran has guided the Muslims to provide charity loans ‘Karz-e-Hassna’ in order to help others business, but there is not a single Islamic banking and financial institution that has complied with this Quranic Verses, rather they are cleverly dealing with excessive interest in the hidden name of ‘profit sharing’ which is nothing but Riba or Usury.53 Thus, the so-called Islamic banking and financial institutions are misinterpreting that they are complying with the Sharia Law as they are violating holy Quran

The Sufi Foundation reports that in the ‘Holy Quran: Surah Al Baqarah’ Verses 2:245, Allah has guided to provide a large loan amount named Qarz-E-Hasna that is totally interest free and almost a charity contribution and the Almighty Allah himself would provide multiple returns to the provider of such loans.54 There is no evidence from the Islamic banking and financial institutions to put into practice of ‘Qarz-E-Hasna’, rather in the hidden name of profit, they are dealing with Riba or Usury and even they are charging different additional charges to the clients far above the general banking sector. They are trying to justify their unethical conduct by passing the lesson of the holy Quran by engaging different perverted Islamic thinkers, who certify that the ongoing practice of Islamic Banking is in the right track. The Muslims as believers of Allah continuously driving to the Islamic Banking without considering the conceptual gap and this is the core competence of the Islamic Banking to grow faster. Barkat conducted a landmark research with the performance of Islamic Bank of Bangladesh and find that the religious bannered bans are charging higher interest than the general banking, not only that, the banks are deeply connected with terrorist funding and evidenced to finance bomb attack in the country and patronising suicide squads.55

Legal structure of Sukuk

Development of Commercial law from 1960s to 1990s

Farhan argues that at the early stage of the history Kuwaiti stock market, there was no significant rules and regulation to control the existing shareholding companies, publish annual reports or check the issuance of commercial bonds, and so on. In the 1950s, the shareholding companies particularly oil based companies had provided healthy financial reports with their own interest due to lack of regulation and they had no legal obligations or barriers in this context; however, the National Bank of Kuwait was the first listed company in Kuwaiti stock exchange.56 That period, oil revenues elevated quickly for which the government had taken many initiatives to concentrate on the infrastructural advancement; in addition, they also focused on the development of national economy by enhancing different projects and flourishing new planning to increase national GDP and purchasing power of the people, and so on.

However, from the very beginning of 1960s, the government had realized the importance of new legal framework to regulate the stock market and introduced Company Act No: 15 in order to support investors for their momentous role on the national economy and eagerness of the financiers to start additional listed corporations. In addition, the aim of that law was to diversify economy by supporting new companies and to increase domestic investment for implementing different projects; therefore, thirteen new firms incorporated in the stock market with KD 35.80m capital at that period. At the same time, the legislators had passed Company Act No: 2, which was amended in 1982 with intent to include new provisions to check and balance capital market through executing financial reporting system; companies faced severe risk factors since this nation had no legal structure for controlling capital market with professionalism. In the last 1960s, the investors were unwilling to incorporate in the stock exchange though there were many effective legal provisions to develop accountability and transparency, for instance, it had 23 listed companies that time; therefore, the government decided to support the new entrant by investing 60% to 98% of overall authorized capital, which influenced individuals to form eight corporations.

In this dissertation, it is important to mention that the stock exchange of Kuwait had focused on diversification from 1977 and it introduced different like financial instruments (Souk Al-Manakh usually brought on credit) to recover the economy from economic downturns, but the share market crashed and small investors experienced huge losses.

Law reform and Companies Decree Law No- 25/2012

The governments of different non-Islamic countries have introduced new laws or changed the provisions of different laws in order to assist the issuance of Sukuk, for instance, the FA57 in the UK removed certain barriers and the Turkish National Assembly enacted FB58 to include tax neutrality measures for Sukuk; moreover, South Korea, Hong Kong and Kenya had taken different initiatives.

