Abstract

This essay considers the three global airline alliances, SkyTeam, Star Alliance and oneworld. Having emerged between 1997 and 2000, they have proceeded to dominate the intercontinental travel industry, leading to concerns over anti-competitive practices. The essay makes the case that they have ultimately been beneficial for the aviation industry despite the potential drawbacks. They find that the three organisations are generally stratified, with oneworld being the smallest in most aspects and Star Alliance being the largest. However, oneworld has better access to the world’s busiest airports than SkyTeam, which may enable it to have higher profits despite the lower revenue. In terms of impact on the industry, the essay finds that global alliances have not affected the profitability of their members despite the purported advantages. However, they have produced increased convenience and cost reductions for passengers compared to their independent counterparts. Moreover, while regulatory bodies were originally concerned over global alliances, they came to recognise their benefits in facilitating international travel. As such, the hypothesis that the effect of airline partnerships on the aviation industry has been positive overall has been confirmed. As long as their anti-competitive tendencies are contained, and they generally are, alliances are positive forces that should continue operating as long as they are viable.

Introduction

Since the initial collaboration between Northwest Airlines and KLM in 1989, airlines worldwide started recognising the benefits of cooperation. Various agreements and inter-organisational efforts took place, and alliances began emerging. Over time, they consolidated and grew in size, leading to the emergence of three global strategic airline alliances: SkyTeam, Star Alliance and One World. Such a development can naturally cause alarm over a potential oligopoly developing, but its benefits also have to be considered. The author’s position is that the organisations mentioned above have created positive change for airlines and customers. To that end, the essay will explore these three entities in terms of their history and current position relative to each other before discussing the effects they have had on commercial aviation.

Star Alliance

Star Alliance, which is headquartered in Germany, is the largest of the three global entities. Per The history of Star Alliance (2020), it was founded on May 14, 1997, in an agreement between Air Canada, Lufthansa, SAS, Thai Airways International and United Airlines. It then proceeded to expand aggressively, but some later members such as VARIG Brazilian Airlines, which joined in October 1997, would eventually leave the alliance (The history of Star Alliance, 2020). Currently, Star Alliance has 26 members, namely, Aegean, Air Canada, Air China, Air India, Air New Zealand, ANA, Asiana Airlines, Austrian, Avianca, Brussels Airlines, Copa Airlines, Croatia Airlines, EgyptAir, Ethiopian, Eva Air, Polish Airlines, Lufthansa, SAS, Shenzhen Airlines, Singapore Airlines, South African Airways, Swiss, Air Portugal, Thai Airways, Turkish Airlines and United (Star Alliance, 2020). It also has agreements with other airlines that are not members.

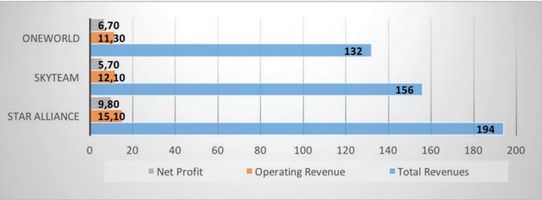

As seen in Fig. 1, Star Alliance is the largest of the three in most statistics, consistently taking a leadership position. In 2019, it had 762.27 million annual passengers, serving over 1300 airports in 195 different countries (Star Alliance, 2019). As can be seen in Fig. 1, its revenues and net profit are by far the highest of the three entities, likely as a result of having the most extensive operations and adequate efficiency. As a result, it has gained massive power in the market, which it has leveraged to its advantage. Boyce and Ville (2017) note that it has worked to displace ticket-purchasing intermediaries such as travel agents, in particular, encouraging passengers to buy online directly from the company. For an individual carrier, such a practice would likely be challenging to implement due to the market share held by these firms. However, Star Alliance was able to coordinate the efforts of its numerous members and ultimately change the arrangement to one that is more profitable for itself and its flyers.

Despite its success, the group may be experiencing some difficulties as a result of its size. Doganis (2019) highlights the danger of disparate interests emerging as the number of members with conflicting interests increases, as well as the changing priorities of early joiners. While the interests of the carriers that joined early may have been aligned with those of the other members at the time of the agreement’s signing, they could have changed since then and become conflicting. Forsyth et al. (2016) provide the specific example of Lufthansa scheduling a business-class flight five minutes before the departure of a similar one by Singapore Airlines in 2007. Even after the service was discontinued, Lufthansa did not cooperate with its alliance partner on that route.

SkyTeam

The first of the alliances discussed, SkyTeam, is between the other two in terms of size. It was formed on June 22, 2000, as a partnership between Aeromexico, Air France, Delta Air Lines and Korean Air, expanding to integrate Aeromexpress, Air France Cargo, Delta Air Logistics and Korean Air Cargo in September (A history of excellence, 2020). At that time, it already served a large number of destinations, making it attractive for other airlines to join because of the prospects for seamless travel provided. As such, over the following years, SkyTeam would include fifteen more members, dramatically expanding its passenger numbers and reach (A history of excellence, 2020). Its current membership comprises Aeroflot, Aerolineas Argentinas, Aeroméxico, AirEuropa, Air France, Alitalia, China Airlines, China Eastern, Czech Airlines, Delta, Garuda Indonesia, Kenya Airways, KLM, Korean Air, Middle East Airlines, Saudia, TAROM, Vietnam Airlines and Xiamen Air (A history of excellence, 2020). Other carriers, such as Continental and Copa, were members at one point but left some time ago to become independent again or join other alliances.

