Introduction

Islamic bank is a term used to define financial institutions that are governed by tenets of Islamic laws and regulations.1 Islamic banking system is quite different from financial practices of mainstream banks in more than one way. Basically Islamic banking is similar to mainstream banking in practice and in most other routine functions, however it differs in areas that pertains to interest, profit and loss sharing which are the characteristic features of the Islamic banking system that sets it apart.2 A working definition given by Hassan and Lewis in the Handbook of Islamic Banking describes Islamic banks as financial institutions that “provide a variety of religiously acceptable financial services to the Muslim communities” 3and thereby serve an important socio-economic role.

The Islamic laws and code of practice that governs the profit and loss sharing (PL S) concept are encompassed in the Islamic principles that are referred as Fiqh al-Muamalt.4 Because a major characteristic feature of Islamic banks pertains to it Profit and Loss sharing principle which is what sets it apart from mainstream banks let us briefly review what this concept of PLS entails.

The PLS concept that is a common feature of all IFIs is contained in the bank’s lending principles. The Islamic banks approach to lending is very unconventional in that the bank does not give out the loan to a borrower per se, but instead acquires the asset on behalf of the borrower who is then supposed to institute repayment to the banks in installments. This for instance is usually referred as Murabaha when the loan is made towards mortgage.5

Another unique feature of Islamic banking pertains to its approach on lending; it does not set out uniform interest rates for all companies but rather customize interest rates to match the company financial performance. This means companies with high profit returns are charged more, a concept defined by the floating rate interest on loan system.6 This core values and features of Islamic banking are the backdrop in which we are going to discuss the way in which the concept of Islamic banks financial products differs with those of ordinary non-Islamic banks.

In the following section let us briefly review the major characteristics of Islamic banks and thereby lay the foundation in which the rest of the discussion on this paper will be based. This is necessary because of the way that IFIs are structured which is very different from mainstream banks; thus in order to understand the Islamic banking concept it is imperative we have a background insight on how Islamic banks are structured and how they function.

Background of Islamic Banking

During the start of the 1980 decade, the Islamic banking system underwent a revolution that is still ongoing up to this moment. The rapid rise of the Islamic Financial Institutions (IFIs) during this time was largely attributed to the economic factors that were taking place worldwide. It is notable to mention that during this time the OPEC countries had excess liquidity capital occasioned by oil revenues which significantly excited the business environment and every other sector of the economy.7 The implication of this excess liquidity meant that many OPEC member countries which are mainly Islamic countries were suddenly faced with a vibrant market occasioned by increased cash flows that could not completely be absorbed in the domestic market.8

This created the need to have viable and strong financial institutions that were essential in filling the financial gap that had became glaring in the wake of excessive liquidity capital that was not properly managed due to the weak nature of IFIs that were not up to the task.9 Another crucial catalyst in this chain of events that contributed to the exponential growth of Islamic banking during this period can be attributed to a range of both internal and external factors. Faced with dire constraints of weak financial institutions within their borders and lack of strong IFIs even internationally, most Islamic countries financial policies became more focused in strengthening the available Islamic banks (IBs) in their back yard. As a result, much effort, expertise and financial injection went toward reforming the existing financial institutions culminating to a revolution of the Islamic financial institutions during the late 1980s and throughout the 1990s.

In addition to these challenges, the US dollar had become consistently strong against most currencies of the Arab countries partly due to high rate of capital flight that was caused by absence of solid financial institutions. To counter this problem and obtain a certain level of leverage on the dollar which is still the standard currency of payment for oil exports, strong financial institutions that upheld Islamic values back at home was seen as the key.10 Since this revolution began, IFIs worldwide has been expanding at an unprecedented rate11; as of 2010 the Ernest & Young associates estimates the number of operational Islamic banks worldwide to be not less than 475 fully fledged financial institutions with operations in more than 75 countries and combined annual turnover of US$1 trillion.12 At the time Islamic banking share market for financial transactions was also estimated at 20%.13 In the next few years we can only assume that this market share of IFIs will only continue increasing if the current trend is anything to go by.

In this paper our main focus would be on challenges posed by the current system of Islamic banks as far as unification of international business law is concerned; more specifically this paper will explore at more depth the unique nature of Islamic banks in general and how the various financial products relates with those of mainstream banks. The purpose is to study how far it is possible to integrate the concepts of IFI’s within the current international business law and specifically in relation to international laws and regulations that govern mainstream banks.

An Overview of Islamic Banks and Islamic Principles

The functions of Islamic banks goes beyond the mainstream banking functions in that an Islamic bank doubles up as a trader, investor and a consultant with mandates that has traditionally been profit maximization just like any other financial institution.14 As such the distinct nature of Islamic banking has advantages that arise as a result of its unique financial transactions and which unfortunately is also its disadvantages. The major advantage of Islamic banking is confined to the banks concept of Profit and Loss Sharing (PLS), in this arrangement the banks depositors are strictly speaking not creditors to the bank, but rather very similar to shareholders who stand to absorb a certain percentage of the banks profit and losses as outlined in the banking contract.15 The implication of this arrangement is that Islamic banks are more insulated from financial losses that emanate from depositors capital than their conventional counterparts.

The disadvantages that are inherent in the Islamic banking system are proportional to the advantages that the bank enjoys in respect to the depositors funds. The same contract between the bank and the depositor that provides for risk sharing also contains components that protect the depositor from non-procedural banking operations that can results in losses.

In such a case the bank is obligated to compensate the depositor with full deposited funds or face legal actions, in what is usually referred as Fiduciary Risk.16

Closely associated with this type of risk is Displaced Commercial Risk, a form of risk that Islamic bank are exposed to whenever they move to top up the depositors “perceived profit sharing”, to be at par with interests that conventional banks are offering at the time.17

This is despite the fact that the bank profits might not be sufficient to provide for such percentage but which they are compelled to pay or face depositor’s financial sabotage. In order to do this the bank has to re-allocate the bank shareholders funds by toppling their profit sharing obligations to cover the shortfall.18 Other areas that the bank faces risks are in areas of collateral, market risk, credit risk, and bank equity since Islamic bank significantly differ with conventional banks in terms of funds mobilization.19 Indeed, the current way in which Islamic banks calculate Capital Adequacy Ratio (CAR) is an indicator of their unique banking system (Basel.org). Because of Ijarah or Murabaha the IFIs has adopted a form of a matrix format to calculate CAR at any given time during the various stages where a borrower is servicing the loan.20

More so the bank risk changes from price risk to credit risk, a feature which must be incorporated in CAR calculations. The implications of CAR in Islamic banks and how it generally impacts on various securitizations transactions that are also unique in IFIs would become apparent as we continue with our discussion in later sections. In fact, what we realize is that many financial products of Islamic banks including the core financial principles of Islam such as profit-loss sharing and sukuk have not been provided at all in both Basel accords. This is a major oversight when you consider that Basel is the universal financial body with mandate to provide financial guidelines to all financial institutions globally.

An Islamic concept that will be at the centre of our discussion throughout this paper is referred as sukuk; sukuk is the equivalent of what the conventional banks refer as bonds, but which does not provide for fixed interest rates or indeed any form of interest-based returns on investments at all.21 As a result Basel I capital adequacy guidelines for instance are limited insofar as application of these guideline in calculation of CAR is concerned where sukuk exist; nevertheless, the “Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI) provides a workable framework”.22 Islamic banks are therefore able to calculate most forms of credit risks using standard approach method, but there are other cases where credit risk calculations do not apply such as in Musharaka and Mudaraba.23

In such cases the banks normally applies specialized lending guidelines that are outlined in Basel II such as the “supervisory slotting method” or the “equity position risk in banking book method.”24 Despite this, Islamic banks continue to face challenges and unique risks as well such as the Sharia Compliance Risk;25 this is a form of risk faced only by Islamic banks which include financial losses encountered due to financial transactions that arise from non-recognition of specific sources of incomes or losses associated with compliance to Islamic banking regulations.