However, the government of Kuwait has introduced Companies Decree Law No. 25/2012 and amended this law59 in order to construct the way commercial entities to operate in this country and to persuade investment by providing relieve to investors and institutes; however, this law introduces some significant issues, for instance, when the companies will not be allowed to issue Sukuk.60 At the same time, Al Oula Law Firm notes that this new law mentions that non-profit organizations are not permitted to issue Sukuk;61 however, incorporated companies can issue Sukuk complying particular objectives under this act;62 furthermore, the general partnership company will not acquire financing by starting Sukuk; 63 although Sukuk is the useful methods of capital increase and payment.64 In addition, the companies will be treated under this law if they increase capital through Sukuk;65 however, DLA PIPPER reports that chapter six of this act specially deals with bonds and Sukuk in order to remove existing barriers to issue or increase capital through Sukuk;66 for example, the company may introduce negotiable Sukuk by fulfilling the requirements of Islamic Sharia.67 However, the joint stock companies need approval from the authority and the Central Bank of Kuwait for the issuance of Sukuk; in addition, the obligations of the New Law are more comprehensive for which the issued capital of the firm has to be fully paid and the proposal to issue Sukuk have to passed in the ordinary general meeting.68 However, this law provides many rights to the Sukuk holders such as, the companies will grant a return considering a share in the annual profits of the organizations, but they must have to obeying the obligations of Sharia;69 on the other hand, it provides pre-emption rights to the Sukuk holders in accordance with the obligation of this act.70

At the same time, each kind of Sukuk has to be issued according to the rules of Sharia and the set of special regulations of Sharia supervisory board; moreover, it has jurisdiction to take legal steps against the parties for the disobeying the rules and requirements of Sharia law. However, this regulation also includes rights of the Sukuk holders;71 it includes rights of the members in the listed companies;72 for instance, they are entitled to receive profits and bonus share, participate in the meeting, take action for the non-compliance of the instruction, and exercise the right of conversion and so on.

Comparison of Sukuk and Conventional Bond

However, there are few distinctions between Sukuk and Conventional Bonds from the theoretical viewpoint, but from the practical evidence, it can be said that they have major similarities in case of return of investment those are discussed as follows:

Distinction from the viewpoint of Ownership

Taqi notes that the first approach of Sukuk holders represent ‘ownership of enterprise assets’ on the contrary to the interest-based conventional bonds those provide fixed income on investment, which is higher than the general bank rate.73 Hassan notes that the religion covered Sukuk correspond to the rights on the assets of the issuing enterprise that generate lucrative profits or higher returns similar to the leased assets of the commercial or industrial companies where the investment vehicles associated with several projects, but for conventional bond, there is no ownership rights and indicates to the interest-bearing debt.74 This is one of the major attribute of Sukuk that differentiate it from the conventional bonds, but the most recent market features evidenced that there are huge Sukuks those issued with uncleanness regarding the interpretation of ownership in the company. For instance, the assets offered with Sukuk are the shares of the company both in physical and financial form, but the Sukuk holders are not treated as shareholders merely enjoy right to returns; as a result, it indicates that Sukuk is just buying the returns generated from shares, which is not legitimate way of earning from the Shariah viewpoint. At the same time, there are some proliferation that the organisation of Sukuk stands on the combination of contracts delivered from the Ijarah, Istisna’ and Murabahah carried out by the Islamic financial institutions and sold to the Sukuk-holders who were interested in get returns operation of the issuer company. Thus, it is emergence to review if the sale of debt and inclusion of fixed percentage of Murabahah contracts engaged with Sukuk then how it complies with the Islamic ideology of interest free economy.75

Distinction from the viewpoint of Regular Profit Distributions

On contrary to the conventional bonds, the second argument of the Sukuk issuers that distinguish it is that Sukuk distributes profit to its holders at a fixed percentage on the consideration of the interest rates (LIBOR) and to do so the contracts of Sukuk has integrated some special clause. In order to legalise practice, the special clause of Sukuk contracts incorporated that while the actual profits of the Sukuk issuer exceeds the percentage of interest rates, the excess amount would be paid to the entirety to the Mudarib, or its partner, or to the investment agent mentioning it as an incentive in favour of the manager to boost effectively. Some Sukuk structure prevailed in the market that does not express any rights of the managers to the ‘excess amount’ as an incentive for them, but articulated that none other than the Sukuk holders are empowered to claim a fixed percentage stands on the rate of interest during regular distributions. At the time when the issuer company generates actual profits less than the predetermined rate of interest; the managers are liable to pay out the difference between the actual profit and the predetermined rate of interest payable to the holders of Sukuk considering it as a payback of an interest free loan. As a result, the managers would recover the loan amount both from the excess amount of profit greater than the interest rate and by reducing the cost of repurchasing assets during redeeming the Sukuk or anyone of the two options.