SkyTeam has substantial power in the market due to its size and massive customer base. SkyTeam (2017) claimed that it served 730 million passengers in 2017, though A history of excellence (2020) presents a lower figure at 676 million. The decline is likely associated with the departure of China Southern, one of the Chinese Big Three that accounted for 115 million passengers annually but saw superior opportunities elsewhere (SkyTeam, 2017). Nevertheless, the alliance remains substantial in size and provides its members with considerable reach and power as a result. Fyall et al. (2019) claim that SkyTeam members, MEA in particular, were able to secure improved deals with fuel, catering, and other suppliers after joining it. Due to its size, the organisation can exert substantial pressure on its partners if it chooses, such as when negotiating airport fees, though, for the same reason, it is often subject to increased government scrutiny.

In terms of position, SkyTeam is located between the other two major alliances in most regards. As Fig. 1 shows, it had more revenue than oneworld but less than Star Alliance in 2017, both by a considerable margin, though its net profits are the lowest of the three for unclear reasons. A similar situation may be observed in most of its other statistics, consistent with its overall size and member count. Rhoades (2016) demonstrates that in each regional market, SkyTeam has at least as many member airlines as oneworld but not more than Star Alliance, also being between the two in terms of countries served and fleet size. This tendency of SkyTeam being in the middle is likely to continue in the future, as alliances mature and reduce the number of radical changes that take place.

Oneworld

The smallest of the three alliances, oneworld was formed shortly after Star Alliance. Hayward (2019) states that it was first announced in September 1998 and formally started operations in February 1999, consisting of American Airlines, British Airways, Canadian Airlines, Cathay Pacific and Qantas Airways. These carriers already served a substantial number of people and a broad range of destinations, and the organisation has expanded since. Members (2020) lists American Airlines, British Airways, Cathay Pacific, Finnair, Iberia, Japan Airlines, Malaysia Airlines, Qantas, Qatar Airways, Royal Air Maroc, Royal Jordanian, S7 Airlines and SriLankan Airlines as members, Fiji Airways as a connect partner, and Alaska Airlines as a future member. As with the other two leading alliances, there were some departures, as well, such as Malev and Air Berlin.

Despite starting earlier than SkyTeam, oneworld was not as successful at growing its passenger traffic over time. As Fig. 1 shows, its revenues are the lowest of the three major global airline alliances. However, its net profits are higher than the second-largest alliance’s, implying that it still has an advantage in some aspect. Vasigh et al. (2016) find that in 2012, oneworld held 28% of the market at world’s ten busiest airports as opposed to SkyTeam’s 21% despite its substantially smaller fleet size and destinations served. It may have been able to capitalise on these busy and premium routes to fly more profitably. Regardless, the alliance is likely under the most pressure of the three due to its lowest influence and market power, though it can still exert considerable influence.

Despite its smaller size, oneworld has been able to distinguish itself in other areas, particularly quality. oneworld wins (2017) highlights that, among a high number of other awards, oneworld earned its 15th consecutive World’s Leading Airline Alliance title from World Travel Awards. The result is indicative of its excellent overall performance and service quality that attracted a loyal customer base. With that said, it should be noted that oneworld appears to emphasise the individuality of its member brands. He and Balmer (2016) cite a senior manager who calls oneworld a sub-brand that seems alongside the specific member airline. As such, the alliance’s brand may not have a substantial influence and a powerful position in terms of reputation. However, with increased recognition and continued awards, this situation may change and improve oneworld’s brand equity.

The Benefits and Issues of Global Alliances

When discussing the influence of global alliances on aviation, three primary stakeholder categories should be mentioned: airlines, passengers and regulators. There are others, such as airports, manufacturers and miscellaneous suppliers, but the effect of alliances on them is challenging to evaluate. Airlines likely expect substantial improvements when they join such an arrangement, enough to offset the costs of integration and resulting restrictions. Law et al. (2018) list advantages such as overcoming regulatory barriers, reducing costs, coordinating schedules and prices to optimise loads, and creating barriers for new entrants. By using shared facilities, they enjoy cheaper high-quality maintenance while providing their passengers with superior offers via initiatives such as code sharing. However, it should be noted that an extensive review by Douglas and Tan (2017) finds no evidence that global alliance membership enhanced members’ performance. The authors conclude that either the perceived advantages of an alliance are not as significant in practice as in theory, or the costs of doing so are high enough to compensate.