In the following section we shall discuss in summary the major Islamic principles that govern IFIs financial regulations with special focus to securitization. This is because securitization in Islamic banking is a fast evolving concept that is rapidly becoming popular although has taken shape over the last few decades agitated by the securitization trend that has been taking place in the mainstream financial institutions. The processes of securitization transactions were first invented back in 1970s; during this early period securitization transactions were predominantly used in transformation of asset pools that were mainly compromised of mortgages, referred as murabaha but have over the years been customized to apply to other IFI’s financial such as Salam, Musharaka, Ijaran and Istisna product as we shall see.26

Basic Islamic Principles

Because the securitization process in Islamic banks is governed by shariah laws as well as the Islamic financial principles, let us briefly review the major Islamic principles that are applied in all forms of business transactions. There are just a handful of fundamental Islamic laws that are integral in almost all forms of business deals, these are; ban on riba which is interest, ban on gharar-maisir, the shariah PLS concept, law on ethical forms of investments and asset backing.27

Perhaps the most fundamental of these laws as we shall see throughout this paper is the ban on riba, in fact it is the law that is always kept in mind when designing all forms of IFI’s securitization products because interest-based transactions are completely not permissible under the Islamic laws.28 It is also the law that is inferred the most times in the Quran which would mean its importance is greatly empshasized; in a nut shell the shariah law on riba states that “Allah hath permitted trade and forbidden usury.”29

The Islamic law that prohibits gharar-maisir which mean business transactions that are undertaken on “excessive uncertainty” is seen to imply from an Islam perspective not to engage in gambling-like business activities.30 This Islamic law effectively prohibits trade practices that are described in conventional banking as speculative trading whose level of risk are as high as the expected return on investment which would be in reference to transactions such as gambling, betting, lotteries and such similar games. PLS sharing concept is a fundamental law in Islam just as the law on prohibition of riba; every aspect of trade undertaken in compliant of Islamic law must be based on equal sharing of profit and loss that is proportion to their investment.31 This in practice implies that the interest-based trading which is prohibited in Islam would have no room in trade transactions.

The other Islamic law requires that all form of investment ventures be undertaken for a good cause that enhances the welfare of the community.32 It is for this reason that Islamic transactions are very particular at establishing the legitimacy of asset pools which is one of the steps that must be undertaken in securitization of assets. Finally, all forms of trade must be asset-backed; this implies that money must be channeled through an asset in order to generate the required profit which will be shared in accordance with PLS concept.33 Without asset-backed transactions shariah law prohibits any form of profit to be gained from such a transaction. Now, with this in mind we can undertake a critical analysis of the concept behind Islamic banks financial products, the principles governing them and how they differ with similar financial products of conventional banks.

The emergence of securitization concept and its uniqueness in Islamic banking

Since this paper also intends to investigate the main similarities and differences between Islamic finance and the normal finance, our focus on this section will be on analyzing how Islamic banks have securitized their financial products and how this differ in conventional banking.

The various securitization transactions that exist in Islamic banks were first made popular by introduction of Islamic Private Debt Securities (PDS) that first took root in Malaysia. It was during this time that the most common Islamic securitization transaction referred as murabaha become very widespread.34 As Islamic banks continued evolving and expanding throughout 1990s and 2000s, more securitization transactions were invented and currently includes a range of several such transactions.

To understand how the various securitization transactions has gradually evolved in the Islamic sector, one would have to understand how IFIs utilizes depositors funds; to this regard there are three forms of applications in general that Islamic banks can commit their funds. One of the most popular applications among these three is a form of contract which are referred as exchange or fixed income instruments. In this category we have four major contracts that the banks have invented; murabaha, ijara, salam and Istisna.35

The major advantages of this category of fixed income contracts are two; one, because they provide the bank with minimal risk exposure, and two because they are relatively easy to implement.36 As we get to discuss these various securitization contracts in detail we shall see how this is so. The second category in which the IFIs can commit their funds is referred as Profit Sharing Equity instruments which are mainly two; mudaraba and musharaka.37 Finally, we have a third category that mainly involves commitment of funds in service products which occurs in form of agency services and currency services among others.

Like all forms of securitization transactions it is imperative that the securitization process under the Islamic tenets certify these three conditions. One, there must be transfer of asset from the seller who is the originator upon exchange of pre-agreed financial amount; this is referred as confirmation of a legal isolation that must be “presumptively beyond the reach of the transferor and its creditors.”38 Two, certain rights must be realized by the new owners upon acquisition of the asset which generally involves right to pledge the particular asset for whatever reasons that the owners desire.39 Finally, the securitization process must be structured in a way that would bar the seller from being able to reacquire the asset back.40 In the next section we now take a critical analysis on two of the Islamic financial products, one from each category that are central to Islamic bank principle of PLS, that is Mudaraba and Musharaka since this principle is in fact the main foundation of Islamic banking.

Musharaka

Musharaka is a form of contract financing that is under the category of Profit Sharing Equity methods which means it is basically a form of partnership that provides for profit sharing in accordance with shariah laws. Generally musharaka is very similar to mudaraba in principles; in Islamic laws musharaka is categorized into two forms; shirkat al aqd and shirkat al milk.41

Shirkat al milk refers to a form of partnership on an asset that exists between more than two parties which does not necessarily have to be defined through a form of an agreement such as a contract. A typical example of shirkat al milk musharaka is a form of financial asset that is obtained through inheritance which the shariah law prohibits from being divided among the parties.42 Shirkat al aqd on the other hand is partnership on asset between various parties that has been pre-agreed on various issues that pertains for instance on return on profit and so on.43 In fact, it is the basis on which all musharaka contracts are done because it requires parties to such an agreement to freely engage as well as to negotiate on the specifics of the contract before is has been agreed upon.

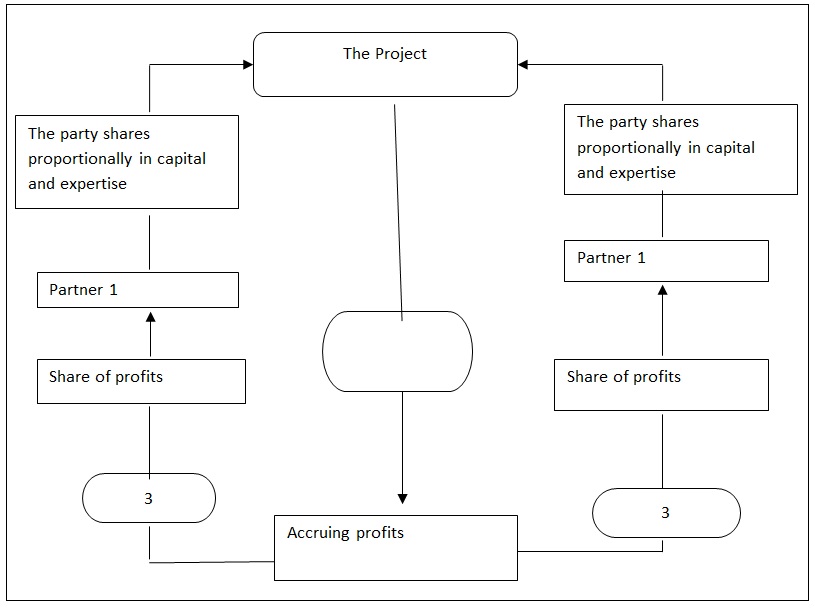

Normally, musharaka contracts involve capital contribution that is inform of cash, even though contribution of capital in form of services is also admissible under sheriah tenets including what is referred as wujuh, to mean “partnership in goodwill”.44 The fact that musharaka contracts is among the most common method of financial products is certainly not by accident considering that it is one of the most straight forward form of contract under Islamic laws. In musharaka contracts, the capital contribution from each party is normally quantified and a framework of profit and loss sharing (which is usually in proportion to the contribution) between all the parties to the contract drafted based on mutual agreement. A typical example of a musharaka contract is depicted below that ideally involve the IB and a client.