Distinction from the Guarantee Clauses

Al-Bashir and Al-Amine notes that virtually all the Sukuks issue guarantee to return of principal amount at maturity by both the sovereign and corporate issuers and the Sukuk proceeds set up a Special Purpose Vehicle (SPV) in order to endow with an assurance that the issuer would take the responsibility for any shortfall.76 The earliest combined declaration to providing guarantee for Sukuk issuance was introduced by the article 30 (5/4) of the Islamic Fiqh Academy, which was applicable to the Muqaradah Sukuk; however, Ariff & Safari argues that the Sharia law does not impose any obstacle to writing the issuers promise in the prospectus for the Sukuk holder or to the third party.77 For a particular project covered by Sukuk could provide guarantee to the Sukuk holder, fund managers, or any independent personally under the customary term of financial liability where the promise would be a compulsion free from the Mudarabah contract where the Sukuk holder or the fund managers are entitled to claim for any shortfall. On the other hand, the Shariah Standards No.17 of the AAOIFI indicates that it would not be fair to incorporate any guarantee in the prospectus that could negatively affect the Sukuk issuer by taking liability to compensate; rather it would be inspiring to compensate very nominal value of the Sukuk or its face value.

Usmani criticises the concurrent Sukuk and blamed it for violation of the Sharia standards that the guarantee issued by Sukuk issuer or manager to pay back the principal amount at maturity or to repurchase the assets correspond to the Sukuk at stated price is closely the similar to the conventional bonds.78 On the contrary, to the Sukuk, the conventional bound has identified as a long-term debt instrument issued by the government on corporate issuers that generates two cash flows for the investors such as coupons, which are a certain amount of money calculated at a predetermined rate of interest payable at annually or quarterly and the face value payable at maturity. With such complex techniques, Sukuk has taken the similar features of the conventional bonds that provide a predetermined percentage of interest on the principal and provide assurance to return the investment at the time of maturity, which is truly questionable whether it is complying Sharia provisions or not. Both the mentioned cash flows are not dependent on the amount of profit and loss occurred to the bond issuer and has no correlation with earnings that generated from the utilisation of the fund, which raised by traditional bounds exist in the ongoing market.

Distinction from the Risk Exposures

Tariq notes that the Sukuk encounters with different risks according to its structure to compare the Sukuk with the conventional bond it is essential to investigate with the risk exposures of both while some unique risks that the Sukuk carries, but conventional bonds are not and some risks are common for both types of bonds.79 For instance, both the conventional bond and Sukuk have business risk to default on interest and even face value or both, but the corrective technique of them are moderately different from each other. Cakir & Raei argues that in case of default of conventional bonds the bondholder has no other alternative to recover anything without lawsuit and it is unknown how much amount could be recovered and how long-time it takes to recover, but Sukuk holders are don’t deal with bankrupted entry, they have rights on asset that provide better recovery chance.80

The call-risk is most prominent risk for the conventional bondholders while they are obligated to sell the bonds to the issuers, if the interest rate in the financial market grows up, the bondholders would be deprived to enjoying higher interest rate; however, as the Sukuk stand on interest free approach, there is no impact of call risk on Sukuk. On the other hand, the corporate and municipal bonds suffer from liquidity risk due to inefficient secondary market while other bonds carry risk to get reasonable price at a tolerable time, non-tradable Sukuk bears same risks although AAIOFI engaged to introduce tradable Sukuk to overcome such dilemmas. Sukuk always suffers from ethical risk whether it is complying with the Sharia Law or not, value of asset at the beginning and rising value of assets at the maturity another risk for Sukuk while the conventional bond has no such risk. Meanwhile, the risk of high inflation rate concerted with purchasing power and risk of changing foreign exchange rate for both Sukuk and conventional bonds are the same to each other.