The primary benefits of global airline alliances for passengers are convenience (expressed through seamless travel) and cost. With their services such as codeshare flights and waiting lounges, alliances can make connections easier and more comfortable. As such, they would be superior to individual airlines for many long-haul flights for which there no direct alternatives. Moreover, shared loyalty programs enable passengers to benefit from such modes of travel more than with non-alliance flights, where unaffiliated carriers would fly different parts of the route. Fare reduction is a more tangible item, suggesting that the reduced costs associated with an alliance enable airlines to charge customers lower prices to obtain a competitive advantage. A counterpoint can be made that an alliance-dominated industry can enable them to charge higher prices in an oligopoly scenario, however. Brueckner and Singer (2019) confirm the first notion, stating that alliance carriers typically charge passengers approximately 7% less than unaffiliated ones. In combination with the loyalty programs mentioned above, this difference creates opportunities for substantial savings, especially for frequent flyers. Without global alliances, these benefits would not have emerged, though it is possible that the increased competition may have compensated them in other ways.

From a regulatory viewpoint, the emergence of a small number of global entities can be seen as problematic, as it jeopardises competition in the field. However, for this reason, they are already reviewing actions that alliances take in substantial detail. Dempsey and Jakhu (2016) state that carriers will typically seek to obtain antitrust authority approval before engaging in any merger-like deals because they face the risk of being challenged otherwise. The safeguards that are currently in place to prevent undesirable carrier behaviours are mostly sufficient to stop abuses of alliances’ positions. Moreover, the emergence of partnerships may have been beneficial for regulatory agencies because of the optimisation that they introduced in the system. Dobson (2017) suggests that antitrust immunity was offered to alliances because they help assemble and distribute passengers, reducing congestion and improving the efciency of the system. As such, despite the concerns, the emergence of alliances can be considered a positive outcome for the aviation industry as a whole.

Conclusion

Overall, though alliances may not have a significant effect on airline performance, they benefited both passengers and regulators. The three current global partnerships have grown substantially large, with over ten members in each, but they have not hurt competition significantly. The reason is that they compete with each other as well as internally, with carriers’ misaligned priorities leading to conflict. At the same time, the cooperation between airlines and the technical optimisations that result lead to the lowering of costs and, consequently, fares, benefiting passengers and regulators interested in more efficient traffic management. This result is significant because it shows that airline alliances are not necessarily harming the aviation industry. As such, they should be permitted to continue under stringent antitrust oversight until they are replaced by developments such as long-haul LCCs.

References

A history of excellence. (2020). SkyTeam. Web.

SkyTeam. (2017). Factsheet: Summer 2017. Web.

Fyall, A., Frochot, I., Legohérel, P., & Wang, Y. (2019). Marketing for tourism and hospitality: Collaboration, technology and experiences. Taylor & Francis.

Kiraci, K. (2019). Does joining global alliances affect airlines’ financial performance? In C. Akar & H. Kapucu (Eds.), Contemporary challenges in business and life sciences (pp. 39-61). Ijopec Publication.

Rhoades, D. L. (2016). Evolution of international aviation: Phoenix rising (3rd ed.). Taylor & Francis.

The history of Star Alliance. (2020). Star Alliance. Web.

Star Alliance. (2020). Star Alliance. Web.

Star Alliance. (2019). October 2019: Facts & figures. Web.

Boyce, G., & Ville, S. (2017). The development of modern business. Macmillan Education, Limited.

Doganis, R. (2019). Flying off course: Airline economics and marketing (5th ed.). Taylor & Francis.

Forsyth, P., Gillen, D., Hüschelrath, K., Niemeier, H. M., & Wolf, H. (Eds.). (2016). Liberalisation in aviation: Competition, cooperation and public policy. United Kingdom: Taylor & Francis.

Hayward, J. (2019). The story of the oneworld alliance. Simple Flying. Web.

Members. (2020). oneworld. Web.

Fleming, K., Vasigh, B., & Tacker, T. (2016). Introduction to air transport economics: From theory to applications (2nd ed.). Taylor & Francis.

oneworld wins its sixth ‘best airline alliance’ award of the year. (2017). oneworld. Web.

He, H. W., & Balmer, J. M. T. (2016). Alliance brands: building corporate brands through strategic alliances? In J. M. T. Balmer, S. M. Powell, J. Kernstock, & T. O. Brexendorf (Eds.), Advances in corporate branding (pp. 72-90). Palgrave Macmillan UK.

Douglas, I., & Tan, D. (2017). Global airline alliances and profitability: A difference-in-difference analysis. Transportation Research Part A: Policy and Practice, 103, 432-443. Web.

Brueckner, J. K., & Singer, E. (2019). Pricing by international airline alliances: A retrospective study. Economics of Transportation, 20. Web.

Dobson, A. (2017). A history of international civil aviation: From its origins through transformative evolution. Taylor & Francis.

Law, C. C. H., Zhang, Y., & Zhang, A. (2018). Regulatory changes in international air transport and their impact on tourism development in Asia Pacific. In X. Fu & J. Peoples (Eds.), Airline economics in Asia (pp. 123-144). Emerald Publishing Limited.

Dempsey, P. S., & Jakhu, R. S. (Eds.). (2016). Routledge handbook of public aviation law. Taylor & Francis.