In the musharaka process that is depicted above what normally happens is that the IB which in this case is an equal partner with another party who might be a client enters into a contract that involves financing of a particular project. Once the project has been finalized, the resulting profits or loss in that case will be shared among the parties proportionally as originally pre-agreed during the enactment of the contract.

The securitization of musharakah is also undertaken in similar manner and is the mode of generating huge liquid capital that is preferred by governments or large corporations that require injection of massive capital on a particular project.

In this case what therefore happens is that musharakah shares are floated of particular values indicated in the share certificate which the government or a private Company exchanges in return of contribution of funds. The party to a musharaka contract who is actually an investor retains the musharakah certificate that represent the capital contribution of that party to the project venture and consequently the expected value of return on capital in monetary terms.45 This would imply that the party to a musharaka contract has therefore the lee way to transfer the ownership of this musharakah certificate to a third party either at par value or at a premium.

The circumstances in which a shareholder to a musharakah contract can opt to transfer the certificate to a third party at par value or at a discount are different for each of this case. Shariah law requires that exchange of monetary assets be made at par where the elements of exchange are both in cash. Thus, where the shareholders contribution has not yet been channeled through the intended capital in order to generate the envisioned earnings that necessitated the securitization process in the first place, then the musharaka shareholder can only transfer such share certificates to secondary market at par without charging any form of premium.46 Besides, the fact that this is mandatory under the Islamic laws serves to prevent financial risk of investors money that would result whereby the value of the liquidity capital would be less than the worth of musharakah share in the market which would be the case if premium was charged upon transfer while no generation of profit was taking place.

However, if the liquidity capital has already been channeled towards a project that was already generating earnings, it is permissible for the musharakah to trade on the certificates of shares in secondary market at a premium. A confusing scenario that often happens when it comes to musharakah securitization is where the initial generated capital is invested in part. This means a proportion of what was originally contributed has not yet been utilized while another certain percentage has been used to obtain assets. This scenario remains contentious among Islamic jurists and there are conflicting positions as whether such musharakah certificates can be traded in secondary markets at a premium or not.

Murabaha

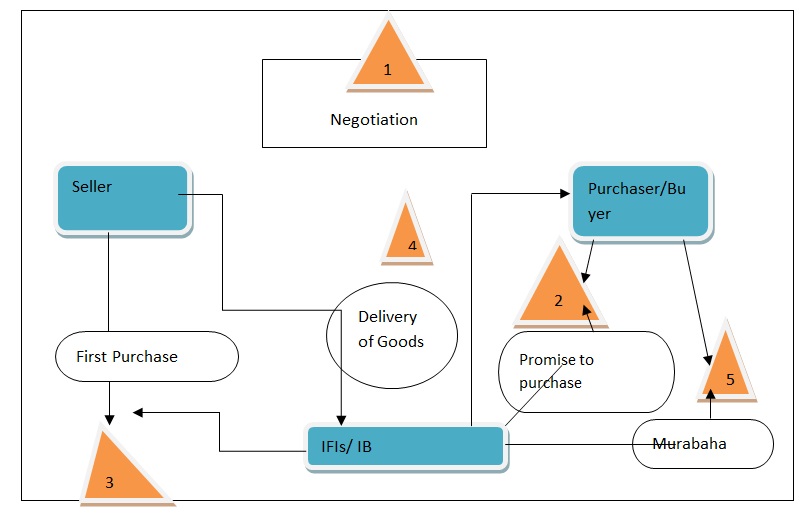

In Islamic banking murabaha entails what can be termed as Cost-Plus Sale contract; in its simplest terms, murabaha entails a securitization process that is only structured to generate a certain profit to the investors. Under shariah laws, murabaha entails a sale contract that can take either of these two forms; installment credit made to the bank or form of deferred payment sale.47

Thus in murabaha, either way the buyer has to institute payments that are made up of the principal amount in addition to the pre-agreed profit. A murabaha contract may involve other parties rather than the buyer and the seller which is the bank; when a third party is involved in the transaction to function as an intermediary between the two principle parties, that party becomes an agent usually referred as wakil.48

Thus, the simplest form of a murabaha contract involves a buyer and the bank, which would normally appoint an agent whereby both parties agree on the mark-up price of the sale that should be paid at the end of the transaction period.

A typical murabaha contract and the transaction process that result from these agreement is well elaborated on this simplified chart which clearly depicts IFIs as the financier that secures the goods on behalf of the buyer.

This process is what is referred in Islam as bai’al-inah to mean a transaction that involves sale and buy-back which under Islamic shariah law is perceived as riba-based borrowing and therefore prohibited.50 This is because the point of laundering the financial asset between the bank and the customer is for purposes of creating interest on a debt-asset, which the Islamic shariah law saw as unwarranted riba. The murabaha-BBA is thus normally frown upon by many Islamic banks. Besides, the process of sale and buy-back that results from this form of securitization leads to separation of financial assets from the mode of financing which is also not allowed under the Islamic tenets.This is the ideal form of murabaha contract that is permissible by Islamic banking since it is a securitization process that conforms to the Islamic shariah laws, notably because the same goods are not sold again to the seller at an interest as is the case in another variant of murabaha that is only found in Malaysia referred as mutabaha-BBA (bai-bi-thamin ajil).49 In this form of murabaha, the banks initiates sales of assets to SPE Company through the normal mudaraba contract, thereafter the bank then buys the same assets but this time with a mark-up value that would be paid on deferred basis.

Islamic Finance & the International Business Law

To understand how Islamic finance interacts with international business law it is necessary to understand the conceptual background of international laws which is the context that Islamic finance will be operationalized. In general international law that applies for each jurisdiction is encompassed within the wider framework of legal system that exist for that specific country which comprise of three branches of law; civil law, common law and theocratic law.51 Theocratic law is what will be our focus in this section since it is the branch of law that applies to Islamic financing and is described as the category of laws that are “based on religious precepts” such as Islamic finance.52

The major differences between theocratic law and these other forms of laws as we shall realize later on is that in theocratic law the legal code is dictated by scriptures which allows little if any room in differed interpretations. On the other hand both common and civil law are different in that the judge is often the person interpreting the law that is formed through constitutional means. One of the concepts that are widely used in regulating financial practices in the international arena both in conventional and Islamic banks is Capital Adequacy Ratio. So in the context of Islamic finance let us discuss what this requirement entails.

International Financial Regulations

Capital Adequacy is a financial term that is used to define the regulatory guidelines that requires financial institutions such as banks to reserve certain percentage of their Primary Capital Base that is consistent with the institutions lending.53 A bank must ensure that it capital base assets is at a minimum of 8 percent of its assets, the rule of thumb that applies is “lending of $12 for each single dollar of the bank’s capital, this is what is referred as Capital Adequacy Ratio (CAR) or at other times Capital to Risk Assets Ratio (CRAR).”54 The purpose of calculating capital adequacy is to ensure that a bank is not exposed to financial risks that are caused by the lending policy of the institution. As we shall realize later calculation of CAR in Islamic banks using this framework is impossible due to the uniqueness of its financial products some of which we shall discuss briefly in this paper.

In many countries government regulations requires the financial institutions to comply with the minimum acceptable level of Capital adequacy which is the other reason why banks need to establish their CAR. The Basel Committee on Banking Supervision framework which is one of the most widely used financial guideline globally redefined the international Capital Adequacy standards on 2004 that are now used to regulate financial institutions currently.55 Basel committee is a body that was found in 1974 in Basel, Switzerland with mandate to develop regulatory frameworks for financial institutions in the wake of international financial market shakeup that affected reputable bank institutions worldwide. In fact Basel conventions has particular use in regulating financial regulations for both IFI’s and conventional banks and we shall therefore focus more on it in order to analyze the general implications of the Basel 1 and 2 accords on Islamic banks as well as explore in depth the Basel accords structure and recommendations.