Research Methodology

Introduction

Legal research means a systematic investigation or fact-finding towards increasing the sum of knowledge of law and the purpose of such research is to the advancement of legal science; at the same time, it is the procedure of recognizing and retrieving information essential to support legal decision-making. However, the rationale of this chapter is to suggest a methodological structure to analyse Sukuk in Kuwait and provide the comparison between Sukuk and conventional bonds.

Primary data

Vibhute & Aynalem states that primary sources contain original information and observations, firsthand and in-depth information, which can be gathered from the respondents or from the published documents, for example, the Constitution, National Gazette (legislation or proclamations by parliament), periodicals, journals (indispensable sources of information), reports (governmental or non-governmental agencies), and conference papers, doctoral dissertations, and many others.81 In addition, rules and regulations, statutes, directives, and judgement of the cases (either higher or lower courts) are useful primary data sources for the legal research; these sources include in-depth original information regarding the identified research problem; therefore, this paper will consider Constitution of Kuwait, report of stock exchange, Oxford Business Group, and Companies Decree Law No. 25/2012.

Secondary data

Secondary resources support the information derived from primary sources; however, it needs to collect in a systematic or planned way; moreover, most important source, such as, books, legal treatises, and commentaries on statutes, legal dictionaries, and bibliographies, reviews and so on. These authentic and inexpensive sources are usually available in published and electronic format; however, books and treatises provide accurate conception about the subject matters to deal with basic principles and judicial issues. In this context, this dissertation will use several books to conduct research on Sukuk and other conventional bonds in Kuwait, such as, Islamic finance law and practice, Islamic Commercial Law, Law and practice of Islamic banking and finance, Legal Research Methods and so on. At the same time, it will use different internet sources, such as, report of Ernst & Young, Reuters, Ajman chamber, international monetary fund, and financial statement of Kuwait Financial Centre and so on.

Descriptive and analytical research

According to the renowned researcher like Khushal Vibhute and Filipos Aynalem analysed about the different types of research, such as, descriptive, analytical, quantitative, qualitative, empirical research, applied and fundamental research; however, the aim of the first approach is to describe the phenomenon or situation under study and to suggest and analyse the state of affairs as it exists at present. Moreover, this approach represents only what has happened or what is happening without going into the causes of the phenomenon; however, it considers all kinds of techniques of survey though it cannot be used for forming causal relationship among variables.

On the other hand, analytical research approach gives the opportunity to the authors to use facts or information from secondary sources to analyse the situation or make a critical evaluation of the material; in this context, this dissertation will use analytical approach to evaluate the position of Sukuk in Kuwait and provide the comparison between Sukuk and conventional bonds.

Data Analysis

As the researcher will not collect primary data through interview, it will not be necessary to use statistical tools to interpret data related with Sukuk in Kuwait and comparison between Sukuk and conventional bonds; however, it has already mentioned that this dissertation will mainly be based on the secondary data sources and primary data sources (constitution, national gazette, and statutes). In this dissertation, the researcher will compare and contrast both the primary and secondary sources about the position of Sukuk in Kuwait in order to assess the impact of Sukuk comparing with the conventional bonds; all charts will be taken from secondary data sources to analyse the situation and find legal facts.

Ethics Statement

The researcher of this dissertation has ethical obligations for which all the sources will be referenced properly using OSCOLA style particularly the name of authors of legal journals and books will be used in both bibliography and in-text to make this dissertation more reliable to the general people.

Scope and Limitations of the Study

The first and foremost objectives of this dissertation is to scrutinise the legal framework of Sukuk in comparison with the conventional bonds in order to identify right direction for the Kuwaiti capital market and to recommend a most adventurous and unified regulatory policy that would ultimately open a new horizon of debt financing for the governmental and corporate issuers. As a legal practitioner, the author of this research is accountable to represent the interest of the issuers, investors, and fund managers and controlling power of the regulators for both the Sukuk and the conventional bonds that would maximise return on investment in the capital market of Kuwait.