Basel Convention on Capital Adequacy

The general idea behind the formation of Basel committee was to provide a forum where member states can hammer out the modalities of cooperation on banking regulatory and oversight matters between themselves.56 Besides this the committee had the mandate to align the various countries approach to financial practices worldwide regardless of their religion affiliations as is the case of IFIs. In order to achieve this vision the committee set out three approaches that would enable realization of this goal namely: facilitate key financial information on bank supervision, strengthen the banking supervisory tools for compliance purposes and finally develop minimum supervisory guidelines.57

The first frameworks that Basel Accord advanced in 1988 on capital adequacy was limited to assisting the financial institutions address the credit risks that they faced. It was a form of crude calculation of capital adequacy in comparison to the current standards; it assumed factoring of bank credit risk will also consequently address other form of risks inherent in banking financial transactions, a fact that was only partly true.58

The 1988 Basel I convention on capital adequacy was limited in terms of width and depth in the way that it approached CAR calculation. Basel I framework on Capital Adequacy was determined by two major factors that included credit risk and standard weight: standard weight calculation was limited in it calculations of weighted risks.59 Basel I accord focus, was therefore on setting the minimum possible capital levels for financial institutions and also ensuring that banks embraced low value assets as collateral. The flip side of this rationale was an increased risk to financial institutions brought about by incomplete analysis of the dynamic market parameters. In the years that followed Basel I accord was amended several times to incorporate and reflect changes in the financial sector. These changes further strengthened the current international financial regulations of banks from unforeseen risky outcomes.

One such amendment was in 1996 for market risk that saw the CAR expanded to incorporate the risks associated with other financial market force. However, even then Basel I accord had still other inherent limitations. The Capital Adequacy calculation for instance did not provide an accurate and reliable financial guideline for determination of CAR.60 Another disadvantage under Basel I accord was the tendency of the banks to undertake regulatory capital arbitrage which enabled them to manipulate their core capitals in order to reflect favorable capital assets that made them compliant, lastly the accord did not offer ideal risk mitigations approaches to banks.61 Hence Basel II was born in 2004 to address these shortcomings and incorporate other challenges that banks were facing in the financial sector.

Capital adequacy is a financial concept that has been very effective as a framework for mitigating risks that are associated with financial transactions in banks, and which the Islamic banking system has sought to embrace by customizing them in a way that provide the same advantages to their institutions. Although Islamic bank are not in the mainstream the impact they have on the world financial market is significant.

Principles of Capital Adequacy

The new Capital Adequacy calculation is guided by three core principles that are referred as pillars: “market discipline, operational capital requirement, and supervisory review.”62 Pillar number one pertains to regulatory capital of three critical risks that a bank encounters during it routine financial operations; these are “market risk, credit risk and operational risk.”63 For each of this risk the accord provides various calculation techniques that set the desired level of accuracy such as standardized approach, foundation Internal Rating-Based (IRB) approach and advanced IRB for calculating credit risk.64

The second pillar tackles the other forms of risks that are not included within the first pillar but which financial institutions are more likely to encounter, such risks include liquidity risk, legal risks, concentration risk and pension risk. It also provides bank supervisory regulators with guidelines for determining bank compliance. Pillar two also requires regulators to assist financial institutions in developing internal systems for determining their capital requirements. The last pillar focus is on market discipline which includes banking ethical standards and accepted business practices that promote bank financial stability.65

The underlying working definition of capital categorizes banks equity into two groups: tier I capital and tier II capital. Tier I Capital is defined as the actual equity inclusive of retained earnings while Tier II Capital is the subordinated debt in addition to the preferred shares.66 Tier I capital are financial institutions assets that can absorb financial losses of a bank during trading without necessitating the bank to enter into bankruptcy. Tier II capital are the other type of assets that are reserved primarily to absorb losses of large magnitude during the event of bankruptcy. While the current Basel II accord has gone a long way in addressing the unique financial characteristics of Islamic banks more adjustments to CAR are needed in order to fully cater for this form of banking system.

The core capital is a sum of both Tier I and II capital while assets in this case refers to the weighted assets or the minimum requirements as set by the banking regulator, such a ratio should not exceed the Basel accord threshold level that is set equal to or less than 8%.67 The CAR is further adjusted to calculate the three other subcomponents of the capital adequacy namely: standardized approach, basic indicator approach and advanced measurement approach that offer varying degree of accuracy.68

An integral component of current CAR calculation is the risk weighting of a bank’s assets which assigns a percentage figure for each category of assets based on the probability of credit risk that might occur for each category of the assets.

For this purpose the approach used in calculating risk weighting requires the bank to categorize the nature of the assets into two: fund based assets and non-funded assets.69Fund based assets usually include bank investments, loans and liquid cash at its disposal, while non-funded assets include items in the Off-Balance sheet that are first taken through a series of conversions in order to ascertain their true value. For instance government debt and bonds are usually assigned zero percentage on risk weight, mortgage loans attracts 50% risk weight and 100% for all other forms of loans advanced to borrowers.70

Further changes to the existing CAR calculation guidelines continues to be included in the Basel accords on capital adequacy, most recently in July 2009 which incorporated other factors in market risk and incremental risk calculations. This new modifications of capital adequacy calculations provides Islamic banks with basis for incorporating the unique features of their financial transactions, more importantly the Islamic Financial Services Board (IFSB) has played a major role in the way that Basel II has addressed the controversy that surrounds capital adequacy calculation and in lobbying for the concepts used by Islamic banks to be included in future Basel guidelines.

Case study

One of the classical examples of a case that exemplifies the differences that exist between Islamic banks and conventional law within the context of international law is that of M. Aslam Khaki v. Syed Mohamad Hashim, 2000.71 This is one of the most interesting cases in that the issue at hand crosscut several key principals of Islamic finance and highlighted how it conflicted with international business laws; more importantly the issue being arbitrated concerned interest which is one of the basic principles of Islamic finance. In this case the ruling that sparked the interest in studying this issue is one by the Supreme Court of Pakistan that “struck down the use of interest on all loans and bank deposits, including personal loans, commercial and corporate loans and interests paid by the government on foreign loan.”72 Since then this case has been subject of debate by no less than dozens of Islamic scholars and remains to date unresolved.

Following the above mentioned ruling, the same court made another turnaround ruling in 2002 that overturned the earlier ruling thereby allowing payment of interests arguing that “invalidating the payment of interest to non-Muslims would pose a high degree of risk to the economic stability and security of Pakistan”.73 Foremost, if anything this ruling just highlights the incompatibility of international business law with that of Islamic banks. Indeed, in its most recent observations the Supreme Court concurs that such a position will prove to have great ramifications to the country’s economic wellbeing which is a factor that probably contributed to overturning of the earlier ruling. The fact that the Supreme court of Pakistan is again reconsidering reversing this ruling indicates a court thrown in limbo in trying to reconcile two parallel financial concepts that are both too uncompromising to allow for a neutral ground.

Let us review the major incompatibilities between Islamic finance and international business law that were brought forth due to this ruling are several. The first and obviously the major one is the factor of interest-based trading; in Islamic finance the argument that interest should be paid on capital or money deposited is tantamount to treating money as a commodity instead of a medium of exchange which is prohibited by shariah laws. In Islamic laws money that have not been invested in a business venture cannot be charged interest as that will mean trading money at higher value that exceeds its face value.74 Indeed this is the major reason that Islamic banks goes to great lengths to ascertain that condition such as this are met when dealing with any assets; one such example is the way that IFIs goes about when securitizing assets.

In Islamic banks securitization of assets for instance is undertaken in similar process that exists in mainstream banks and requires creation of SPV which will have the mandate to issue the sukuk bonds to the investors. However, under Islamic laws the securitization process must be structured in order to adhere to shariah laws that govern the financial principles of IBs; for instance it is paramount that the asset pool of securitized assets not be from any proceeds of haram earnings.75 In addition, shariah laws require that the investor be given a certain shares of ownership in any securitization process which is usually achieved by transfer of certain ownership rights. Finally, the basis on which investment is made under Islamic laws must be anchored on partnership that advocates PLS concept rather than interest-based financing.76 All these conditions are very different from conventional banks similar financial products.

An integral component for all these securitization process involve a common element that is referred as mudaraba but which is referred as SPE in the mainstream banking. In Islamic banking, mudaraba refers to the investors who are willing to obtain the financial assets in exchange of liquid capital while mudarib refers to the Company that is fronting the securitization of the assets. In Islamic banks, the nature of securitization that the bank transacts in is largely trade-based, termed as murabaha or leasing based, ijara.77 Ideally, the process of securitization in Islamic banks involves the original transaction of the financial asset to the acquiring bank which would later become the originator under the frameworks of murabaha when the transaction is trade-based or bai-bi thamin ajil when it is lease-based.78

Because, the acquisition of such assets are undertaken out of debt, the Islamic shariah laws prohibits riba in their resulting transactions which means that they can only be transferred to a third party at par. The securitization process requires creation of SPE just as in conventional banking industry which has the mandate to manage the pool of assets. Because, acquisition of these financial assets by musharaka, whom represent the SPE in IBs does not change the fact that they are assets advanced on debt, further transfer of these now liquidated assets can still be only at par. This means a secondary market in the securitization chain when it comes to Islamic banks would not exist.79 A securitization process that is unique to Islamic financial institutions is depicted in the following diagram which articulately presents how the same process in mainstream banks has been customized to reflect an Islamic securitization process that is shariah compliant.

What is different in this process is that under Islamic laws the securitization process must also involve two other processes; one, a verification exercise that assess the compliance of asset pool with shariah laws and two, the business deal structure which involve issues of credit enhancement and so on.80

The other way in which Islamic financing differs with the tenets of international law is in their concept of loan, and this we can see in the way that they approach securitization of assets as well as Islamic banks principles on riba.81 In Islamic banks issuance of loan is not taken as a mean of generating income for the institution as is the case in mainstream banks since this will constitute trading on money as we have seen; to get around this there are several financial products that IFIs have designed to solve this challenge. It is such financial products that Islamic banks have often customized in their bid to embrace some of the concepts from the western countries which have ended up being very controversial and more often unresolved as is the case in the Pakistan Supreme court ruling and others.

Challenges experienced by Islamic Banks

There are several challenges experienced by Islamic banks in as far as securitization of its financial products is concerned. In IFIs the importance of asset securitization which is the main way in which it uses to customize its financial is well elaborated to be crucial by various research studies because of the economic benefits that it provides to the institutions as well as other stakeholders in what is referred as maslaha. However, as we have seen securitized Islamic financial products must be in accordance with shari’a laws which mean that these products are constrained from benefiting optimally in the financial market place for several reasons. Foremost, the fact that IFIs have only evolved recently over the last three decades or so, means that they have been late in adopting this concept of securitization from mainstream banks from where it was originally invented and therefore not yet fully refined to be in accordance with Islamic regulations.82 Secondly, Islamic banks have a challenge of ensuring that securitization transactions are compatible with the Islamic shari’a laws and tenets; while the essence concept of securitization is allowed under shar’a law, there are nevertheless other aspects in securitization that could be contravening some of the Islamic shari’a principles such as gharar and riba as.83

Another challenge that faces Islamic banks when it comes to transactions involving securitization is conforming to the shari’a law of riba; because sharia law prohibit IFIs from transacting in types of asset which provides for interest, Islamic banks must therefore find a way to circumvent this condition. A research paper by Zaher and Kabir states that “the Islamic community has rationalized the elimination of riba interest based upon values of justice, efficiency, stability and growth” to be the core values that are integrated in all forms of IFIs.84 Four, the sharia law prohibits transfer of financial cash or debt between parties at a premium since this will constitute interest which is riba.85 Thus to determine which type of financial assets qualifies to be transferred at negotiated price and which must be transacted at par, the rule of thumb is to ensure that physical assets and financial claims are apportioned in such a way where the physical assets accounts for majority of shares above the 50% mark,86 otherwise any resulting securitization transaction must be transferred at par; this is both rigorous and time consuming.

Finally, because of the sharia laws constraints in which Islamic banks operate under, the implication is that securitization process in IFIs is strictly defined in order to avoid contravening the Islamic financial principles thereby limiting the rate at which securitization occurs in IFIs as well as complicating the whole process87. Having discussed in general the special challenges faced by Islamic banks as far as securitization is concerned let us discuss other challenges experienced by IFIs in general.

The Islamic law provides a structure for implementation of financial contracts, commercial and transactions; nonetheless, company laws and commercial banking suitable for execution of financial contracts and Islamic banking do not prevail. These contracts are considered as selling and buying goods and for this reason are taxed twice.88 The banking, commercial as well as company laws include stipulations that are only just described and exclude the Islamic banking extent of activities in the conventional limits.

The other challenges is that arbitrations in court of laws that involve Islamic banking are subjected to similar legal system plus are carried out by judge using common and civil law codes whilst the environment of the Islamic legal system is absolutely different.89 In nonexistence of Islamic banking laws, the implementation of accords in courts might need additional costs and efforts; thus, companies’ laws and banking in some nations need appropriate alterations to offer a level-playing ground for the Islam banks.90 Additionally, global recognition of financial contracts in Islamic banking needs them to comply with both Shariah laws as well as international business law such as civil law and common law systems which we have seen to be mostly incompatible with each other.91

Assets funded through Murabah and Ijara are not indicated on the Islamic banking statement of financial position since the bank is not allowed to own asset or property and enter into some type of trade, this means that international financial regulations becomes impossible to apply at times in IFIs.92Another challenge is that in Islamic banks, deposits are normally based on loss and profit principle (Murabaha or Musharaka) and if anything takes place and the Islamic bank make losses this must be passed on to the depositors. This is the major barrier to mobilization of deposit in Islamic banking; in a number of instances, it results to funds withdrawal.93

Islamic prudential rules are likewise significant, currently deficiency of efficient prudential rules is a weakness to Islamic financing; for example, leasing prudential policies are implemented to Ijara where they have different character, like taking advances. Thus taking advances result to conversion of ijara contract to Musharakah, while Ijara regulations are implemented to it which is unlawful under IFIs regulations.94

Another threat facing Islamic financing is fatwa (religious ruling on Islamic laws matters set by scholar) since it works beside the agreement of fatwas; such an agreement is needed so as to ease execution and intricacy difficulties that comes with such contracts plus to reduce the Islamic financial structuring cost of the products.95 This in general tends to limit utilization of Islamic financial products. In addition, the different interpretation on Islamic law given by fatwa raises the discrepancy amongst leading customers, investors and the products of Islamic financing to be unsure concerning the compliance to products offered by shariah. This at best has contributed to the confusion that surrounds Islamic financial concept and has progressively resulted to loss of confidence in Islamic financing altogether.96

There exist organisations and bodies such as AAOIFI (Accounting and Auditing Organisation for Islamic Financial Institutions) that attempts to hammer out a common framework of Islamic banking with intention of standardizing Islamic laws.97 Nevertheless, without incorporating the religious experts’ agreement, there exist no universal set and binding Islamic banking laws; the problem is religious experts interpretation on Islamic laws more than often tends to differ.

Additional challenges faced by Islamic financing are the limitation of competent professionals at every stage who have know-how of both Islamic laws and conventional banking. An individual with awareness of conventional system of banking may easily comprehend the products of Islamic financing; however, one may not effectively build up as well as advertise the product with no knowledge of the regulation exclusive to Islam.98 The speedy development of Islamic financing implies that the sector is not able to generate adequate experts required to sustain this growth. Currently, most interested professionals functioning in this sector have insufficient time to get the needed skills to facilitate them to proficiently deal with or counsel on transactions involving Islamic finance. This deficiency of experts is upsetting and hampers the development of the sector.

Generally, assets in Islamic finance are relatively illiquid and long-term but this is not an issue since many Muslim nations have cash.99 Although, under common conditions of the market, the divergence between the assets duration that are illiquid and long-term liabilities that are short-term may present severe challenges as manifested by the liquidity constrict; it is such features from western banks that Islamic finance are adopting that have led to severe weakening and near international financial meltdown.