The excellence of this research has extremely dependable on the accessibility and scope of the qualitative research that has allowed to utilising both the primary secondary data, and remarkably varied in different stage of collecting data from the reliable and valid primary and secondary sources without interview. The researcher of this dissertation has enough scopes to observe primary data from the legislative framework of Kuwait, its business law, statutory instruments, financial market regulations along with court rules, orders, official gazette, and judicial review published with Sukuk in Kuwait. Moreover, the researcher has enhanced opportunities to use the secondary sources like and stock market data, textbooks, treatises, thesis, journal articles, dictionaries, and encyclopaedias, commentaries on statutes while ha has facilities to utilise tertiary sources like subject guides and Union lists of the state of Kuwait.

At the same time, this research has faced different limitations while unavailability of research grant for this study is a major obstacle that the researcher faced. Moreover, the allocated time limit for such an enormous study area is so short, which is another notable limitation for this study while shortage of previous research with Sukuk in Kuwait, confusing nature of primary data, scarcity of applicable secondary data that may easily fit with the research objectives, thus the researcher possibly will puzzle to gather more refined data.

Literature Search of the Previous Research:

Table 12: Literature search of the previous research. Source: Self generated

Findings and Discusion

Analyzing the Status of Sukuk in Kuwait

According to the report of the Central Bank of Kuwait, the first Islamic bank KFH started its operation 1977, which operates in accordance with the provisions of Sharia law; however, Islamic finance institutions comprise investment banks and companies (total 93 companies); at present, it has total 106 investment funds among them 54 are Sharia based.82 At the same time, the Central Bank of Kuwait reported that a huge number of investors and related parties are willing to invest for the quality Sukuk particularly government Sukuk, such as, Islamic bank and institutions considering the profit margin in this regard; generally, investors invest in this sector and kept until maturity date.

In accordance with the estimation of Global Research, Kuwaiti Sukuk market occupied only 3% of the total share of international Sukuk market while Malaysia captured more than 32% and the UAE hold about 32% share from 2001 to 2007; however, the next figure shows the presence of Sukuk market in more details:

Issuance of Sukuk in Kuwait with other GCC countries

From the report of different organizations like Global research, IMF, and Zawya, it can be said that capital market had observed success collectively, which forced the new issuers to enter and contribute in the stock market though total quantity of issued Sukuk reduced $8869m by the last 4-year (Kuwait Financial Centre, 2012). However, the next table provides more information about Corporate and Sovereign Sukuk to compare the position:

Table 13: Sukuk Issued in the GCC countries (2007-2011). Source: Self generated

It can presume from the above-mentioned information that corporate issuers had demonstrated low interest in 2008 and 2010 because of several external factors and adverse financial circumstance in the GCC member states; in contrast, the number of total sovereign Sukuk had also reduced from 2009 though there was no change in this sector in 2011.

Table 14: Sukuk Issued in the GCC countries in 2006-2007. Source: Self generated

Here, it is important to note that, Oman and Kuwait were in the lowest position accordingly in the capital market of GCC countries by holding 2% of the total Sukuks; on the other hand, the United Arab Emirates captured more than 66% of total Sukuk; here, the next diagram shows about the position of Sukuk market of the GCC countries:

Kuwait Financial Centre notes that the economy of all the GCC countries mainly based on the oil industry due to having enough reserve of crude oil, Petroleum and so on; therefore, the economy of these countries is not enough diversified, which has great impact on the capital market of these nations.85 Y-Sing notes that in the Sukuk industry, the year before 2013 posed major disputes to the newcomers in the modern Muslim countries like Egypt or Oman in comparison to Kuwait; nevertheless, the industry still observed enormous achievements that year since the major players had smartly refurbished their businesses from recessionary impact, and executed strategic goals and amended courses of action.86

Sukuk Default Case Study of International Investment Group Kuwait

Here, it is important to note that IIG was not fulfil legal obligations to the certificate holders and this company was not in a position to clear periodic payment for US$200m matured Sukuks though it sent the non-payment notice along with mention operational system; therefore, regulators had initiated to introduce transparent and accountable regulatory system for Kuwaiti Sukuk market. In case of Hussayn Ali AlKharafi Vs IIG,87 the CA ordered IIG to compensate KD3.20m along with legal interest at 7% from the first quarter of 2009; however, the representative of this company stated that it had estimated about US$9.90m losses for this ruling of the court; in addition, it resulted more than US$28.40m at that fiscal year.88 Suqalmal reports that in this case, the company had interested to settle the case out of court and tried to negotiate with the parties by giving extra facilities or benefits to save the companies from liabilities, but this attempt was unsuccessful since the Sukuk issuer had not obeyed the fundamental provisions of Sharia law in some extent. However, the decision of this case and uncertain result from the negotiations raised some basic questions in this issue, such as, how a company can fulfil the condition of both commercial and Sharia law in single contract or what is the right process to determine which part of the interest is halal and which part is not. Therefore, it is difficult for the courts to differentiate Halal interest with other form of benefits; in this case, IIG had not trade a portfolio of stocks in accordance with the instructions of the respondents for IIG could not exclude liability. On the other hand, the plaintiff of this case argued that the respondent had given simply a proxy or authorization to sell, which should not treat an instruction of the Sukuk certificate; therefore, Hussayn Ali could not claim that the company had not followed instruction precisely.

Shariah Finance Watch reports that Sukuk issuers in Kuwait had lost their confidence to refinance the debt they borrowed on short-term basis and they seem that capital market failed to recover from global economic downturns, for instance, NIG asked for 4-year extension on repayment of Sukuk as it is in danger to be the line of defaults in market.89 In addition, French argues that it has asked creditors for this extension on a US$475 million Sukuk (maturing next month); however, it borrowed cheap short-term cash, but faced debt problems for which it needs extension to repay 30% of the US$475 million Sukuks.90

Sukuk Default Case Study of the Investment Dar Company (TID)

Wijnbergen and Zaheer mentioned that the default of the Investment Dar (TID) in 2009 was the first incident of Sukuk failure that generated many question regarding the validity and efficiency of the Sharia compliance bond in the GCC region.91 The fact is that the TID, a Kuwaiti holding company has failed to pay intermittent of the Sukuk for an amount of US$ 100 million and urged to restructuring for its incapability to pay back debt of about US$ 3.5 billion and further US$250 million for its another two categories of Sukuk. The first defaulted US$ 100 million Sukuk was in the category of Sukuk Al-Musharaka that had issued in 2005 and registered in the stock exchange of Bahrain and London in next year; additionally, TID issued further Sukuk of US$150 million in the same category and both the issuers were defaulted in the same year.

Details of the Originator

The Investment Dar started its journey in 1994 with the aim to address the gap of Islamic finance in Kuwaiti market and established itself as the pioneer of Islamic finance in the GCC region with the active participation of the giant business leaders of Kuwait and within short time; it turned into the largest investment company in the Arab world.92 At the beginning, the company started with a paid up capital of US$ 83.3 million, registered with the central bank, as am investment holding company, and introduced Sharia compliance banking system in Kuwait and shares of the banks are listed in the Kuwaiti stock exchange. TDI extended its services to the consumer banking, funds management, property development; it generated KD80.5 million of profit with a total asset of KD669.6 million, and acquired many good businesses while acquiring the British Carmaker Aston Martin is remarkable one in 2007.93

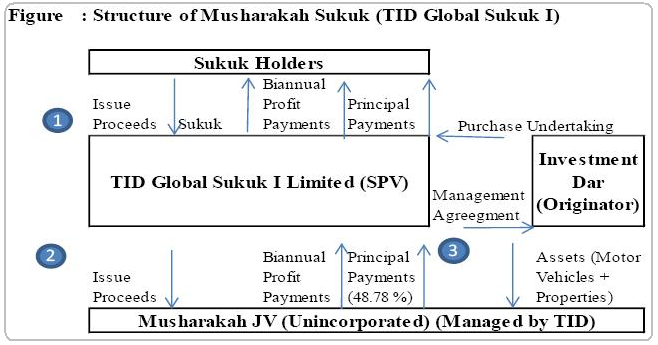

Structure of the TID Sukuk

The Investment Dar reports that in 2005, TID introduced the Sukuk Al-Musharaka (co-ownership Sukuk) with the joint collaboration ABC Islamic Bank of Bahrain with offerings of 6-month LIBOR plus 2% per year while the maturity at five years, in next year TID introduced another three years maturity Sukuk with LIBOR plus 1.75% with the terms of semi-annual distribution. In 2006, the Sukuk prospectus explored the structure as follows:

The figure illustrates that the SPV issued TID Global Sukuk I Limited to the Sukuk investors and primarily through a trust agreement between the issuer and Sukuk holder where the SPV was empowered by Musharakah contract of joint venture and SPV 48.78% of the capital investment. TID as the originator of the Sukuk involved US$157.5 million while the third party and corporate investors supplied rest 52.22% of the investment that amounted US$ 305.7 million Musharakah capitalisation with an asset coverage of into 150 units. To securing the investors, the TID provided the guarantee to repurchasing the SPV shares in the original assets during the final maturity period of Sukuk in order to protect the investors from the unpredicted insolvency event while there is a management agreement linking the originator along with the SPV and the explained structure has approved by the Sharia board.

Reasons for TID Default

The financial performance of TID was excellent until 2007 with steady growth of Sukuk Al-Musharaka and the company accounted KD132 million aggregate profits with aggregate assets of KD 1.27billion while the company backed by owners’ equity of KD 387m, but the company reported KD 80.3 million losses for the first instance. The consolidated income statement of TID illustrated that the company suffered from KD 88.14 million of unrealized losses, injurious investments associates non-payment KD 61.6 million, KD 12.1 million blocked to the financial institutions for twenty funds, and bed debts of KD 8.2 million while TID was able to recover only KD 9.3 million of it cash investment. In 2008, the company directly and indirectly influenced with the global financial crisis and TID failed to Sukuk holders profit distribution due to liquidity crisis while the short-term liabilities notably gone beyond its liquid assets; in December 2008 the investors and the associates went to the court and claimed to recover their investment from the TID assets and collateral.

Restructuring TID

In 2009, TID came into an agreement with its sponsors, creditors, and investment managers to freeze up the claims for the interim period until the end of 2009; consequently, the deadline had extended up to first quarter of 2010. Al Markaz Law Firm notes that the Central Bank of Kuwait has engaged an administrator by this time to supervise the debt restructuring and to scrutinise the financial accounting system of the company while TID necessitate to having a loan of around US$1 billion in order to refinance its debt obligations and decided to go to the court. A law firm ‘Al Markaz Law Firm’ submitted prayer to the court of appeal under Section 2, Chapter (3) of the Financial Stability Law and the court granted the application arguing that Article 38 that provides the president of the concerned circuit at the Court of Appeal to grant scope of restructuring for defaults.95 In March 2010, a Kuwaiti court granted protection to TID from creditors under the Financial Stability Law that stipulates that court investors no lawsuit or court judgment would be executed against TID in order to provide a chance to the appellant for restructuring until 31st January of 2011, later, the court also approved the revised restructuring plan with extended. The revised plans to restructuring company had incorporated in the strategy with intent to pay back KD 600 million within six years starting from June 2011; however, both shareholders and creditors approved it; alliance of TID and the company made the first payment of KD 82 million within the scheduled deadline.

Challenge of Kuwait Sukuk Case in the English Court

Chuah argues that the case of the Investment Dar Company KSCC v. Blom Developments Bank96 has raised several questions regarding the poverty of the Sharia Law, controversial features of Sukuk, the limitation of Islamic finance, and the weakness of Kuwaiti legal system that has failed to mitigate the conflicts arisen from the Sukuk default.97 The fact of the case illustrated that the Investment Dar (TID) was a Kuwaiti investment company that entered into an agency agreement with Blom Developments Bank where TID has taken the responsibility to invest he deposits of Blom and would provide a fixed rate of return on the investment to the Blom without any obligation of performance. The agreement between TID and Blom had amalgamated with the governing law, it was clearly mentioned that the English law would govern the contract while a particular clause expressed that ‘Wakala’ agreement would be interpreted by the Sharia supervisory board complying with Sharia law. While TID failed to make payment to the Blom, it sued for the recovery of all invested amounts along with the profit in accordance with the specified rate of return and blamed that TID would be liable for breach of contract and breach of trust.