Particularly the liquidity risk is severe for Islamic financing since the market that complies with shariah is almost non-existent plus the Islamic banks might face several limitations when pattering interbank instruments.100 Additionally, the IFIs are forced to run excessively liquid statement of financial position because of this challenge, thus giving up profitability and in the end destroying the owners’ of the firm value. Banks may actually face two forms of liquidity issues; liquidity shortage and excess liquidity. A number of banks may have liquidity shortages, when the money is withdrawn by depositors plus bank has no surplus to finance its short-term. On the other hand, bank’s faced with excess liquidity may not have any hint where to invest for short-term.

There is no doubt that the major critical challenge faced by Islamic banking is confidence creation in the depositors plus other operators. Where traditionally structured Islamic banking products are somewhat simple, identical products that are customized from conventional banks have a tendency of being more complex. In such cases Shariah conformity frequently results to extra needs in the process of structuring that in turn results to superior costs of transactions.101 Although, a mixture of initiative and perseverance has facilitated the sector to overcome numerous inherent obstacles thereby creating a sector which is growing gradually and which have steady evolution of financial products.

Additionally, the sector is facing a deficiency in short-term products of investments; in Europe and GCC, the Murabaha funding is mainly utilized as a short-term funding instrument. A number of Islamic banks tried to make-up substitute products, though they were challenged by their incapacity to produce assets originated by liquidity issues and credit ratings associating to their statement of financial position.

Before 2008, the market of sukuk had been going through explosive growth but in actual fact, the international sukuk market in 2007 had more than doubled plus was on trail to posting inspiring development. But this development has evidently slowed at the start of the fiscal year particularly that of sukuk denominated by U.S. dollar as well as the sukuk primary market.102

The exceptional development and size of Islamic financing have begun to draw the interest of global actors and numerous new identical entrants; thus, numerous conservative banks are currently providing Islamic services and products through the use of “Islamic Windows” in a normally self-reliant subsidiary.103 This in general has led to emergence of dubious Islamic financial products that are not consistent with Islamic law as many Islamic institutions have organized to provide more aggressive services and products to capture the market share. As clients’ financial complexity and awareness rises, consequently do their anticipations of superior quality service; presently individual are more focused to rapidly obtaining finance approvals which further strain the challenges faced by Islamic banks.

Besides, the requirement of accountability plus transparency in the international financial markets resulted to an extensive level of new rules for Islamic financing, on top of meeting AAOIFI and global regulations like IAS 39 as well as Base II they also need to comply with their traditional shariah laws.104Similarly, every financial institution should be able to attain local rules operational and reporting requirements. This perhaps is a challenge, particularly in non-Islamic nations where controlling banks (central) and any other governing bodies may enforce requirements that deviate from Shariah principles and standards.

Additionally, Islamic banking sector must reconsider to cater for the demand of extra complex services and products that are expected to continue emerging while all the time ensuring that they are consistent with Islamic shariah laws. It must be innovating instead of duplicating the conventional system of banking services and products that attain the developing requirements of its clients.105All in all Islamic financial institutions seems to be facing insurmountable challenges as we have seen above which it must strive to overcome if it must succeed in the international financial arena. Consequently, there is no doubt that these challenges poses great obstacle towards developing a common framework that aligns Islamic finance with international business law.

Recommendations

Because of the unique nature of Islamic financing, any strategies that are aimed at addressing its shortcomings will have to be multi-sectoral; the following strategies can be effective in addressing the challenges faced by IFIs.

Financial engineering

Financial engineering entails the plan, development plus execution of inventive financial instruments with procedures over and above the preparation of resourceful solutions.106 The engineering can result to new client-type economic instrument, processes, security or even innovative resolution to issues of corporate finance, for instance the requirement of lowering financing costs, managing risk better, or increasing the investment returns.107

Financial engineering should initiate new shariah services and products to the Islamic financial bodies which improve liquidity, portfolio diversification and risk management.108 Normally, efforts that pertains financial engineering practices to Islamic financing will necessitate significantly commitment of huge resources so as to meet the demand of financial intermediaries, investors, plus entrepreneurs for safety and liquidity; securitization is the main contender for the economic engineering. New economic improvements are required to spur the demand for financial instruments on both sides of development system; extensively short-range deposits plus investments which are long-term are therefore necessary.

Money markets compatible to Shariah do not currently exist plus there is unequal Islamic interbank marketplace where institutions may place, say, for the night finances or may use to assure a requirement for provisional liquidity.109

Diversification and risk management

Economic markets are developing into more interdependent and integrated concepts, the present signal of globalization and liberalization of capital market is timing the requirement for improvement of risk management instruments, particularly for emerging markets and developing economies. Offering a more varied combination of Islamic financial products or distributing risks in a greater geographic area means less financial risk is experienced by IFIs. Geographic development of base of the depositors for Islamic institutions may attain diversification on the side of liabilities; asset-side diversification on the other hand may reduce the inconsistency in returns that ensue from financial intermediary claimholders. Geographically spread products may further assist the financial institutions to enhance credit risk through choosing borrowers with superior credit plus ratings and shunning those having weak credit.

Financial non-intermediaries services

The function of intermediation must be extended further than its conventional unit; especially it is required to widen the scope of financial services provided. Having this role the Islamic banks may serve as a single stop shop serving various kinds of clientele by providing services and products that are in accordance with Islamic principles. Generally, the Islamic banks are insufficiently capable of offering typical investment banking services, for example, assurances and fees-based advisory services but the modifications and expansions of fees-based services would improve the functionality of Islamic financial services. Fees-based agreements such as Wakalah, Joalah, and Kifalah need more expansion and development for them to be acknowledged and operationalized to utilize the full abilities of Islamic banks.110

Capital markets development

Taking action to the recent wave of oil incomes and increasing demand for shariah compliant services and products, Islamic capital markets are growing at a hastening pace and stakeholders are beginning to understand their potential. Development of institutional infrastructure like accounting standards and regulatory bodies is a step in the right direction towards harmonizing Islamic financial regulations but this requires all stakeholders as well as the government to institute policies towards this end.111 Well built Islamic capital markets will not just help institutional investors and borrowers, but can also improve Islamic banks operations by offering them with advanced risks management, liquidity and portfolios tools.112 Eventually, these improvements will aid in integrating the Islamic financial institutions together with conventional worldwide financial systems.

Conclusion

Unless, the Islamic scholars start by hammering out standardized interpretation of Islamic laws as pertains Islamic Finance, the prospects for harmonizing IFIs with international business law will remain impossible if the findings of this paper are anything to go by. As it is the more Islamic banks continues to invent new financial products in tandem with the need of a fast globalizing market that is spearheaded by the conventional banks, the harder it becomes to integrate IFIs with international laws. The problem is and will always remain the fact that IFIs are regulated by theocratic law that can rarely if ever be expected to change while international business law is an ever evolving concept that is refined now and then to keep pace with the global developments.

With such an arrangement it is unlikely that the two concepts of IFIs and international business law will ever be reconciled, and I hypothesize that they will always be crashing save for the few times that they appear to be consistent in principles. In any case ban on riba, speculative trading, ban on gharar-maisir and PLS will always remain central to Islamic finance. So perhaps the question is if the international business law will ever embrace this, if that might be the case then it will mean that the concept of capitalism as we know it will also need to change.

Bibliography

Aggarwal, R. K. and Yousef, T., 2000. Islamic Banks and Investment Financing. Journal of Money, Credit and Banking, 32, 1: 31-43.

Ahmad A., Rehman K., & Saif M.I., 2010. Islamic Banking Experience of Pakistan: Comparison Between Islamic and Conventional Banks. International Journal of Business and Management, 5,2: 137-143.

Aioanei. S., 2007. European Challenges for Islamic Banks. Romanian Journal. 10.25: 7-20.

Aktar. W, Akhtar. N & Jaffri K.A. 2009. Islamic MicroFinance and Poverty Alleviation: A Case Of Pakistan. Proceedings 2nd CBRC. Lahore. Pakistan.