TID argued that under the clause-5 of the contract it has clearly mentioned that the Islamic law would govern the contract and Sharia interpretation is the final decision for any arbitration, the contract has formed totally opposite to the Sharia law as it handled with interest (Riba) that Islam always prohibits. The claimant reasoned that the clause-5 of the contract would be a breach of contract, as incorporation of Sharia Law is a matter of contractual performance, but under any circumstances, it is not an applicable law here.98 While the case motioned in the court, it raised tremendous unrest among the Islamic financial institutions, and Sharia supervisory boards of Kuwait as the instruments were certified as Sharia compliant, thus their speculation was that a secular court might not dare to challenge an Islamic law compliant instrument.

The court was remarkably sensitive to the concern, but Bank Shamil of Bahrain v. Beximco both parties had agreed that both the Sharia and English law would govern the contract, but two legal system couldn’t be an applicable law for a single contract and the Court of Appeal verdicts that English law would be applicable law. In the summary judgment, the court held that contract between TID and Blom had ultra vires as TID Article does not allow it to invest anywhere that is not Sharia compliant and the contract itself was complete opposite to the Islamic law and the contract was void, where Blom has mistakenly invested under an unenforceable contract. Thus, the judge added Blom is bound to succeed with distinct principles of reimbursement in English law, the onus of formulating a debatable case that raised question regarding the enforceable law of contract, judicial intervention into the Sharia practice, capacity of the foreign law to put into Sukuk in the secular jurisdiction.

Whether Sukuk be used heavily in Kuwait’s financial markets or not

From the last decade, the capital market of Kuwait has experienced remarkable expansion in terms of issuance of conventional bonds and Sukuks due to the regulatory framework to oblige the provisions of Sharia law; in addition, the capital market experienced growth after recovering the national economy from global financial crisis in 2008. At the same time, it was possible for the government to emphasis more on the long-term infrastructural development projects by increasing the number of issuance of Islamic bonds; therefore, the policy makers of this country have concentrated on circumspect approach to lending and borrowing, and to controlling the capital market effectively. In this process, the government has faced severe challenges in different stages of supply chain management, such as, poor governance of future offerings and lack of regulatory framework to control of the financial market raised the tension of default Sukuks or other financial risks. However, the government has already enacted new law with intent to control capital market more effectively, restore trust in locally originated Sukuks, and develop national economy by issuing new bonds in accordance with the provisions of this legislation though it should require additional time to assess the impact of this law in the market.99

The US$190 million issue of Gulf Holding Company with other Sukuks will be matured by 2013; however, the development of the Sukuk market in Kuwait was unexpectedly shortened because of the global financial downturn in 2008, for instance, in 2010, issuance of Sukuks with conventional bonds reduced by 27.6% from the previous fiscal year. According to the report of the central bank of Kuwait, issuance of Sukuk market remained completely inactive though only US$1billion of conventional bonds added in 2010; at the same time, many investors was in under serious external and internal risk factors for which GIH shook the market in 2008, and TID was the first investors, which fall in default. Therefore, new Sukuk issuers lost their confidence to invest in this segment to raise capital at the period of recessionary economy; however, in 2009, TID avoided liquidation and GIH had signed many formal restructuring contracts with investors and changed strategies to focus on the core business.

Moreover, GIH had introduced three-year amortizing services with its lending banks; at the same time, the Central Bank of Kuwait approved the restructuring debt of TID; on the other hand, The shareholders of IIG voted in 2010 to decrease the capital by about 55% with intent to save the company from financial crisis. In this context, the government of this country enacted new law in order to add new provisions to introduce a robust governance structure for Sukuk issuance in the future; in addition, formation of CMA will develop the business and investment environment.

From the above discussion, it can be argued that at the initial stage, it was hard for the potential Sukuk issuers to enter in the Sukuk market to increase fund; however, the provisions of new law and the plan of the central bank of Kuwait created a new dimension with many hopes, which will be renaissance in Sharia-compliant activities.

Recommendations and Conclusion

Recommendations

- Most of the public and private listed companies particularly Sukuk issuers in Kuwait had not complied the provisions of Kuwaiti stock exchange for which this country is only 22 out of 100 in SCI in 2009; therefore, IMF had recommended that the legislators should concentrate more on the legal framework containing international standards;