Ali, K.2005. Islamic Banking. Journal of Islamic Banking and Finance, 4, 1: 31-56.

Alkhan, Khalid. 2006. Islamic Securitization A Revolution in the Banking Industry. Abudhabi: Miracle Graphics Co.

Ayub, Muhammad. 2008. Understanding Islamic Finance. London: John Wiley & Sons Ltd.

Basel.org. A New Capital Adequacy Framework. 2000. Consultative Paper Issued by the Basel Committee on Banking Supervision. Web.

Basel, 2001. History of the Basel Committee and its Membership. Web.

Basel, 2006. International Convergence of Capital Measurement and Capital Standards. Web.

Chapra, M. Umer. 2007.Challenges facing the Islamic financial industry: Handbook of Islamic Banking. ed. by Hassan, M. Kabir & Lewis, Mervyn K. Northampton, US: Edward Elgar Publishing, Inc.

El-Gamal, M. 2005. Islamic Banking Corporate Governance and Regulation: A call for Mutualization. Web.

El-Gamel, M. 2006. Islamic Finance. Web.

Ezinearticles.com. 2011. Challenges faced by Islamic finance. Web.

Earnest, Y. 2010. The Islamic Funds & Investments Report. Web.

eStandardforum, 2009. Jordan: Core Principles for Effective Banking Supervision. On-line. Available from internet, Accessed 28, Jul. 2011.

FiMarkets, 2009. The Solvency Ratio. Web.

Fsa.gov.uk. 2011. Islamic finance in the UK: Regulation and challenges. Web.

FederalReserve.org. 2006. Federal Reserve Statistical Release Z.1: Flow of Funds Accounts of the United States, Flows and Outstandings, Fourth Quarter. Web.

Gurulkan, H. 2010. Islamic Securitization: A legal approach. Web.

Hassan, Z., 1995. Economic Development in Islamic Perspective: Concepts, Objectives and Some Issues. In Journal of Islamic Economics, 1, 6: 80-111.

Hassan, M. 2004. Issues in the Regulation of Islamic Banking: The case of Sudan. Web.

Hassan , M. & Lewis, M. 2007. Islamic banking: an introduction and overview: Handbook of Islamic Banking. Northampton, US: Edward Elgar Publishing, Inc.

Hesse, H., Jobst, A. A., and Sole, J. 2008. Trends and challenges in Islamic finance. In Journal of world economics, 9.2: 175-193.

Iqbal, M. & Molyneux P.,2005. Thirty Years of Islamic Banking: History, Performance and Prospects. Islamic Economic 19, 1: 37-39.

Iqbal, Z., A. Mirakhor, N. Krichenne and H. Askari. 2010. The Stability of Islamic Finance: Creating a Resilient Financial Environment for a Secure Future, Wiley Finance.

Kayed, R. & Kabir, H. 2008. Islamic Entrepreneurship. Riyadh, Routledge.

Kettering, K. 2008. Securitization and its Discontents: The Dynamics of Financial Product Development. Journal of Cardozo Law Review, 29.4: 1555-1598.

Kuran, T. 2001, Speculations on Islamic Financial Alternatives: A Response to Bill Maurer. Anthropology Today, 17, 3.

Khan, M.M. and Bhatti, M. I. 2008. Development in Islamic Banking: A Financial Risk- Allocation Approach. Journal of Risk Finance, 9, 1: 40-51.

Lawai H., 1994. Key Features in Islamic Banking. Journal of Islamic Banking and Finance. 11.4.7-13.

Lee Kun-ho & Ullah S. 2008. Inter-bank Cooperation between Islamic and Conventional-The case of Pakistan. International Review of Business Research Papers, 4,4, 9: 1-26.

Malik, M. S., Malik, A. and Mustafa, W. 2011. Controversies that make Islamic banking controversial: An analysis of issues and challenges. Journal of social and management sciences, 2.1(2011):41-46.

Meraj, A., 2010, Islamic Banking Challenges and Growth. Web.

Nzibo.com. Challenges facing Islamic banks. On-line. Available from internet Web.

Obaidulah, M. 2007. Securitization in Islam: Handbook of Islamic Banking. ed. by Hassan, M. Kabir & Lewis, Mervyn K. Northampton, US: Edward Elgar Publishing, Inc.

ObaidUllah M., 2008. Islamic Finance for Micro & Medium Enterprises. Center for Islamic Banking, Finance and Management. University Brunei Darussalam.

Rasmusen, E., 1988. Mutual Banks and Stock Banks. Journal of Law and Economics, 31(2): 188-199.

Saleh, A. and Zeitun, R., 2006. Islamic Banking Performance in the Middle East: A Case Study of Jordan. Web.

Shenker, C. & Colletta, A.1991. Asset Securitization. Evolution, Current Issues and New Frontiers, 69: 1369: 1370-88.

Siddiqui, M.N., 2006. Islamic Banking and Finance in theory and practice: A Survey of state of the Art. Journal of Islamic Economics Studies, Islamic Research and Training Institute, Islamic Development bank, 13, 2 29-42.

Scott, H., 2005. Capital Adequacy Beyond Basel: Banking, Securities and Insurance. Washington, DC: Oxford University Press.

Schleifer, A. and Vishny, R., 1997. A Survey of Corporate Governance. Journal of Finance, 52(8): 145-162.

Shahfoundationbd.org. Islamic banking: problems and prospects. Web.

Sheikh S.A., 2010. An alternative Approach to practical Islamic Corporate Finance. Web.

Sheikh S.A., 2007. Critical Analysis of Current Islamic Banking System. Web.

SunGard., 2008. Islamic Banking and Finance-Growth and Challenges Ahead. Web.

Timberg, A., 2000. Risk Management: Islamic Financial policies. Islamic banking and its Potential Impact. Web.

Usmani, T., 2008. Islamic Finance: Musharakah & Mudarabah. Journal of Islamic Banking and Finance, 25, 3: 41-53.

Zaher, T. & Kabir, H. 2004. A Comparative Literature Survey of Islamic Finance and Banking. London: John Wiley & Sons Ltd.

Footnotes

- El-Gamel, M. 2006. Islamic Finance. Web.

- Ibid.

- Ibid.

- Hassan, M. 2004. Issues in the Regulation of Islamic Banking: The case of Sudan. Web.

- El-Gamel, Islamic Finance.

- Iqbal, Z., A. Mirakhor, N. Krichenne and H. Askari. 2010. The Stability of Islamic Finance: Creating a Resilient Financial Environment for a Secure Future, Wiley Finance.

- Alkhan, Khalid. 2006. Islamic Securitization A Revolution in the Banking Industry. Abudhabi: Miracle Graphics Co.

- Ibid, p. 54.

- Ibid, p. 54.

- Chapra, M. Umer. 2007.Challenges facing the Islamic financial industry: Handbook of Islamic Banking. ed. by Hassan, M. Kabir & Lewis, Mervyn K. Northampton, US: Edward Elgar Publishing, Inc.

- Malik, M. S., Malik, A. and Mustafa, W. Controversies that make Islamic banking controversial: An analysis of issues and challenges. In Journal of social and management sciences, 2.1(2011):41-46.

- Earnest, Y. 2010. The Islamic Funds & Investments Report. Web.

- Ibid.

- Hassan, M. 2004. Issues in the Regulation of Islamic Banking: The case of Sudan. Web.

- Ibid.

- Ibid.

- Hassan, Issues in the regulation of Islamic Banking.

- Hassan , M. & Lewis, M. 2007. Islamic banking: an introduction and overview: Handbook of Islamic Banking. Northampton, US: Edward Elgar Publishing, Inc. Web.

- Ibid.

- Hassan , M. & Lewis, M. 2007. Islamic banking: an introduction and overview: Handbook of Islamic Banking.

- Hesse, H., Jobst, A. A., and Sole, J. 2008. Trends and challenges in Islamic finance. In Journal of world economics, 9.2: 175-193.

- Timberg, A. 2000. Risk Management: Islamic Financial policies. Islamic banking and its Potential Impact. Web.

- Ibid.

- Ibid.

- Saleh, A. and Zeitun, R., 2006. Islamic Banking Performance in the Middle East: A Case Study of Jordan. Web.

- Lawai H., 1994. Key Features in Islamic Banking. In Journal of Islamic Banking and Finance. 11.4.7-13.

- Ayub, Muhammad. 2008. Understanding Islamic Finance. London: John Wiley & Sons Ltd.

- Kayed, R. & Kabir, H. 2008. Islamic Entrepreneurship. Riyadh, Routledge.

- Gurulkan, H. 2010. Islamic Securitization: A legal approach. Web.

- Ibid.

- Sheikh S.A., 2007. Critical Analysis of Current Islamic Banking System. Online, Available from internet, www.accountancy.com.pk. Accessed 30, Jul. 2011.

- Sheikh S.A., 2007. Critical Analysis of Current Islamic Banking System.

- Siddiqui, M.N., 2006. Islamic Banking and Finance in theory and practice: A Survey of state of the Art. In Journal of Islamic Economics Studies, Islamic Research and Training Institute, Islamic Development bank, 13, 2, 29-42.

- Meraj, A., 2010, Islamic Banking Challenges and Growth. Online. Available from internet , www.thebanker.com, Accessed 28, Jul. 2011.

- Kayed, R. & Kabir, H. 2008. Islamic Entrepreneurship.

- Kettering, K. 2008. Securitization and its Discontents: The Dynamics of Financial Product Development. In Journal of Cardozo Law Review, 29.4: 1555-1598.

- Ibid.

- Usmani, T., 2008. Islamic Finance: Musharakah & Mudarabah. In Journal Of Islamic Banking and Finance, 25, 3: 41-53.

- Ibid.

- Ibid.

- Aggarwal, R. K. and Yousef, T., 2000. Islamic Banks and Investment Financing. Journal of Money, Credit and Banking, 32, 1, 31-43.

- Aggarwal, R. K. and Yousef, T., 2000. Islamic Banks and Investment Financing.

- Ibid.

- Ali, K.2005. Islamic Banking, Journal of Islamic Banking and Finance, 4, 1, 31-56.

- Obaidulah, M. 2007. Securitization in Islam: Handbook of Islamic Banking. ed. by Hassan, M. Kabir & Lewis, Mervyn K. Northampton, US: Edward Elgar Publishing, Inc.

- Ibid.

- ObaidUllah M., 2008. Islamic Finance for Micro & Medium Enterprises. Center for Islamic Banking, Finance and Management, University Brunei Darussalam.

- Ibid.

- Shenker, C. & Colletta, A. 1991. Asset Securitization: Evolution, Current Issues and New Frontiers, 69: 1369, 1370-88.

- Ibid.

- Zaher, T. & Kabir, H. 2004. A Comparative Literature Survey of Islamic Finance and Banking. London: John Wiley & Sons Ltd.

- Schleifer, A. and Vishny, R., 1997. A Survey of Corporate Governance. Journal of Finance, 52(8), pp 145-162.

- Basel, 2000. A New Capital Adequacy Framework. Consultative Paper Issued by the Basel Committee on Banking Supervision. Web.

- Ibid.

- Rasmusen, E., 1988. Mutual Banks and Stock Banks. Journal of Law and Economics, 31(2), pp 188-199.

- Basel, 2000. A New Capital Adequacy Framework. Consultative Paper Issued by the Basel Committee on Banking Supervision.

- Ibid.

- Basel, 2001. History of the Basel Committee and its Membership. Web.

- Basel, 2001. History of the Basel Committee and its Membership.

- Ibid.

- FiMarkets, 2009. The Solvency Ratio. Web.

- Basel.org. A New Capital Adequacy Framework. 2000.Consultative Paper Issued by the Basel Committee on Banking Supervision, Web.

- Ibid

- Ibid.

- Scott, H., 2005. Capital Adequacy Beyond Basel: Banking, Securities and Insurance. Washington, DC: Oxford University Press.

- Basel.org. A New Capital Adequacy Framework.

- Basel, 2006. International Convergence of Capital Measurement and Capital Standards. Web.

- Khan, M.M. and Bhatti, M. I.,.2008. Development in Islamic Banking: A Financial Risk-Allocation Approach, In Journal of Risk Finance, 9, 1, 40-51.

- eStandardforum, 2009. Jordan: Core Principles for Effective Banking Supervision. Web.

- Ibid.

- Ahmad A., Rehman K., & Saif M.I., 2010. Islamic Banking Experinec of Pakistan: Comparison Between Islamic and Conventional Banks. In International Journal of Business and Management, 5,2,137-143.

- Ibid.

- Aktar. W, Akhtar. N & Jaffri K.A. 2009. Islamic MicroFinance and Poverty Alleviation: A Case Of Pakistan. Proceedings 2nd CBRC. Lahore. Pakistan.

- Iqbal, M. & Molyneux P.,2005. Thirty Years of Islamic Banking: History, Performance and Prospects. In Islamic Economic 19, 1, 37-39.

- Ibid.

- Ali, K.2005. Islamic Banking, Journal of Islamic Banking and Finance, 4, 1, 31-56.

- Siddiqui, M.N., 2006. Islamic mBanking and Finance in theory and practice: A Survey of state of the Art. In Journal of Islamic Economics Studies, Islamic Research and Training Institute, Islamic Development bank, 13, 2, 29-42.

- Ibid, p. 31.

- Obaidulah, M. 2007. Securitization in Islam: Handbook of Islamic Banking

- Gurulkan, H. 2010. Islamic Securitization: A legal approach.

- Kuran, T. 2001, Speculations on Islamic Financial Alternatives: A Response to Bill Maurer. Anthropology Today, 17, 3.

- Timberg, A., 2000. Risk Management: Islamic Financial policies. Islamic banking and its Potential Impact. Web.

- Ibid.

- Zaher, T. & Kabir, H. 2004. A Comparative Literature Survey of Islamic Finance and Banking. London: John Wiley & Sons Ltd.

- Ibid.

- Ibid

- Ibid.

- Fsa.gov.uk. 2011. Islamic finance in the UK: Regulation and challenges. Web.

- Ibid.

- Ibid.

- Ezinearticles.com. 2011. Challenges faced by Islamic finance. Web.

- Ezinearticles.com. 2011. Challenges faced by Islamic finance.

- FederalReserve.org. 2006. Federal Reserve Statistical Release Z.1: Flow of Funds Accounts of the United States, Flows and Outstandings, Fourth Quarter. Web.

- Ibid.

- SunGard., 2008. Islamic Banking and Finance-Growth and Challenges Ahead. Web.

- SunGard., 2008. Islamic Banking and Finance-Growth and Challenges Ahead.

- Ibid.

- Sheikh S.A., 2010.An alternative Approach to practical Islamic Corporate Finance. Web.

- Shahfoundationbd.org. Islamic banking: problems and prospects. Web.

- Aioanei. S., (2007), European Challenges for Islamic Banks. In the Romanian Journal. 10.25. 7-20.

- El-Gamal, M. 2005. Islamic Banking Corporate Governance and Regulation: A call for Mutualization, Web.

- Ibid.

- Ibid.

- Hassan, Z., (1995), Economic Development in Islamic Perspective: Concepts, Objectives and Some Issues. In Journal of Islamic Economics, 1, 6, 80-111.

- Hassan, M., 2004. Issues in the Regulation of Islamic Banking: The case of Sudan. Web.

- Aggarwal, R. K. and Yousef, T., 2000. Islamic Banks and Investment Financing.

- Ibid.

- Ibid

- Nzibo.com. Challenges facing Islamic banks. Web.

- Ali, K.2005. Islamic Banking, Journal of Islamic Banking and Finance, 4, 1, 31-56.

- Lee Kun-ho & Ullah S. 2008. Inter-bank Cooperation between Islamic and Conventional-The case of Pakistan. International Review of Business Research Papers, 4,4, 9: 1-26.

- Ali, K.2005. Islamic Banking, Journal of Islamic Banking and Finance.